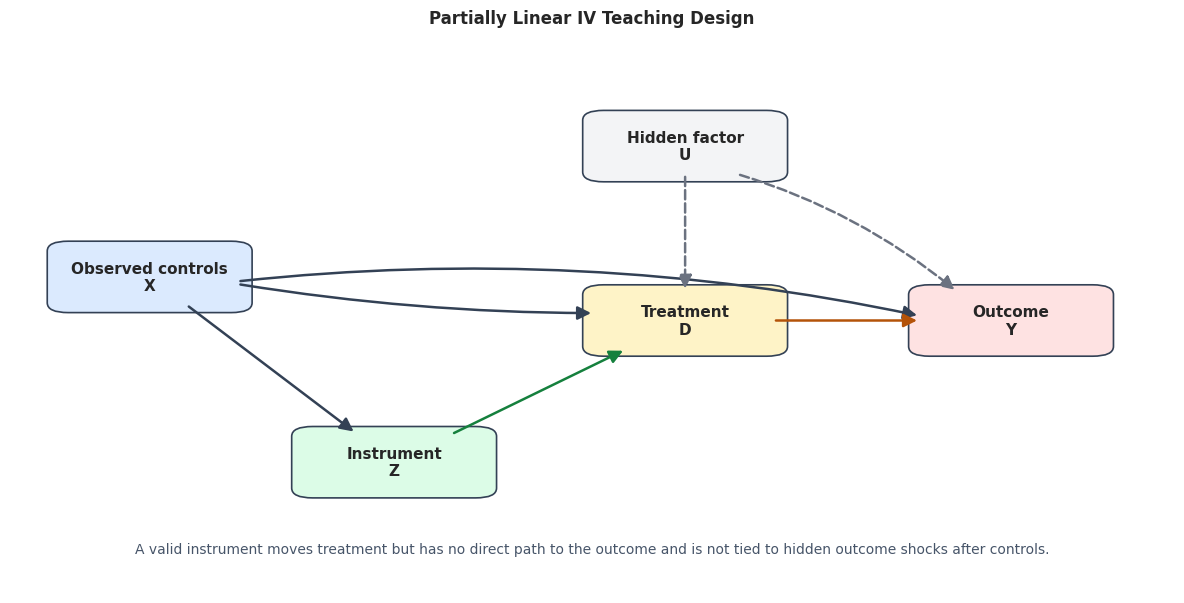

# Define reusable helpers for the Draw The IV Design section.

from matplotlib.patches import FancyBboxPatch, FancyArrowPatch

nodes = {

"X": {"xy": (0.12, 0.58), "label": "Observed controls\nX", "color": "#dbeafe"},

"Z": {"xy": (0.33, 0.24), "label": "Instrument\nZ", "color": "#dcfce7"},

"D": {"xy": (0.58, 0.50), "label": "Treatment\nD", "color": "#fef3c7"},

"Y": {"xy": (0.86, 0.50), "label": "Outcome\nY", "color": "#fee2e2"},

"U": {"xy": (0.58, 0.82), "label": "Hidden factor\nU", "color": "#f3f4f6"},

}

edge_specs = [

("X", "Z", "#334155", "solid", 0.00),

("X", "D", "#334155", "solid", 0.04),

("X", "Y", "#334155", "solid", -0.08),

("Z", "D", "#15803d", "solid", 0.00),

("D", "Y", "#b45309", "solid", 0.00),

("U", "D", "#6b7280", "dashed", 0.00),

("U", "Y", "#6b7280", "dashed", -0.10),

]

fig, ax = plt.subplots(figsize=(12, 6.2))

ax.set_axis_off()

box_w, box_h = 0.14, 0.095

def edge_endpoint(source_xy, target_xy, from_source=True):

"""

Return a point just outside the source or target box boundary.

Parameters

----------

source_xy : tuple[float, float]

Starting coordinate for a drawn edge.

target_xy : tuple[float, float]

Ending coordinate for a drawn edge.

from_source : bool

Whether to compute the boundary point from the source side of the edge.

Returns

-------

tuple[float, float]

Adjusted endpoint coordinate for a directed or partially directed graph edge.

"""

x0, y0 = source_xy

x1, y1 = target_xy

dx, dy = x1 - x0, y1 - y0

scale = 1.0 / max(abs(dx) / (box_w / 2), abs(dy) / (box_h / 2))

if from_source:

return (x0 + dx * scale * 1.08, y0 + dy * scale * 1.08)

return (x1 - dx * scale * 1.12, y1 - dy * scale * 1.12)

for spec in nodes.values():

x, y = spec["xy"]

rect = FancyBboxPatch(

(x - box_w / 2, y - box_h / 2),

box_w,

box_h,

boxstyle="round,pad=0.018",

facecolor=spec["color"],

edgecolor="#334155",

linewidth=1.2,

zorder=3,

)

ax.add_patch(rect)

ax.text(x, y, spec["label"], ha="center", va="center", fontsize=11, fontweight="bold", zorder=4)

for start, end, color, style, rad in edge_specs:

start_xy = edge_endpoint(nodes[start]["xy"], nodes[end]["xy"], from_source=True)

end_xy = edge_endpoint(nodes[start]["xy"], nodes[end]["xy"], from_source=False)

arrow = FancyArrowPatch(

start_xy,

end_xy,

arrowstyle="-|>",

mutation_scale=20,

linewidth=1.8,

color=color,

linestyle=style,

connectionstyle=f"arc3,rad={rad}",

zorder=5,

)

ax.add_patch(arrow)

ax.text(

0.50,

0.08,

"A valid instrument moves treatment but has no direct path to the outcome and is not tied to hidden outcome shocks after controls.",

ha="center",

va="center",

fontsize=10,

color="#475569",

)

ax.set_title("Partially Linear IV Teaching Design", pad=18)

plt.tight_layout()

fig.savefig(FIGURE_DIR / f"{NOTEBOOK_PREFIX}_pliv_design_dag.png", dpi=160, bbox_inches="tight")

plt.show()