import warnings

warnings.filterwarnings("ignore")

from IPython.display import Markdown, display

from graphviz import Digraph

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import seaborn as sns

from scipy.special import softmax, expit

from scipy.stats import norm

from sklearn.compose import ColumnTransformer

from sklearn.ensemble import HistGradientBoostingClassifier

from sklearn.metrics import roc_auc_score

from sklearn.pipeline import Pipeline

from sklearn.preprocessing import OneHotEncoder

rng = np.random.default_rng(20260430)

sns.set_theme(style="whitegrid", context="notebook")

plt.rcParams["figure.figsize"] = (10, 5)

plt.rcParams["axes.spines.top"] = False

plt.rcParams["axes.spines.right"] = False

plt.rcParams["figure.dpi"] = 130

def pct(x, digits=1):

return f"{100 * x:.{digits}f}%"

def dollars(x, digits=0):

return f"${x:,.{digits}f}"

def styled_table(df, pct_cols=None, money_cols=None, num_cols=None):

pct_cols = pct_cols or []

money_cols = money_cols or []

num_cols = num_cols or []

fmt = {}

for col in pct_cols:

fmt[col] = lambda v: pct(v, 2)

for col in money_cols:

fmt[col] = lambda v: dollars(v, 2) if abs(v) < 100 else dollars(v, 0)

for col in num_cols:

fmt[col] = lambda v: f"{v:,.3f}"

return df.style.format(fmt)03. Recommendation Systems and Ranking

Recommendation systems are causal systems hiding inside machine learning systems.

A recommender does not merely predict what a user likes. It changes what the user sees, clicks, buys, watches, saves, and returns to later. That means offline metrics based on historical clicks can be deeply misleading:

- popular items get more exposure, so they get more clicks,

- top-ranked items get more attention, so they look more relevant,

- the production policy decides what data exists,

- unexposed items have missing outcomes,

- a new ranking policy may put users into contexts that the old policy rarely explored.

This notebook turns recommendation and ranking into causal decision problems. We will simulate logged recommendation data, estimate policy value using off-policy evaluation, diagnose support and position bias, and design a professional readout for whether a new ranking policy is ready for an online test.

Learning Goals

By the end of this notebook, you should be able to:

- Explain why recommender feedback is logged under a behavior policy.

- Define policy value for recommendations and rankings.

- Distinguish prediction metrics from causal policy metrics.

- Estimate a new recommender policy offline using IPS, SNIPS, and doubly robust estimators.

- Diagnose common support and effective sample size problems.

- Explain position bias and inverse examination weighting.

- Identify feedback loops created by exposure-based learning.

- Translate offline causal evidence into an A/B test decision memo.

1. Setup

We will use numpy, pandas, sklearn, statsmodels, seaborn, and Graphviz.

2. The Causal Question in Recommendation

A supervised recommender asks:

Which item is the user likely to click, given historical data?

A causal recommender asks:

What reward would the user generate if we showed a different item or ranking?

For a single recommendation slot, let \(A_i\) be the item shown to user-context \(X_i\) and let \(Y_i(a)\) be the reward if item \(a\) were shown. The value of a policy \(\pi\) is:

\[ V(\pi) = E\left[\sum_a \pi(a\mid X)Y(a)\right] \]

For a deterministic policy that always chooses one item:

\[ V(\pi) = E[Y(\pi(X))] \]

The difficulty is that logged data contains only:

\[ Y_i = Y_i(A_i) \]

We do not observe what would have happened for items that were not shown. This is the same fundamental problem of causal inference, now inside a recommender system.

3. Why Historical Clicks Are Biased

The production recommender is the data-generating process. If it mostly shows popular items, the data will mostly contain outcomes for popular items. If it rarely shows new items, the data will contain little evidence about new items.

This creates several biases:

- Selection bias: only shown items have observed outcomes.

- Position bias: top-ranked items are more likely to be examined and clicked.

- Popularity bias: old winners get more exposure and therefore more feedback.

- Trust bias: users may click top results because they trust the system.

- Support failure: a target policy may choose actions rarely or never chosen by the logging policy.

Counterfactual learning-to-rank work studies how to learn from biased interaction logs. Jagerman and de Rijke (2020) describe position bias as users observing and clicking top-ranked items more than lower-ranked ones. Vardasbi, Oosterhuis, and de Rijke (2020) emphasize that clicks can be biased by position, selection, and trust, so click probability is not the same as relevance probability.

dot = Digraph("recsys_causal_graph", format="svg")

dot.attr(rankdir="LR", bgcolor="transparent")

dot.attr("node", shape="box", style="rounded,filled", color="#3B4252", fillcolor="#EEF2F7", fontname="DejaVu Sans")

dot.attr("edge", color="#5E6C84", fontname="DejaVu Sans")

dot.node("context", "User context\nhistory, segment,\nintent")

dot.node("policy", "Logging policy\nproduction ranker")

dot.node("shown", "Shown item or slate")

dot.node("position", "Position and layout")

dot.node("reward", "Observed reward\nclick, watch, purchase")

dot.node("unobserved", "Unobserved rewards\nfor hidden items")

dot.node("newpolicy", "Target policy\ncandidate ranker")

dot.node("decision", "Decision\nship, test,\nrollback")

dot.edge("context", "policy")

dot.edge("policy", "shown")

dot.edge("context", "reward")

dot.edge("shown", "reward", label="causal effect")

dot.edge("position", "reward", label="examination")

dot.edge("shown", "position")

dot.edge("policy", "unobserved", label="missingness")

dot.edge("newpolicy", "decision")

dot.edge("reward", "decision", label="offline estimate")

dot

Off-policy evaluation (OPE) formalizes this problem. Su, Dimakopoulou, and Krishnamurthy (2019) describe the key OPE challenge as distribution mismatch between the target policy and the logging policy. Saito and Joachims (2022) note that recommender systems often have large action spaces, which can make support and variance problems severe.

4. Running Example: Logged Top-Slot Recommendations

We will simulate an e-commerce recommender that chooses one item for the top recommendation slot.

Each impression has:

- user segment,

- user price sensitivity,

- user novelty preference,

- item category,

- item popularity,

- item margin,

- the item shown by the production logging policy,

- the logging propensity for that item,

- observed click/purchase reward.

Because this is a simulation, we also know the true expected reward for every possible item. In real data, those counterfactual rewards are hidden.

def make_catalog(seed=10):

local_rng = np.random.default_rng(seed)

categories = ["electronics", "home", "beauty", "sports", "fashion", "books", "grocery", "travel"]

rows = []

for item_id in range(12):

category = categories[item_id % len(categories)]

quality = local_rng.normal(0.0, 0.55)

popularity = local_rng.beta(2.2, 2.8)

margin = local_rng.uniform(8, 48)

novelty = local_rng.uniform(0.0, 1.0)

rows.append(

{

"item_id": item_id,

"category": category,

"quality": quality,

"popularity": popularity,

"margin": margin,

"novelty": novelty,

}

)

return pd.DataFrame(rows)

catalog = make_catalog()

display(catalog)| item_id | category | quality | popularity | margin | novelty | |

|---|---|---|---|---|---|---|

| 0 | 0 | electronics | -0.606836 | 0.263463 | 13.436784 | 0.689036 |

| 1 | 1 | home | 0.471865 | 0.639737 | 31.030422 | 0.753302 |

| 2 | 2 | beauty | -0.534751 | 0.561390 | 44.261150 | 0.226114 |

| 3 | 3 | sports | -0.612125 | 0.307741 | 19.297341 | 0.605865 |

| 4 | 4 | fashion | 0.541043 | 0.837651 | 13.976596 | 0.136789 |

| 5 | 5 | books | 0.848267 | 0.375272 | 21.580623 | 0.148569 |

| 6 | 6 | grocery | 0.421832 | 0.357325 | 12.585774 | 0.233090 |

| 7 | 7 | travel | -0.076717 | 0.226836 | 26.273652 | 0.738671 |

| 8 | 8 | electronics | -0.702515 | 0.462519 | 40.669378 | 0.881835 |

| 9 | 9 | home | 0.371261 | 0.198945 | 15.715087 | 0.333217 |

| 10 | 10 | beauty | 0.442547 | 0.256243 | 26.574903 | 0.508629 |

| 11 | 11 | sports | -0.497328 | 0.518320 | 33.348337 | 0.279002 |

def simulate_contexts(n=70_000, seed=20):

local_rng = np.random.default_rng(seed)

segments = local_rng.choice(["deal_seeker", "loyalist", "explorer", "premium"], size=n, p=[0.30, 0.30, 0.25, 0.15])

price_sensitivity = np.clip(

local_rng.beta(2.2, 2.4, size=n)

+ 0.22 * (segments == "deal_seeker")

- 0.18 * (segments == "premium"),

0,

1,

)

novelty_preference = np.clip(

local_rng.beta(2.0, 2.8, size=n)

+ 0.30 * (segments == "explorer")

- 0.12 * (segments == "loyalist"),

0,

1,

)

purchase_intent = np.clip(

local_rng.beta(2.4, 3.0, size=n)

+ 0.18 * (segments == "loyalist")

+ 0.12 * (segments == "premium"),

0,

1,

)

return pd.DataFrame(

{

"impression_id": np.arange(n),

"segment": segments,

"price_sensitivity": price_sensitivity,

"novelty_preference": novelty_preference,

"purchase_intent": purchase_intent,

}

)

segment_category_pref = {

"deal_seeker": {"grocery": 0.42, "fashion": 0.25, "home": 0.20},

"loyalist": {"books": 0.25, "home": 0.22, "beauty": 0.20},

"explorer": {"travel": 0.48, "sports": 0.30, "electronics": 0.22},

"premium": {"electronics": 0.38, "beauty": 0.24, "travel": 0.20},

}

def reward_logit(context_row, item_row):

segment = context_row["segment"]

category_bonus = segment_category_pref.get(segment, {}).get(item_row["category"], -0.08)

return (

-3.35

+ 1.70 * context_row["purchase_intent"]

+ category_bonus

+ 0.62 * item_row["quality"]

+ 0.70 * context_row["novelty_preference"] * item_row["novelty"]

- 0.45 * context_row["price_sensitivity"] * (item_row["margin"] / 48)

+ 0.28 * item_row["popularity"]

)

def compute_reward_matrix(contexts, catalog):

reward = np.zeros((len(contexts), len(catalog)))

for j, item in catalog.iterrows():

# Vectorized version of reward_logit.

category_bonus = np.array(

[segment_category_pref.get(seg, {}).get(item["category"], -0.08) for seg in contexts["segment"]]

)

logits = (

-3.35

+ 1.70 * contexts["purchase_intent"].to_numpy()

+ category_bonus

+ 0.62 * item["quality"]

+ 0.70 * contexts["novelty_preference"].to_numpy() * item["novelty"]

- 0.45 * contexts["price_sensitivity"].to_numpy() * (item["margin"] / 48)

+ 0.28 * item["popularity"]

)

reward[:, j] = expit(logits)

return reward

contexts = simulate_contexts()

true_reward = compute_reward_matrix(contexts, catalog)

true_profit = true_reward * catalog["margin"].to_numpy()

print(f"Contexts: {len(contexts):,}")

print(f"Items: {len(catalog)}")

print(f"Average true reward across all possible context-item pairs: {true_reward.mean():.3%}")Contexts: 70,000

Items: 12

Average true reward across all possible context-item pairs: 10.322%The production logging policy is not random. It favors expected click probability, popularity, and some margin. It also explores a little, which is crucial for later OPE.

def logging_policy_probs(contexts, catalog, true_reward, temperature=0.42, epsilon=0.08):

# Production score mixes relevance with popularity and margin.

score = (

2.20 * true_reward

+ 0.80 * catalog["popularity"].to_numpy()[None, :]

+ 0.20 * (catalog["margin"].to_numpy()[None, :] / catalog["margin"].max())

)

probs = softmax(score / temperature, axis=1)

probs = (1 - epsilon) * probs + epsilon / len(catalog)

return probs

def sample_logged_data(contexts, catalog, true_reward, true_profit, seed=30):

local_rng = np.random.default_rng(seed)

behavior_probs = logging_policy_probs(contexts, catalog, true_reward)

actions = np.array([local_rng.choice(len(catalog), p=p) for p in behavior_probs])

propensities = behavior_probs[np.arange(len(contexts)), actions]

click_prob = true_reward[np.arange(len(contexts)), actions]

clicked = local_rng.binomial(1, click_prob)

margin = catalog.loc[actions, "margin"].to_numpy()

profit = clicked * margin

logged = contexts.copy()

logged["item_id"] = actions

logged["propensity"] = propensities

logged["click"] = clicked

logged["profit"] = profit

logged["true_click_prob_logged_action"] = click_prob

logged = logged.merge(catalog, on="item_id", how="left")

return logged, behavior_probs

logged, behavior_probs = sample_logged_data(contexts, catalog, true_reward, true_profit)

display(logged.head())

print(f"Logged impressions: {len(logged):,}")

print(f"Observed click rate under logging policy: {logged['click'].mean():.3%}")

print(f"Observed profit per impression under logging policy: {logged['profit'].mean():.3f}")| impression_id | segment | price_sensitivity | novelty_preference | purchase_intent | item_id | propensity | click | profit | true_click_prob_logged_action | category | quality | popularity | margin | novelty | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0 | deal_seeker | 0.545175 | 0.261660 | 0.325562 | 2 | 0.101029 | 0 | 0.000000 | 0.037844 | beauty | -0.534751 | 0.561390 | 44.261150 | 0.226114 |

| 1 | 1 | loyalist | 0.140713 | 0.136803 | 0.203040 | 4 | 0.155693 | 0 | 0.000000 | 0.074455 | fashion | 0.541043 | 0.837651 | 13.976596 | 0.136789 |

| 2 | 2 | deal_seeker | 0.568347 | 0.244141 | 0.644651 | 1 | 0.151039 | 0 | 0.000000 | 0.165341 | home | 0.471865 | 0.639737 | 31.030422 | 0.753302 |

| 3 | 3 | loyalist | 0.487899 | 0.386189 | 1.000000 | 5 | 0.110944 | 1 | 21.580623 | 0.304164 | books | 0.848267 | 0.375272 | 21.580623 | 0.148569 |

| 4 | 4 | loyalist | 0.216171 | 0.550332 | 0.955689 | 8 | 0.067100 | 0 | 0.000000 | 0.135393 | electronics | -0.702515 | 0.462519 | 40.669378 | 0.881835 |

Logged impressions: 70,000

Observed click rate under logging policy: 11.131%

Observed profit per impression under logging policy: 2.677exposure = (

logged.groupby(["item_id", "category"])

.agg(

exposure_share=("impression_id", lambda x: len(x) / len(logged)),

observed_ctr=("click", "mean"),

avg_propensity=("propensity", "mean"),

margin=("margin", "first"),

popularity=("popularity", "first"),

quality=("quality", "first"),

)

.reset_index()

.sort_values("exposure_share", ascending=False)

)

display(styled_table(exposure, pct_cols=["exposure_share", "observed_ctr", "avg_propensity"], money_cols=["margin"]))| item_id | category | exposure_share | observed_ctr | avg_propensity | margin | popularity | quality | |

|---|---|---|---|---|---|---|---|---|

| 4 | 4 | fashion | 16.74% | 14.05% | 16.95% | $13.98 | 0.837651 | 0.541043 |

| 1 | 1 | home | 14.53% | 14.77% | 14.92% | $31.03 | 0.639737 | 0.471865 |

| 2 | 2 | beauty | 10.00% | 6.79% | 9.96% | $44.26 | 0.561390 | -0.534751 |

| 11 | 11 | sports | 8.45% | 6.15% | 8.35% | $33.35 | 0.518320 | -0.497328 |

| 8 | 8 | electronics | 8.39% | 7.59% | 8.41% | $40.67 | 0.462519 | -0.702515 |

| 5 | 5 | books | 8.38% | 14.17% | 8.37% | $21.58 | 0.375272 | 0.848267 |

| 6 | 6 | grocery | 6.76% | 13.09% | 6.74% | $12.59 | 0.357325 | 0.421832 |

| 10 | 10 | beauty | 6.52% | 12.11% | 6.46% | $26.57 | 0.256243 | 0.442547 |

| 7 | 7 | travel | 5.55% | 10.73% | 5.73% | $26.27 | 0.226836 | -0.076717 |

| 9 | 9 | home | 5.05% | 11.69% | 5.17% | $15.72 | 0.198945 | 0.371261 |

| 3 | 3 | sports | 5.02% | 7.42% | 5.17% | $19.30 | 0.307741 | -0.612125 |

| 0 | 0 | electronics | 4.61% | 8.21% | 4.70% | $13.44 | 0.263463 | -0.606836 |

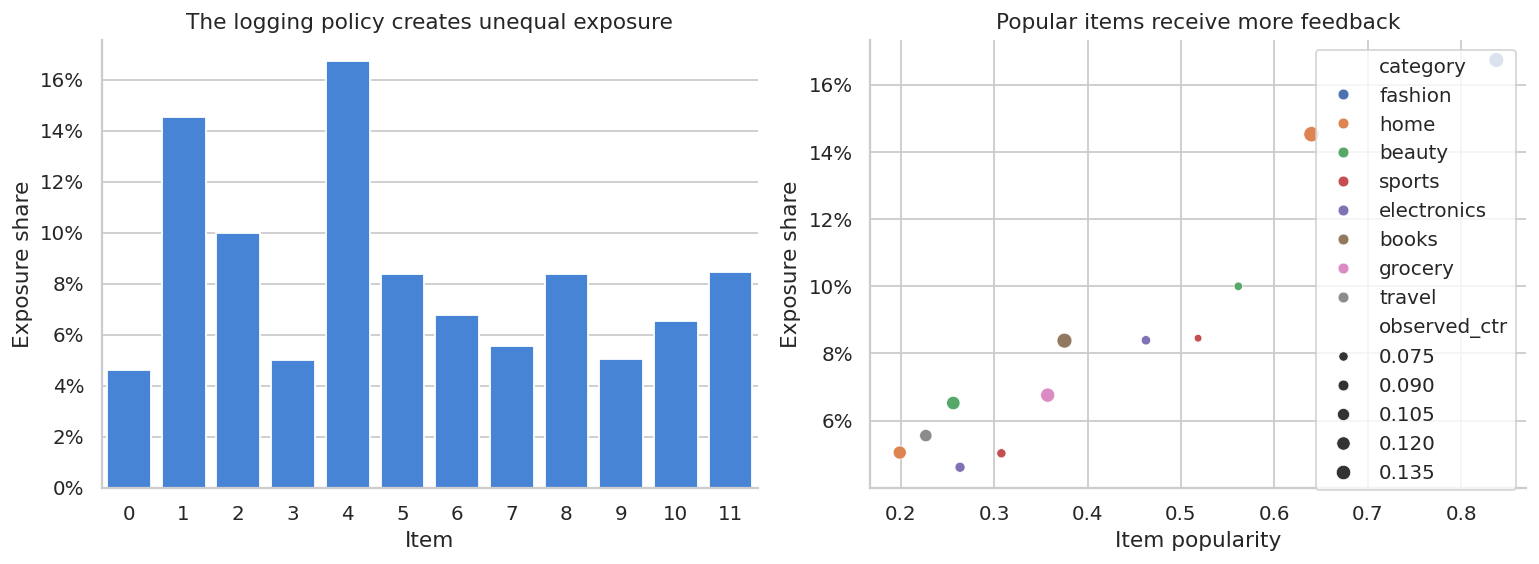

fig, axes = plt.subplots(1, 2, figsize=(12, 4.5))

sns.barplot(data=exposure, x="item_id", y="exposure_share", ax=axes[0], color="#2F80ED")

axes[0].set_title("The logging policy creates unequal exposure")

axes[0].set_xlabel("Item")

axes[0].set_ylabel("Exposure share")

axes[0].yaxis.set_major_formatter(lambda x, pos: f"{100*x:.0f}%")

sns.scatterplot(data=exposure, x="popularity", y="exposure_share", size="observed_ctr", hue="category", ax=axes[1])

axes[1].set_title("Popular items receive more feedback")

axes[1].set_xlabel("Item popularity")

axes[1].set_ylabel("Exposure share")

axes[1].yaxis.set_major_formatter(lambda x, pos: f"{100*x:.0f}%")

plt.tight_layout()

plt.show()

A recommender trained naively on this data will confuse exposure with preference. Items with more exposure have more clicks partly because they were shown more often.

5. Candidate Target Policies

We will evaluate three policies:

- Logging policy: the production policy that collected the data.

- Click-max policy: choose the item with the highest true click probability. In real life we would estimate this.

- Profit-aware policy: choose the item with the highest expected profit.

Because this is a simulation, we can compute the true value of each policy. In real data, we would not know these values.

click_policy_action = true_reward.argmax(axis=1)

profit_policy_action = true_profit.argmax(axis=1)

true_values = pd.DataFrame(

[

{

"policy": "Logging policy",

"true_click_value": np.mean(np.sum(behavior_probs * true_reward, axis=1)),

"true_profit_value": np.mean(np.sum(behavior_probs * true_profit, axis=1)),

},

{

"policy": "Click-max policy",

"true_click_value": true_reward[np.arange(len(contexts)), click_policy_action].mean(),

"true_profit_value": true_profit[np.arange(len(contexts)), click_policy_action].mean(),

},

{

"policy": "Profit-aware policy",

"true_click_value": true_reward[np.arange(len(contexts)), profit_policy_action].mean(),

"true_profit_value": true_profit[np.arange(len(contexts)), profit_policy_action].mean(),

},

]

)

display(styled_table(true_values, pct_cols=["true_click_value"], money_cols=["true_profit_value"]))| policy | true_click_value | true_profit_value | |

|---|---|---|---|

| 0 | Logging policy | 11.08% | $2.68 |

| 1 | Click-max policy | 15.96% | $3.61 |

| 2 | Profit-aware policy | 14.33% | $4.54 |

Notice a common recommender tradeoff: the policy with the best click rate is not necessarily the policy with the best contribution profit.

6. Off-Policy Evaluation Estimators

Assume we have logs from a behavior policy \(\mu(a\mid x)\) and want to estimate the value of target policy \(\pi(a\mid x)\).

Inverse Propensity Score

\[ \hat{V}_{IPS}(\pi) = \frac{1}{n}\sum_{i=1}^n \frac{\pi(A_i\mid X_i)}{\mu(A_i\mid X_i)}Y_i \]

Self-Normalized IPS

\[ \hat{V}_{SNIPS}(\pi) = \frac{\sum_i w_iY_i}{\sum_i w_i} \]

where:

\[ w_i = \frac{\pi(A_i\mid X_i)}{\mu(A_i\mid X_i)} \]

Doubly Robust

Let \(\hat{q}(x,a)\) estimate \(E[Y\mid X=x,A=a]\).

\[ \hat{V}_{DR}(\pi) = \frac{1}{n}\sum_i \left[ \sum_a \pi(a\mid X_i)\hat{q}(X_i,a) + \frac{\pi(A_i\mid X_i)}{\mu(A_i\mid X_i)} \left(Y_i-\hat{q}(X_i,A_i)\right) \right] \]

The direct method uses the outcome model only. IPS uses randomization probabilities only. DR combines both.

feature_cols = ["segment", "price_sensitivity", "novelty_preference", "purchase_intent", "item_id"]

categorical_cols = ["segment", "item_id"]

numeric_cols = ["price_sensitivity", "novelty_preference", "purchase_intent"]

preprocess = ColumnTransformer(

transformers=[

("cat", OneHotEncoder(handle_unknown="ignore", sparse_output=False), categorical_cols),

("num", "passthrough", numeric_cols),

]

)

reward_model = Pipeline(

steps=[

("preprocess", preprocess),

(

"model",

HistGradientBoostingClassifier(

max_iter=120,

learning_rate=0.06,

max_leaf_nodes=20,

random_state=7,

),

),

]

)

reward_model.fit(logged[feature_cols], logged["click"])

logged["q_hat_logged"] = reward_model.predict_proba(logged[feature_cols])[:, 1]

auc = roc_auc_score(logged["click"], logged["q_hat_logged"])

print(f"Outcome model AUC on logged data: {auc:.3f}")Outcome model AUC on logged data: 0.672def predict_q_for_actions(contexts, catalog, model):

blocks = []

for item_id in catalog["item_id"]:

temp = contexts.copy()

temp["item_id"] = item_id

blocks.append(model.predict_proba(temp[feature_cols])[:, 1])

return np.column_stack(blocks)

q_hat_matrix = predict_q_for_actions(contexts, catalog, reward_model)

def ope_for_deterministic_policy(logged, target_actions, q_hat_matrix, outcome_col="click"):

logged_action = logged["item_id"].to_numpy()

mu = logged["propensity"].to_numpy()

reward = logged[outcome_col].to_numpy()

n = len(logged)

match = logged_action == target_actions

weights = match.astype(float) / mu

ips = np.mean(weights * reward)

snips = np.sum(weights * reward) / np.sum(weights)

direct = q_hat_matrix[np.arange(n), target_actions].mean()

dr = np.mean(

q_hat_matrix[np.arange(n), target_actions]

+ weights * (reward - q_hat_matrix[np.arange(n), logged_action])

)

ess = (weights.sum() ** 2) / np.sum(weights**2)

return {

"direct_method": direct,

"ips": ips,

"snips": snips,

"doubly_robust": dr,

"match_rate": match.mean(),

"mean_weight": weights.mean(),

"max_weight": weights.max(),

"effective_sample_size": ess,

}

click_ope = ope_for_deterministic_policy(logged, click_policy_action, q_hat_matrix, outcome_col="click")

profit_ope_click_policy = ope_for_deterministic_policy(logged, click_policy_action, q_hat_matrix, outcome_col="profit")

profit_ope_profit_policy = ope_for_deterministic_policy(logged, profit_policy_action, q_hat_matrix, outcome_col="click")

ope_click_table = pd.DataFrame(

[

{

"policy": "Click-max policy",

"true_value": true_values.loc[true_values["policy"].eq("Click-max policy"), "true_click_value"].iloc[0],

**click_ope,

},

{

"policy": "Profit-aware policy",

"true_value": true_values.loc[true_values["policy"].eq("Profit-aware policy"), "true_click_value"].iloc[0],

**ope_for_deterministic_policy(logged, profit_policy_action, q_hat_matrix, outcome_col="click"),

},

]

)

display(

styled_table(

ope_click_table[

[

"policy",

"true_value",

"direct_method",

"ips",

"snips",

"doubly_robust",

"match_rate",

"effective_sample_size",

"max_weight",

]

],

pct_cols=["true_value", "direct_method", "ips", "snips", "doubly_robust", "match_rate"],

num_cols=["effective_sample_size", "max_weight"],

)

)| policy | true_value | direct_method | ips | snips | doubly_robust | match_rate | effective_sample_size | max_weight | |

|---|---|---|---|---|---|---|---|---|---|

| 0 | Click-max policy | 15.96% | 13.48% | 16.20% | 16.17% | 16.15% | 10.69% | 6,449.281 | 16.314 |

| 1 | Profit-aware policy | 14.33% | 13.58% | 14.16% | 14.50% | 14.50% | 14.03% | 9,547.849 | 15.346 |

The target policies are deterministic, so only impressions where the logged item matches the target item contribute to IPS. If the match rate is low or weights are extreme, the offline estimate becomes fragile.

This is why mature recommender platforms log propensities and maintain exploration traffic.

def weight_diagnostics(logged, target_actions):

logged_action = logged["item_id"].to_numpy()

weights = (logged_action == target_actions).astype(float) / logged["propensity"].to_numpy()

positive = weights[weights > 0]

return pd.DataFrame(

{

"metric": [

"Match rate",

"Mean positive weight",

"95th percentile positive weight",

"Max positive weight",

"Effective sample size",

"Effective sample share",

],

"value": [

(weights > 0).mean(),

positive.mean(),

np.quantile(positive, 0.95),

positive.max(),

(weights.sum() ** 2) / np.sum(weights**2),

((weights.sum() ** 2) / np.sum(weights**2)) / len(weights),

],

}

), weights

diag_click, weights_click = weight_diagnostics(logged, click_policy_action)

diag_profit, weights_profit = weight_diagnostics(logged, profit_policy_action)

diag_click["policy"] = "Click-max policy"

diag_profit["policy"] = "Profit-aware policy"

weight_diag = pd.concat([diag_click, diag_profit], ignore_index=True)

display(weight_diag.pivot(index="metric", columns="policy", values="value").reset_index())| policy | metric | Click-max policy | Profit-aware policy |

|---|---|---|---|

| 0 | 95th percentile positive weight | 15.070827 | 10.061802 |

| 1 | Effective sample share | 0.092133 | 0.136398 |

| 2 | Effective sample size | 6449.281277 | 9547.848601 |

| 3 | Match rate | 0.106857 | 0.140343 |

| 4 | Max positive weight | 16.313727 | 15.346105 |

| 5 | Mean positive weight | 9.374935 | 6.958124 |

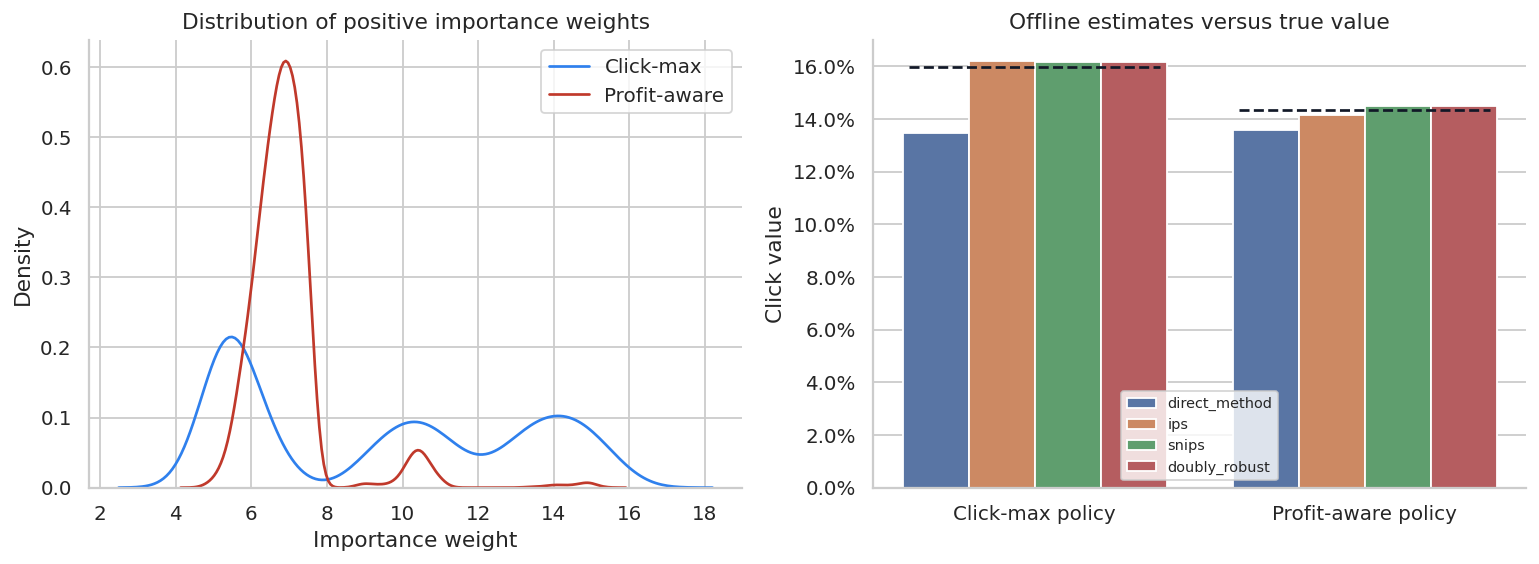

fig, axes = plt.subplots(1, 2, figsize=(12, 4.5))

for weights, label, color in [

(weights_click, "Click-max", "#2F80ED"),

(weights_profit, "Profit-aware", "#C0392B"),

]:

positive = weights[weights > 0]

sns.kdeplot(positive, ax=axes[0], label=label, color=color)

axes[0].set_title("Distribution of positive importance weights")

axes[0].set_xlabel("Importance weight")

axes[0].legend()

compare = ope_click_table.melt(

id_vars=["policy", "true_value"],

value_vars=["direct_method", "ips", "snips", "doubly_robust"],

var_name="estimator",

value_name="estimated_value",

)

sns.barplot(data=compare, x="policy", y="estimated_value", hue="estimator", ax=axes[1])

for i, policy in enumerate(compare["policy"].unique()):

true_val = compare.loc[compare["policy"].eq(policy), "true_value"].iloc[0]

axes[1].hlines(true_val, i - 0.38, i + 0.38, colors="#111827", linestyles="--")

axes[1].set_title("Offline estimates versus true value")

axes[1].set_xlabel("")

axes[1].set_ylabel("Click value")

axes[1].yaxis.set_major_formatter(lambda x, pos: f"{100*x:.1f}%")

axes[1].legend(title="", fontsize=8)

plt.tight_layout()

plt.show()

This plot makes the central practical point:

- direct method can be biased if the reward model extrapolates poorly,

- IPS is unbiased under correct propensities and support, but can have high variance,

- SNIPS often reduces variance at the cost of some bias,

- doubly robust can be more stable when either the reward model or propensity logic is good enough.

None of these methods remove the need for an online experiment before major launch.

7. Profit-Aware Recommendation

Clicks are often not the real objective. An e-commerce system may care about contribution profit, long-term retention, customer satisfaction, inventory, or supplier fairness.

Here we estimate the value of the profit-aware policy using observed profit. We need a separate outcome model for profit if using DR on profit. For simplicity, we will compare IPS and SNIPS, then use an outcome model for expected profit.

profit_model = Pipeline(

steps=[

("preprocess", preprocess),

(

"model",

HistGradientBoostingClassifier(

max_iter=100,

learning_rate=0.06,

max_leaf_nodes=18,

random_state=11,

),

),

]

)

# Convert profit to a binary purchase proxy for model stability, then multiply by item margin in policy evaluation.

logged["purchase"] = (logged["profit"] > 0).astype(int)

profit_model.fit(logged[feature_cols], logged["purchase"])

q_purchase_matrix = predict_q_for_actions(contexts, catalog, profit_model)

q_profit_matrix = q_purchase_matrix * catalog["margin"].to_numpy()[None, :]

def ope_profit_for_policy(logged, target_actions, q_profit_matrix):

logged_action = logged["item_id"].to_numpy()

mu = logged["propensity"].to_numpy()

reward = logged["profit"].to_numpy()

n = len(logged)

weights = (logged_action == target_actions).astype(float) / mu

direct = q_profit_matrix[np.arange(n), target_actions].mean()

ips = np.mean(weights * reward)

snips = np.sum(weights * reward) / np.sum(weights)

dr = np.mean(

q_profit_matrix[np.arange(n), target_actions]

+ weights * (reward - q_profit_matrix[np.arange(n), logged_action])

)

return direct, ips, snips, dr

profit_eval_rows = []

for name, actions in [

("Click-max policy", click_policy_action),

("Profit-aware policy", profit_policy_action),

]:

direct, ips, snips, dr = ope_profit_for_policy(logged, actions, q_profit_matrix)

true_profit_value = true_profit[np.arange(len(contexts)), actions].mean()

profit_eval_rows.append(

{

"policy": name,

"true_profit_value": true_profit_value,

"direct_method": direct,

"ips": ips,

"snips": snips,

"doubly_robust": dr,

}

)

profit_eval = pd.DataFrame(profit_eval_rows)

display(

styled_table(

profit_eval,

money_cols=["true_profit_value", "direct_method", "ips", "snips", "doubly_robust"],

)

)| policy | true_profit_value | direct_method | ips | snips | doubly_robust | |

|---|---|---|---|---|---|---|

| 0 | Click-max policy | $3.61 | $3.05 | $3.61 | $3.60 | $3.61 |

| 1 | Profit-aware policy | $4.54 | $4.35 | $4.50 | $4.61 | $4.61 |

A ranking policy should be evaluated against the business objective, not just the easiest label. If click-max increases clicks but shifts traffic toward low-margin items, it may look good in a product analytics dashboard while hurting contribution profit.

8. Position Bias in Ranked Lists

Now move from one top-slot recommendation to a ranked list.

In a ranked interface, an item can receive more clicks because it is more relevant or because it was placed higher. Let:

\[ C_{ij} = E_{ij} \cdot R_{ij} \]

where:

- \(C_{ij}\) is whether user \(i\) clicked item \(j\),

- \(E_{ij}\) is whether the user examined the position,

- \(R_{ij}\) is whether the item was relevant enough to click if examined.

If examination probability differs by rank, naive click-through rate is a biased relevance label.

def simulate_ranked_logs(contexts, catalog, true_reward, top_k=5, n_sessions=35_000, seed=55):

local_rng = np.random.default_rng(seed)

subset_idx = local_rng.choice(len(contexts), size=n_sessions, replace=False)

ctx = contexts.iloc[subset_idx].reset_index(drop=True)

rewards = true_reward[subset_idx]

# Production ranker favors popularity and relevance.

rank_score = 1.6 * rewards + 0.85 * catalog["popularity"].to_numpy()[None, :]

rankings = np.argsort(-rank_score, axis=1)[:, :top_k]

exam_prob_by_position = np.array([0.90, 0.62, 0.43, 0.30, 0.20])

rows = []

for i in range(n_sessions):

for pos in range(top_k):

item = rankings[i, pos]

relevance = rewards[i, item]

exam_prob = exam_prob_by_position[pos]

click_prob = exam_prob * relevance

click = local_rng.binomial(1, click_prob)

rows.append(

{

"session_id": i,

"segment": ctx.loc[i, "segment"],

"position": pos + 1,

"item_id": item,

"examination_prob": exam_prob,

"true_relevance": relevance,

"click": click,

}

)

return pd.DataFrame(rows)

rank_logs = simulate_ranked_logs(contexts, catalog, true_reward)

display(rank_logs.head())

print(f"Rows: {len(rank_logs):,}")

print(f"Sessions: {rank_logs['session_id'].nunique():,}")| session_id | segment | position | item_id | examination_prob | true_relevance | click | |

|---|---|---|---|---|---|---|---|

| 0 | 0 | loyalist | 1 | 4 | 0.90 | 0.110160 | 0 |

| 1 | 0 | loyalist | 2 | 1 | 0.62 | 0.117660 | 0 |

| 2 | 0 | loyalist | 3 | 2 | 0.43 | 0.058435 | 0 |

| 3 | 0 | loyalist | 4 | 5 | 0.30 | 0.147432 | 0 |

| 4 | 0 | loyalist | 5 | 11 | 0.20 | 0.048940 | 0 |

Rows: 175,000

Sessions: 35,000position_summary = (

rank_logs.groupby("position")

.agg(

rows=("click", "size"),

observed_ctr=("click", "mean"),

mean_true_relevance=("true_relevance", "mean"),

examination_prob=("examination_prob", "mean"),

)

.reset_index()

)

display(styled_table(position_summary, pct_cols=["observed_ctr", "mean_true_relevance", "examination_prob"]))| position | rows | observed_ctr | mean_true_relevance | examination_prob | |

|---|---|---|---|---|---|

| 0 | 1 | 35000 | 11.98% | 13.38% | 90.00% |

| 1 | 2 | 35000 | 8.77% | 14.56% | 62.00% |

| 2 | 3 | 35000 | 4.50% | 10.42% | 43.00% |

| 3 | 4 | 35000 | 2.63% | 9.10% | 30.00% |

| 4 | 5 | 35000 | 1.79% | 8.60% | 20.00% |

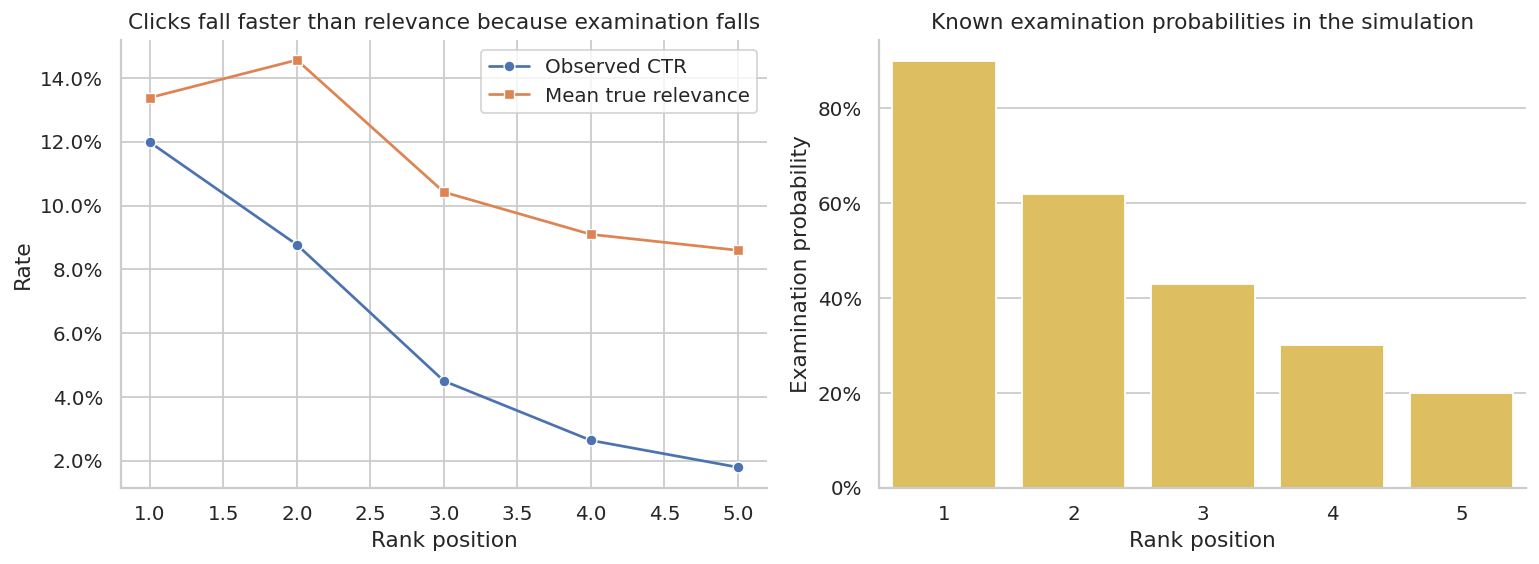

fig, axes = plt.subplots(1, 2, figsize=(12, 4.5))

sns.lineplot(data=position_summary, x="position", y="observed_ctr", marker="o", ax=axes[0], label="Observed CTR")

sns.lineplot(data=position_summary, x="position", y="mean_true_relevance", marker="s", ax=axes[0], label="Mean true relevance")

axes[0].set_title("Clicks fall faster than relevance because examination falls")

axes[0].set_xlabel("Rank position")

axes[0].set_ylabel("Rate")

axes[0].yaxis.set_major_formatter(lambda x, pos: f"{100*x:.1f}%")

axes[0].legend()

sns.barplot(data=position_summary, x="position", y="examination_prob", ax=axes[1], color="#F2C94C")

axes[1].set_title("Known examination probabilities in the simulation")

axes[1].set_xlabel("Rank position")

axes[1].set_ylabel("Examination probability")

axes[1].yaxis.set_major_formatter(lambda x, pos: f"{100*x:.0f}%")

plt.tight_layout()

plt.show()

The top position gets many more clicks partly because it is examined more often. Treating clicks as direct relevance labels would over-credit higher positions and under-credit lower positions.

item_rank_summary = (

rank_logs.groupby("item_id")

.agg(

exposures=("click", "size"),

avg_position=("position", "mean"),

naive_ctr=("click", "mean"),

ips_relevance_estimate=("click", lambda x: np.nan),

true_relevance=("true_relevance", "mean"),

)

.reset_index()

)

ips_by_item = (

rank_logs.assign(weighted_click=lambda d: d["click"] / d["examination_prob"])

.groupby("item_id")

.agg(ips_relevance_estimate=("weighted_click", "mean"))

.reset_index()

)

item_rank_summary = item_rank_summary.drop(columns=["ips_relevance_estimate"]).merge(ips_by_item, on="item_id")

item_rank_summary = item_rank_summary.merge(catalog[["item_id", "category", "popularity"]], on="item_id")

display(

styled_table(

item_rank_summary.sort_values("avg_position"),

pct_cols=["naive_ctr", "ips_relevance_estimate", "true_relevance"],

num_cols=["avg_position", "popularity"],

)

)| item_id | exposures | avg_position | naive_ctr | true_relevance | ips_relevance_estimate | category | popularity | |

|---|---|---|---|---|---|---|---|---|

| 2 | 4 | 35000 | 1.000 | 11.98% | 13.38% | 13.31% | fashion | 0.838 |

| 0 | 1 | 35000 | 2.000 | 8.77% | 14.56% | 14.15% | home | 0.640 |

| 1 | 2 | 34821 | 3.459 | 2.25% | 6.59% | 6.18% | beauty | 0.561 |

| 3 | 5 | 15269 | 3.856 | 6.33% | 18.55% | 18.58% | books | 0.375 |

| 4 | 6 | 10023 | 4.119 | 4.76% | 14.50% | 14.82% | grocery | 0.357 |

| 7 | 11 | 31535 | 4.316 | 1.88% | 6.48% | 6.65% | sports | 0.518 |

| 5 | 8 | 13301 | 4.739 | 2.28% | 9.04% | 9.74% | electronics | 0.463 |

| 6 | 10 | 51 | 5.000 | 1.96% | 27.50% | 9.80% | beauty | 0.256 |

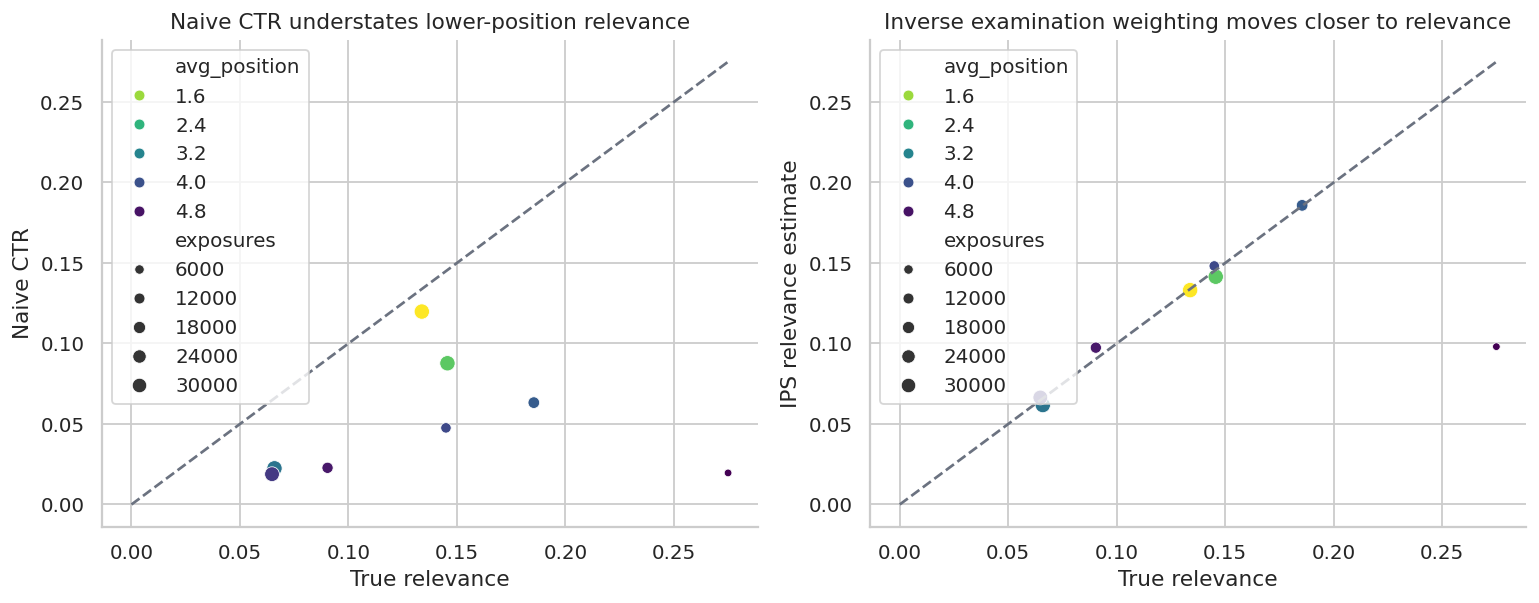

fig, axes = plt.subplots(1, 2, figsize=(12, 4.8))

sns.scatterplot(

data=item_rank_summary,

x="true_relevance",

y="naive_ctr",

size="exposures",

hue="avg_position",

palette="viridis_r",

ax=axes[0],

)

axes[0].plot([0, item_rank_summary["true_relevance"].max()], [0, item_rank_summary["true_relevance"].max()], "--", color="#6B7280")

axes[0].set_title("Naive CTR understates lower-position relevance")

axes[0].set_xlabel("True relevance")

axes[0].set_ylabel("Naive CTR")

sns.scatterplot(

data=item_rank_summary,

x="true_relevance",

y="ips_relevance_estimate",

size="exposures",

hue="avg_position",

palette="viridis_r",

ax=axes[1],

)

axes[1].plot([0, item_rank_summary["true_relevance"].max()], [0, item_rank_summary["true_relevance"].max()], "--", color="#6B7280")

axes[1].set_title("Inverse examination weighting moves closer to relevance")

axes[1].set_xlabel("True relevance")

axes[1].set_ylabel("IPS relevance estimate")

plt.tight_layout()

plt.show()

This simple correction uses known examination propensities. In real systems, propensities are often estimated from randomized swaps, interleaving experiments, eye-tracking studies, or click models. If the examination model is wrong, the correction can still be biased.

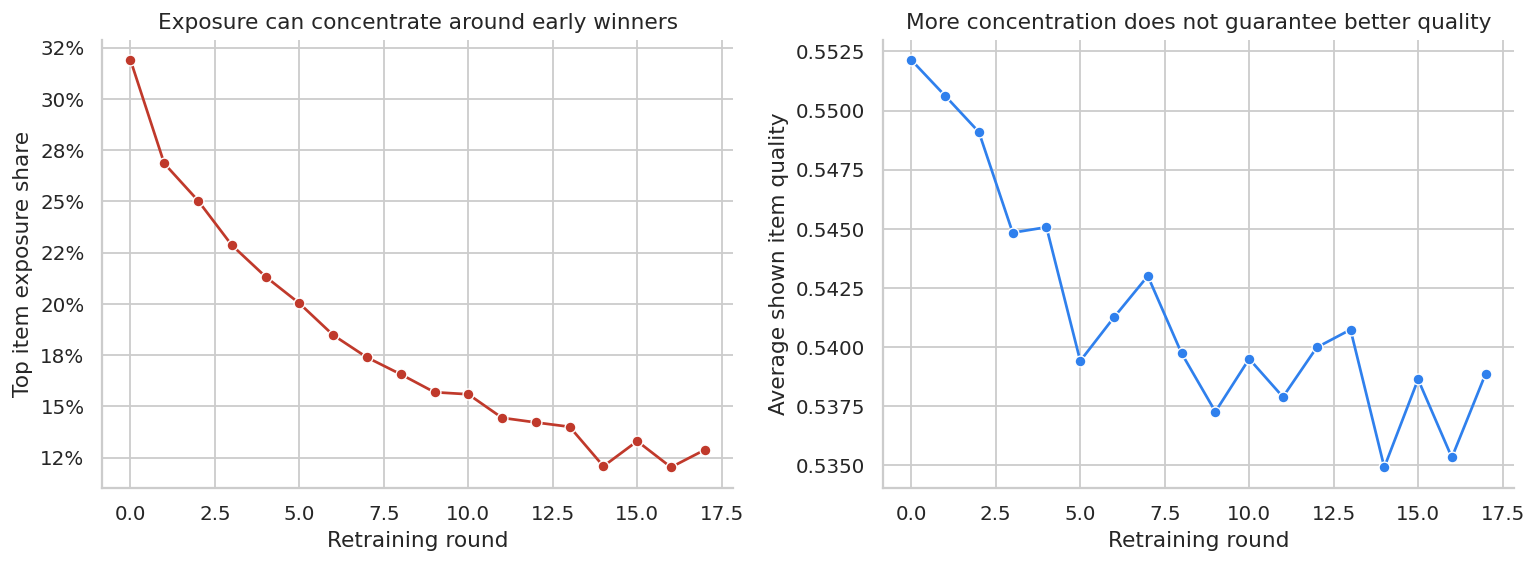

9. Feedback Loops and Exposure Concentration

Recommendation systems can create their own evidence.

If the next model trains on clicks from the current model, then exposed items get more labels and hidden items remain uncertain. A popularity-based retraining loop can concentrate exposure over time.

def simulate_feedback_loop(catalog, rounds=18, impressions_per_round=8_000, seed=70):

local_rng = np.random.default_rng(seed)

item_quality = expit(catalog["quality"].to_numpy())

popularity_score = catalog["popularity"].to_numpy().copy()

records = []

for t in range(rounds):

score = 0.35 * item_quality + 0.65 * popularity_score

probs = softmax(score / 0.20)

shown = local_rng.choice(len(catalog), size=impressions_per_round, p=probs)

click_prob = item_quality[shown] * 0.12

clicks = local_rng.binomial(1, click_prob)

counts = np.bincount(shown, minlength=len(catalog))

click_counts = np.bincount(shown, weights=clicks, minlength=len(catalog))

# Update popularity using observed clicks.

popularity_score = 0.88 * popularity_score + 0.12 * (click_counts + 1) / (counts + 10)

exposure_share = counts / counts.sum()

top_item_share = exposure_share.max()

herfindahl = np.sum(exposure_share**2)

avg_quality_shown = np.average(item_quality, weights=exposure_share)

records.append(

{

"round": t,

"top_item_exposure_share": top_item_share,

"exposure_concentration_hhi": herfindahl,

"avg_quality_shown": avg_quality_shown,

}

)

return pd.DataFrame(records)

feedback = simulate_feedback_loop(catalog)

display(feedback.head())| round | top_item_exposure_share | exposure_concentration_hhi | avg_quality_shown | |

|---|---|---|---|---|

| 0 | 0 | 0.319000 | 0.157876 | 0.552139 |

| 1 | 1 | 0.268500 | 0.135100 | 0.550626 |

| 2 | 2 | 0.250375 | 0.125967 | 0.549092 |

| 3 | 3 | 0.228625 | 0.116758 | 0.544836 |

| 4 | 4 | 0.213250 | 0.110587 | 0.545068 |

fig, axes = plt.subplots(1, 2, figsize=(12, 4.5))

sns.lineplot(data=feedback, x="round", y="top_item_exposure_share", marker="o", ax=axes[0], color="#C0392B")

axes[0].set_title("Exposure can concentrate around early winners")

axes[0].set_xlabel("Retraining round")

axes[0].set_ylabel("Top item exposure share")

axes[0].yaxis.set_major_formatter(lambda x, pos: f"{100*x:.0f}%")

sns.lineplot(data=feedback, x="round", y="avg_quality_shown", marker="o", ax=axes[1], color="#2F80ED")

axes[1].set_title("More concentration does not guarantee better quality")

axes[1].set_xlabel("Retraining round")

axes[1].set_ylabel("Average shown item quality")

plt.tight_layout()

plt.show()

Feedback loops are not solved by better predictive modeling alone. They require exploration, counterfactual evaluation, guardrails, and sometimes explicit diversity constraints.

10. Online Experiment Readout

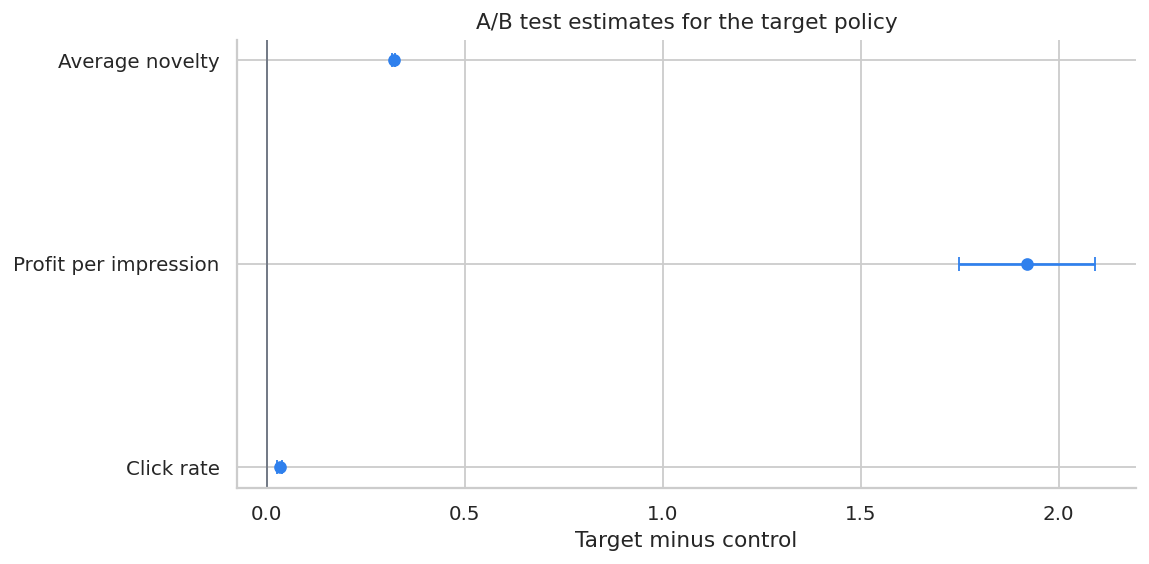

Offline OPE is a screening tool. For a meaningful product launch, the final answer should come from an online experiment when feasible.

We will simulate a simple A/B test comparing the logging policy with the profit-aware policy.

def simulate_ab_test(contexts, catalog, true_reward, true_profit, n=50_000, seed=88):

local_rng = np.random.default_rng(seed)

idx = local_rng.choice(len(contexts), n, replace=False)

group = local_rng.binomial(1, 0.5, size=n)

behavior_probs_test = behavior_probs[idx]

logging_actions = np.array([local_rng.choice(len(catalog), p=p) for p in behavior_probs_test])

target_actions = true_profit[idx].argmax(axis=1)

actions = np.where(group == 1, target_actions, logging_actions)

click_prob = true_reward[idx, actions]

clicks = local_rng.binomial(1, click_prob)

profit = clicks * catalog.loc[actions, "margin"].to_numpy()

novelty = catalog.loc[actions, "novelty"].to_numpy()

category = catalog.loc[actions, "category"].to_numpy()

return pd.DataFrame(

{

"group": np.where(group == 1, "Profit-aware target", "Logging control"),

"item_id": actions,

"category": category,

"click": clicks,

"profit": profit,

"novelty": novelty,

}

)

ab = simulate_ab_test(contexts, catalog, true_reward, true_profit)

ab_summary = (

ab.groupby("group")

.agg(

impressions=("click", "size"),

click_rate=("click", "mean"),

profit_per_impression=("profit", "mean"),

avg_novelty=("novelty", "mean"),

category_diversity=("category", lambda x: 1 - np.sum((x.value_counts(normalize=True) ** 2))),

)

.reset_index()

)

display(styled_table(ab_summary, pct_cols=["click_rate"], money_cols=["profit_per_impression"], num_cols=["avg_novelty", "category_diversity"]))| group | impressions | click_rate | profit_per_impression | avg_novelty | category_diversity | |

|---|---|---|---|---|---|---|

| 0 | Logging control | 24833 | 11.15% | $2.67 | 0.434 | 0.856 |

| 1 | Profit-aware target | 25167 | 14.50% | $4.59 | 0.755 | 0.177 |

def diff_in_means_ci(df, outcome, treatment_label="Profit-aware target", control_label="Logging control"):

t = df.loc[df["group"].eq(treatment_label), outcome].to_numpy()

c = df.loc[df["group"].eq(control_label), outcome].to_numpy()

diff = t.mean() - c.mean()

se = np.sqrt(t.var(ddof=1) / len(t) + c.var(ddof=1) / len(c))

return diff, diff - 1.96 * se, diff + 1.96 * se

ab_effects = []

for outcome in ["click", "profit", "novelty"]:

diff, lo, hi = diff_in_means_ci(ab, outcome)

ab_effects.append({"outcome": outcome, "lift": diff, "ci_low": lo, "ci_high": hi})

ab_effects = pd.DataFrame(ab_effects)

display(ab_effects)| outcome | lift | ci_low | ci_high | |

|---|---|---|---|---|

| 0 | click | 0.033407 | 0.027554 | 0.039259 |

| 1 | profit | 1.920929 | 1.749178 | 2.092681 |

| 2 | novelty | 0.320962 | 0.317516 | 0.324408 |

fig, ax = plt.subplots(figsize=(9, 4.5))

plot_effects = ab_effects.copy()

plot_effects["outcome"] = plot_effects["outcome"].map(

{"click": "Click rate", "profit": "Profit per impression", "novelty": "Average novelty"}

)

plot_effects["y"] = np.arange(len(plot_effects))

ax.errorbar(

plot_effects["lift"],

plot_effects["y"],

xerr=[plot_effects["lift"] - plot_effects["ci_low"], plot_effects["ci_high"] - plot_effects["lift"]],

fmt="o",

color="#2F80ED",

capsize=4,

)

ax.axvline(0, color="#6B7280", linewidth=1)

ax.set_yticks(plot_effects["y"])

ax.set_yticklabels(plot_effects["outcome"])

ax.set_title("A/B test estimates for the target policy")

ax.set_xlabel("Target minus control")

plt.tight_layout()

plt.show()

This A/B test directly estimates the policy effect in the deployment environment. Offline estimates helped decide whether the policy was worth testing; the online test provides the launch evidence.

11. Practical Diagnostics

A recommendation policy should not move from offline analysis to launch without diagnostics.

diagnostics = pd.DataFrame(

[

{

"diagnostic": "Propensity logging",

"question": "Do logs contain the exact probability of the shown action?",

"failure mode": "IPS and DR cannot be trusted without behavior propensities.",

},

{

"diagnostic": "Common support",

"question": "Does the logging policy sometimes choose actions the target policy would choose?",

"failure mode": "Offline estimates extrapolate into unsupported regions.",

},

{

"diagnostic": "Effective sample size",

"question": "How many weighted observations really identify the target policy?",

"failure mode": "A large log can become a small effective experiment.",

},

{

"diagnostic": "Weight tails",

"question": "Are a few impressions carrying most of the IPS estimate?",

"failure mode": "High variance and unstable conclusions.",

},

{

"diagnostic": "Position bias",

"question": "Can we separate examination from relevance?",

"failure mode": "Top positions look better just because users see them.",

},

{

"diagnostic": "Objective alignment",

"question": "Are we optimizing clicks, profit, retention, satisfaction, or long-term value?",

"failure mode": "The model improves an easy metric while harming the real objective.",

},

{

"diagnostic": "Guardrails",

"question": "What happens to diversity, creator exposure, inventory, latency, and complaint rate?",

"failure mode": "The recommender wins the primary metric but damages the ecosystem.",

},

]

)

display(diagnostics)| diagnostic | question | failure mode | |

|---|---|---|---|

| 0 | Propensity logging | Do logs contain the exact probability of the s... | IPS and DR cannot be trusted without behavior ... |

| 1 | Common support | Does the logging policy sometimes choose actio... | Offline estimates extrapolate into unsupported... |

| 2 | Effective sample size | How many weighted observations really identify... | A large log can become a small effective exper... |

| 3 | Weight tails | Are a few impressions carrying most of the IPS... | High variance and unstable conclusions. |

| 4 | Position bias | Can we separate examination from relevance? | Top positions look better just because users s... |

| 5 | Objective alignment | Are we optimizing clicks, profit, retention, s... | The model improves an easy metric while harmin... |

| 6 | Guardrails | What happens to diversity, creator exposure, i... | The recommender wins the primary metric but da... |

12. Decision Memo Template

Below is a compact readout that combines offline OPE with the online experiment recommendation.

profit_row = profit_eval.loc[profit_eval["policy"].eq("Profit-aware policy")].iloc[0]

logging_profit = true_values.loc[true_values["policy"].eq("Logging policy"), "true_profit_value"].iloc[0]

offline_dr_lift = profit_row["doubly_robust"] - logging_profit

ab_profit = ab_effects.loc[ab_effects["outcome"].eq("profit")].iloc[0]

ess_profit = weight_diagnostics(logged, profit_policy_action)[0].query("metric == 'Effective sample size'")["value"].iloc[0]

memo = f'''

### Recommendation Policy Readout

**Decision:** Whether to advance the profit-aware recommender from offline evaluation to broader online testing.

**Current policy:** Production logging policy with stochastic exploration.

**Candidate policy:** Profit-aware top-slot recommender.

**Offline OPE:** Doubly robust estimated profit value for the candidate is {dollars(profit_row["doubly_robust"], 3)} per impression.

**Estimated offline lift versus logging policy:** {dollars(offline_dr_lift, 3)} per impression.

**Support diagnostic:** Effective sample size for the candidate policy is {ess_profit:,.0f} impressions out of {len(logged):,} logged impressions.

**Online experiment result:** A/B profit lift is {dollars(ab_profit["lift"], 3)} per impression with 95% CI [{dollars(ab_profit["ci_low"], 3)}, {dollars(ab_profit["ci_high"], 3)}].

**Recommendation:** Continue staged rollout if guardrails remain stable; keep exploration traffic active so future candidate policies remain evaluable.

**Caveats:** Monitor diversity, item exposure concentration, customer satisfaction, long-term retention, and support gaps for new or rarely shown items.

'''

display(Markdown(memo))Recommendation Policy Readout

Decision: Whether to advance the profit-aware recommender from offline evaluation to broader online testing.

Current policy: Production logging policy with stochastic exploration.

Candidate policy: Profit-aware top-slot recommender.

Offline OPE: Doubly robust estimated profit value for the candidate is $4.615 per impression.

Estimated offline lift versus logging policy: $1.938 per impression.

Support diagnostic: Effective sample size for the candidate policy is 9,548 impressions out of 70,000 logged impressions.

Online experiment result: A/B profit lift is $1.921 per impression with 95% CI [$1.749, $2.093].

Recommendation: Continue staged rollout if guardrails remain stable; keep exploration traffic active so future candidate policies remain evaluable.

Caveats: Monitor diversity, item exposure concentration, customer satisfaction, long-term retention, and support gaps for new or rarely shown items.

A senior readout should separate three claims:

- Offline evidence: the candidate looks promising under OPE.

- Identification risk: support, propensities, position bias, and reward modeling are plausible but imperfect.

- Deployment decision: online experimentation and guardrails decide launch.

13. Practical Workflow

A strong causal recommender workflow usually looks like this:

- Define the decision policy and the business objective.

- Log action propensities for every recommendation or ranking.

- Maintain exploration traffic so future policies have support.

- Store context, candidate set, action, position, layout, propensity, and reward.

- Estimate direct, IPS, SNIPS, and DR values.

- Report match rate, weight distribution, and effective sample size.

- Correct ranking feedback for position or examination bias.

- Check guardrails: diversity, fairness, inventory, latency, long-term retention.

- Use OPE as a screen, not a final launch decision.

- Validate with an online experiment before broad rollout.

Hands-On Extensions

Try extending this notebook in the following ways:

- Replace the deterministic target policies with stochastic target policies.

- Add a slate policy that recommends three items at once.

- Estimate propensities instead of using known logged propensities.

- Add delayed rewards such as 7-day retention or repeat purchase.

- Add a constraint that limits exposure concentration for any one item.

- Compare IPS with clipped IPS and SWITCH-style estimators.

- Train a CATE model to personalize exploration rates.

Key Takeaways

- Recommender systems create the data used to train and evaluate future recommenders.

- Historical clicks are biased by selection, position, trust, and feedback loops.

- Policy value is a causal estimand: what reward would happen under a target policy?

- IPS uses logged propensities to correct distribution mismatch.

- SNIPS and DR can improve finite-sample stability, but they require diagnostics.

- Position bias means click probability is not relevance probability.

- Exploration is an asset because it creates support for future policy evaluation.

- Offline OPE should screen policies before online experimentation, not replace A/B tests.

References

Jagerman, R., & de Rijke, M. (2020). Accelerated convergence for counterfactual learning to rank. Proceedings of the 43rd International ACM SIGIR Conference on Research and Development in Information Retrieval, 469-478. https://doi.org/10.1145/3397271.3401069

Joachims, T., & Swaminathan, A. (2016). Counterfactual evaluation and learning for search, recommendation and ad placement. Proceedings of the 39th International ACM SIGIR Conference on Research and Development in Information Retrieval, 1199-1201. https://doi.org/10.1145/2911451.2914803

Kiyohara, H., Saito, Y., & Matsuhiro, T. (2022). Doubly robust off-policy evaluation for ranking policies under the cascade behavior model. Proceedings of the Fifteenth ACM International Conference on Web Search and Data Mining, 487-497. https://doi.org/10.1145/3488560.3498380

Saito, Y., Aihara, S., & Matsutani, M. (2020). Open bandit dataset and pipeline: Towards realistic and reproducible off-policy evaluation. arXiv. https://doi.org/10.48550/arxiv.2008.07146

Saito, Y., & Joachims, T. (2022). Off-policy evaluation for large action spaces via embeddings. arXiv. https://doi.org/10.48550/arxiv.2202.06317

Su, Y., Dimakopoulou, M., & Krishnamurthy, A. (2019). Doubly robust off-policy evaluation with shrinkage. arXiv. https://doi.org/10.48550/arxiv.1907.09623

Vardasbi, A., Oosterhuis, H., & de Rijke, M. (2020). When inverse propensity scoring does not work. Proceedings of the 29th ACM International Conference on Information & Knowledge Management, 1475-1484. https://doi.org/10.1145/3340531.3412031