import warnings

import graphviz

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import seaborn as sns

from IPython.display import display

from sklearn.base import clone

from sklearn.ensemble import HistGradientBoostingClassifier, HistGradientBoostingRegressor, RandomForestRegressor

from sklearn.linear_model import RidgeCV

from sklearn.metrics import mean_squared_error, r2_score, roc_auc_score

from sklearn.model_selection import KFold, train_test_split

from sklearn.pipeline import make_pipeline

from sklearn.preprocessing import StandardScaler

warnings.filterwarnings("ignore")

sns.set_theme(style="whitegrid", context="notebook")

pd.set_option("display.float_format", "{:.3f}".format)08. Causal ML Model Validation

Causal machine learning is hard to validate because the object we most want to predict is usually unobserved.

For an outcome model, validation is familiar: compare predicted outcomes to observed outcomes. For a CATE model, the target is:

\[ \tau(x) = E[Y(1)-Y(0)\mid X=x] \]

But for each individual we only observe one potential outcome. We do not observe both \(Y(1)\) and \(Y(0)\) for the same unit. That means ordinary prediction validation is not enough.

This notebook is a practical validation playbook for causal ML in industry. We will use simulation truth to learn what good validation looks like, then emphasize the diagnostics that remain available in real projects.

Learning Goals

By the end of this notebook, you should be able to:

- Explain why outcome-prediction accuracy is not the same as treatment-effect accuracy.

- Use simulation-only metrics such as PEHE to understand estimator behavior.

- Use held-out R-loss as a practical model-selection criterion.

- Validate CATE ranking with uplift and targeting curves.

- Estimate calibration of treatment-effect scores with doubly robust pseudo-outcomes.

- Evaluate top-k policy value under capacity constraints.

- Run placebo, stability, overlap, and drift checks before deployment.

- Translate causal ML validation into a professional model-risk readout.

def sigmoid(x):

return 1 / (1 + np.exp(-x))

def make_dag(edges, title=None, node_colors=None, rankdir="LR"):

graph = graphviz.Digraph(format="svg")

graph.attr(rankdir=rankdir, bgcolor="white", pad="0.2")

graph.attr("node", shape="box", style="rounded,filled", color="#334155", fontname="Helvetica")

graph.attr("edge", color="#475569", arrowsize="0.8")

node_colors = node_colors or {}

nodes = sorted({node for edge in edges for node in edge[:2]})

for node in nodes:

graph.node(node, fillcolor=node_colors.get(node, "#eef2ff"))

for edge in edges:

if len(edge) == 2:

graph.edge(edge[0], edge[1])

else:

graph.edge(edge[0], edge[1], label=edge[2])

if title:

graph.attr(label=title, labelloc="t", fontsize="18", fontname="Helvetica-Bold")

return graph

def top_fraction_mask(scores, fraction, require_positive=False):

scores = np.asarray(scores)

if fraction <= 0:

return np.zeros(len(scores), dtype=int)

if fraction >= 1:

mask = np.ones(len(scores), dtype=int)

else:

threshold = np.quantile(scores, 1 - fraction)

mask = (scores >= threshold).astype(int)

if require_positive:

mask = mask * (scores > 0).astype(int)

return mask

def bootstrap_ci(values, seed=1, n_boot=500, alpha=0.05):

rng = np.random.default_rng(seed)

values = np.asarray(values)

boot = []

for _ in range(n_boot):

idx = rng.integers(0, len(values), len(values))

boot.append(values[idx].mean())

return np.quantile(boot, [alpha / 2, 1 - alpha / 2])1. Why Causal ML Validation Is Different

The fundamental problem is that treatment effects are not directly observed. We observe:

\[ Y = WY(1) + (1-W)Y(0) \]

but the individual effect:

\[ Y(1)-Y(0) \]

is never observed for the same unit.

This creates a validation trap. A model can predict outcomes well while being bad at treatment effects. Outcome prediction mainly rewards learning the baseline outcome function:

\[ m(x)=E[Y\mid X=x] \]

Causal personalization needs the difference between potential outcomes:

\[ \tau(x)=E[Y(1)-Y(0)\mid X=x] \]

These are related but not the same target. Rothenhausler (2020) emphasizes that ordinary predictive cross-validation can select models that are not optimal for causal parameters. Gao et al. (2020) also describe the central difficulty: HTE accuracy is hard to assess because HTE itself is invisible in ordinary validation data.

make_dag(

edges=[

("Features", "TreatmentAssignment"),

("Features", "BaselineOutcome"),

("Features", "TreatmentEffect"),

("TreatmentAssignment", "ObservedOutcome"),

("BaselineOutcome", "ObservedOutcome"),

("TreatmentEffect", "ObservedOutcome"),

("ObservedOutcome", "OutcomePredictionMetrics"),

("UnobservedCounterfactual", "CausalValidationProblem"),

("TreatmentEffect", "CausalValidationProblem"),

],

title="Outcome validation sees Y, but treatment-effect validation targets an unobserved contrast",

node_colors={

"Features": "#dbeafe",

"TreatmentAssignment": "#fef3c7",

"BaselineOutcome": "#dcfce7",

"TreatmentEffect": "#ede9fe",

"ObservedOutcome": "#f1f5f9",

"OutcomePredictionMetrics": "#cffafe",

"UnobservedCounterfactual": "#fee2e2",

"CausalValidationProblem": "#fce7f3",

},

)

2. Validation Targets

A causal ML validation plan usually separates five questions:

- Identification: are the causal assumptions plausible?

- Nuisance quality: are propensity and outcome models usable?

- Effect estimation: do CATE scores estimate effect magnitudes?

- Ranking quality: do high-scored units really have larger effects?

- Decision value: does the treatment policy improve outcomes after costs and constraints?

In simulation, we can directly check CATE error:

\[ PEHE = \sqrt{\frac{1}{n}\sum_i(\hat{\tau}(X_i)-\tau(X_i))^2} \]

In real data, PEHE is unavailable. We use proxies: R-loss, doubly robust calibration, uplift curves, policy value, placebo checks, stability checks, and prospective experiments.

3. Running Example: Promotional Retention Campaign

Imagine a subscription company deciding who should receive a retention promotion. The outcome is next-period account value. The treatment is a promotion plus outreach workflow.

The true effect is heterogeneous:

- Some high-risk, high-value accounts are persuadable.

- Some very unhealthy accounts are hard to save.

- Some low-risk accounts would renew anyway.

- Some discount-sensitive customers respond to incentives.

We will simulate observational data with confounding, then fit several causal ML scores and validate them on held-out data.

def simulate_campaign_data(n=11000, seed=5808, shifted=False):

rng = np.random.default_rng(seed)

churn_risk = rng.beta(2.2, 2.5, n)

product_health = rng.beta(2.6, 2.1, n)

discount_sensitivity = rng.beta(2.1, 2.7, n)

usage_depth = rng.normal(0, 1, n)

log_mrr = rng.normal(4.4, 0.62, n)

mrr_z = (log_mrr - log_mrr.mean()) / log_mrr.std()

enterprise = rng.binomial(1, sigmoid(-0.35 + 0.9 * mrr_z + 0.35 * churn_risk), n)

onboarding_gap = rng.beta(1.8, 3.1, n)

support_load = rng.poisson(np.clip(0.3 + 3.1 * churn_risk - 0.8 * product_health + 0.7 * enterprise, 0.05, None))

region_west = rng.binomial(1, 0.33, n)

region_emea = rng.binomial(1, 0.27, n) * (1 - region_west)

if shifted:

churn_risk = np.clip(0.08 + 0.92 * churn_risk, 0, 1)

product_health = np.clip(product_health - 0.08 + rng.normal(0, 0.03, n), 0, 1)

discount_sensitivity = np.clip(discount_sensitivity + 0.07, 0, 1)

support_load = support_load + rng.poisson(0.35, n)

severe_risk = ((churn_risk > 0.78) & (product_health < 0.25)).astype(float)

reachable_risk = churn_risk * (1 - product_health)

high_value_need = enterprise * (churn_risk > 0.45).astype(float)

propensity = sigmoid(

-0.95

+ 1.85 * churn_risk

- 1.15 * product_health

+ 0.65 * enterprise

+ 0.55 * discount_sensitivity

+ 0.42 * onboarding_gap

+ 0.20 * support_load

+ 0.22 * mrr_z

)

propensity = np.clip(propensity, 0.06, 0.94)

treatment = rng.binomial(1, propensity, n)

baseline = (

62

+ 12.0 * mrr_z

+ 19.0 * product_health

- 27.0 * churn_risk

+ 6.0 * enterprise

+ 3.0 * usage_depth

- 1.7 * support_load

- 7.0 * onboarding_gap

+ 2.3 * region_west

- 1.2 * region_emea

+ 3.5 * np.sin(usage_depth)

)

tau = (

2.5

+ 40.0 * reachable_risk

+ 8.0 * high_value_need

+ 11.0 * discount_sensitivity * churn_risk

+ 6.0 * onboarding_gap

- 16.0 * severe_risk

- 2.2 * np.maximum(support_load - 4, 0)

+ 2.0 * region_emea

)

tau = np.clip(tau, -12, 48)

outcome = baseline + treatment * tau + rng.normal(0, 8.0, n)

return pd.DataFrame(

{

"account_id": np.arange(1, n + 1),

"churn_risk": churn_risk,

"product_health": product_health,

"discount_sensitivity": discount_sensitivity,

"usage_depth": usage_depth,

"log_mrr": log_mrr,

"mrr_z": mrr_z,

"enterprise": enterprise,

"onboarding_gap": onboarding_gap,

"support_load": support_load,

"region_west": region_west,

"region_emea": region_emea,

"propensity": propensity,

"treatment": treatment,

"baseline": baseline,

"true_tau": tau,

"outcome": outcome,

}

)

df = simulate_campaign_data()

feature_cols = [

"churn_risk",

"product_health",

"discount_sensitivity",

"usage_depth",

"mrr_z",

"enterprise",

"onboarding_gap",

"support_load",

"region_west",

"region_emea",

]

df.head()| account_id | churn_risk | product_health | discount_sensitivity | usage_depth | log_mrr | mrr_z | enterprise | onboarding_gap | support_load | region_west | region_emea | propensity | treatment | baseline | true_tau | outcome | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1 | 0.627 | 0.814 | 0.620 | 0.665 | 4.654 | 0.406 | 1 | 0.729 | 3 | 1 | 0 | 0.779 | 1 | 67.679 | 23.810 | 93.935 |

| 1 | 2 | 0.474 | 0.843 | 0.694 | -0.982 | 4.528 | 0.203 | 1 | 0.673 | 2 | 0 | 1 | 0.672 | 1 | 58.488 | 23.139 | 75.721 |

| 2 | 3 | 0.661 | 0.162 | 0.223 | 1.651 | 4.724 | 0.519 | 0 | 0.364 | 3 | 0 | 0 | 0.746 | 1 | 54.240 | 28.474 | 97.196 |

| 3 | 4 | 0.158 | 0.431 | 0.792 | 0.955 | 4.986 | 0.940 | 1 | 0.388 | 0 | 0 | 0 | 0.575 | 1 | 86.212 | 9.795 | 100.562 |

| 4 | 5 | 0.710 | 0.652 | 0.352 | 1.187 | 4.755 | 0.568 | 1 | 0.689 | 2 | 0 | 0 | 0.781 | 1 | 66.608 | 27.269 | 104.903 |

summary = pd.DataFrame(

{

"quantity": [

"Accounts",

"Treatment rate",

"Average observed outcome",

"Average true CATE",

"Share with positive true effect",

"Propensity min",

"Propensity max",

],

"value": [

len(df),

df["treatment"].mean(),

df["outcome"].mean(),

df["true_tau"].mean(),

(df["true_tau"] > 0).mean(),

df["propensity"].min(),

df["propensity"].max(),

],

}

)

display(summary)| quantity | value | |

|---|---|---|

| 0 | Accounts | 11000.000 |

| 1 | Treatment rate | 0.557 |

| 2 | Average observed outcome | 68.545 |

| 3 | Average true CATE | 17.288 |

| 4 | Share with positive true effect | 1.000 |

| 5 | Propensity min | 0.121 |

| 6 | Propensity max | 0.940 |

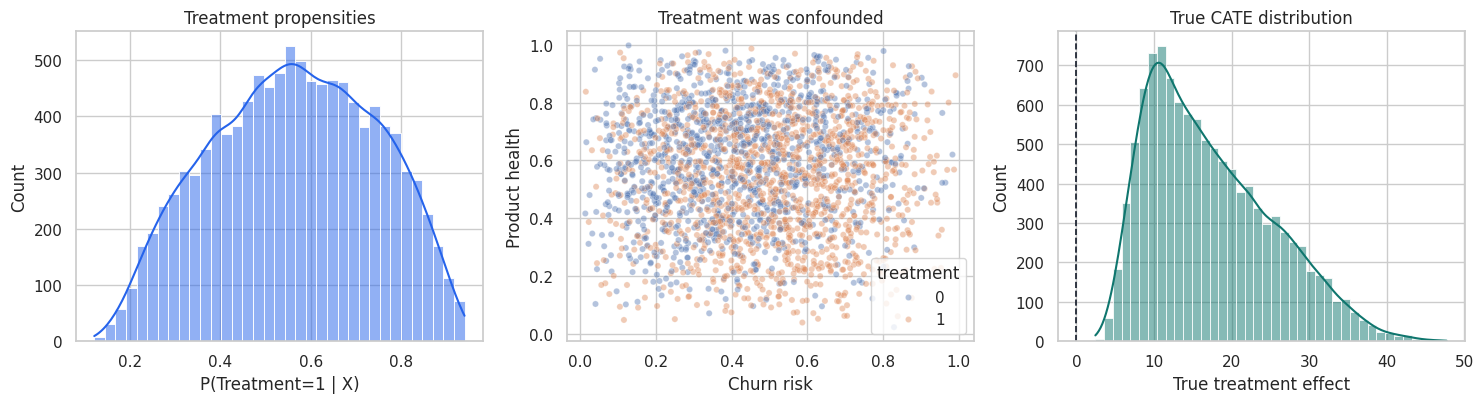

fig, axes = plt.subplots(1, 3, figsize=(15, 4.2))

sns.histplot(df["propensity"], bins=35, kde=True, color="#2563eb", ax=axes[0])

axes[0].set_title("Treatment propensities")

axes[0].set_xlabel("P(Treatment=1 | X)")

sns.scatterplot(

data=df.sample(2500, random_state=3),

x="churn_risk",

y="product_health",

hue="treatment",

alpha=0.42,

s=20,

ax=axes[1],

)

axes[1].set_title("Treatment was confounded")

axes[1].set_xlabel("Churn risk")

axes[1].set_ylabel("Product health")

sns.histplot(df["true_tau"], bins=40, kde=True, color="#0f766e", ax=axes[2])

axes[2].axvline(0, color="#111827", linestyle="--", linewidth=1.2)

axes[2].set_title("True CATE distribution")

axes[2].set_xlabel("True treatment effect")

plt.tight_layout()

plt.show()

The simulation gives us a luxury that real projects do not have: the true treatment effect for every account. We will use it as a teaching device, but the notebook will clearly mark which diagnostics are simulation-only and which are usable in real projects.

4. Train, Validation, and Honest Scoring

Validation must be honest. We will:

- Split the data into model-training and validation samples.

- Fit CATE candidate models only on the training sample.

- Fit nuisance models on the training sample and score the validation sample.

- Compare candidate CATE scores on the held-out validation sample.

This avoids judging a causal score on the same observations used to fit it.

train_idx, val_idx = train_test_split(

df.index,

test_size=0.40,

random_state=5810,

stratify=df["treatment"],

)

train = df.loc[train_idx].copy()

valid = df.loc[val_idx].copy()

len(train), len(valid), train["treatment"].mean(), valid["treatment"].mean()(6600, 4400, np.float64(0.556969696969697), np.float64(0.5568181818181818))5. Candidate CATE Models

We will compare several scores:

- ATE baseline: predicts the same effect for everyone.

- Risk-only score: ranks by churn risk, a common but noncausal business shortcut.

- S-learner: one outcome model with treatment and treatment interactions.

- T-learner: separate outcome models for treated and untreated observations.

- R-learner style score: residualizes outcome and treatment, then learns treatment-effect heterogeneity.

- Placebo shuffled-treatment score: a negative-control model trained after shuffling treatment labels.

The placebo score should not validate well. It is a useful reminder that a flexible model can create impressive-looking heterogeneity out of noise.

def add_treatment_features(frame, treatment_values):

base = frame[feature_cols].reset_index(drop=True).copy()

treatment_values = np.asarray(treatment_values)

base["treatment"] = treatment_values

for col in feature_cols:

base[f"treatment_x_{col}"] = treatment_values * base[col].to_numpy()

return base

def fit_s_learner(train_frame):

model = HistGradientBoostingRegressor(

max_iter=180,

learning_rate=0.045,

min_samples_leaf=45,

l2_regularization=0.03,

random_state=5811,

)

X = add_treatment_features(train_frame, train_frame["treatment"].to_numpy())

model.fit(X, train_frame["outcome"])

return model

def predict_s_learner(model, frame):

x1 = add_treatment_features(frame, np.ones(len(frame)))

x0 = add_treatment_features(frame, np.zeros(len(frame)))

return model.predict(x1) - model.predict(x0)

def fit_t_learner(train_frame, seed=5812):

base_model = HistGradientBoostingRegressor(

max_iter=180,

learning_rate=0.045,

min_samples_leaf=40,

l2_regularization=0.025,

random_state=seed,

)

m1 = clone(base_model)

m0 = clone(base_model)

m1.fit(train_frame.loc[train_frame["treatment"] == 1, feature_cols], train_frame.loc[train_frame["treatment"] == 1, "outcome"])

m0.fit(train_frame.loc[train_frame["treatment"] == 0, feature_cols], train_frame.loc[train_frame["treatment"] == 0, "outcome"])

return m1, m0

def predict_t_learner(models, frame):

m1, m0 = models

return m1.predict(frame[feature_cols]) - m0.predict(frame[feature_cols])

def crossfit_nuisance_for_r_learner(train_frame, n_splits=5, seed=5813):

n = len(train_frame)

m_hat = np.zeros(n)

e_hat = np.zeros(n)

fold_id = np.zeros(n, dtype=int)

outcome_model = HistGradientBoostingRegressor(

max_iter=160,

learning_rate=0.05,

min_samples_leaf=45,

l2_regularization=0.03,

random_state=seed,

)

propensity_model = HistGradientBoostingClassifier(

max_iter=160,

learning_rate=0.05,

min_samples_leaf=45,

l2_regularization=0.03,

random_state=seed + 1,

)

kfold = KFold(n_splits=n_splits, shuffle=True, random_state=seed)

for fold, (fit_idx, pred_idx) in enumerate(kfold.split(train_frame), start=1):

fit = train_frame.iloc[fit_idx]

pred = train_frame.iloc[pred_idx]

om = clone(outcome_model)

pm = clone(propensity_model)

om.fit(fit[feature_cols], fit["outcome"])

pm.fit(fit[feature_cols], fit["treatment"])

m_hat[pred_idx] = om.predict(pred[feature_cols])

e_hat[pred_idx] = np.clip(pm.predict_proba(pred[feature_cols])[:, 1], 0.04, 0.96)

fold_id[pred_idx] = fold

return m_hat, e_hat, fold_id

def fit_r_learner(train_frame):

m_hat, e_hat, _ = crossfit_nuisance_for_r_learner(train_frame)

y_res = train_frame["outcome"].to_numpy() - m_hat

w_res = train_frame["treatment"].to_numpy() - e_hat

pseudo_target = y_res / np.where(np.abs(w_res) < 0.05, np.sign(w_res) * 0.05 + (w_res == 0) * 0.05, w_res)

weights = np.clip(w_res**2, 0.0025, None)

tau_model = HistGradientBoostingRegressor(

max_iter=180,

learning_rate=0.045,

min_samples_leaf=45,

l2_regularization=0.03,

random_state=5814,

)

tau_model.fit(train_frame[feature_cols], pseudo_target, sample_weight=weights)

return tau_model

def fit_nuisance_for_validation(train_frame):

outcome_model = HistGradientBoostingRegressor(

max_iter=180,

learning_rate=0.045,

min_samples_leaf=45,

l2_regularization=0.03,

random_state=5815,

)

propensity_model = HistGradientBoostingClassifier(

max_iter=180,

learning_rate=0.045,

min_samples_leaf=45,

l2_regularization=0.03,

random_state=5816,

)

m1, m0 = fit_t_learner(train_frame, seed=5817)

m = clone(outcome_model)

e = clone(propensity_model)

m.fit(train_frame[feature_cols], train_frame["outcome"])

e.fit(train_frame[feature_cols], train_frame["treatment"])

return m, e, m1, m0s_model = fit_s_learner(train)

t_models = fit_t_learner(train)

r_model = fit_r_learner(train)

nuisance_m, nuisance_e, nuisance_m1, nuisance_m0 = fit_nuisance_for_validation(train)

rng = np.random.default_rng(5818)

placebo_train = train.copy()

placebo_train["treatment"] = rng.permutation(placebo_train["treatment"].to_numpy())

placebo_t_models = fit_t_learner(placebo_train, seed=5819)

ate_hat = (

train.loc[train["treatment"] == 1, "outcome"].mean()

- train.loc[train["treatment"] == 0, "outcome"].mean()

)

valid_scores = pd.DataFrame(index=valid.index)

valid_scores["ATE baseline"] = ate_hat

valid_scores["Risk-only score"] = 35 * (valid["churn_risk"] - valid["churn_risk"].mean())

valid_scores["S-learner"] = predict_s_learner(s_model, valid)

valid_scores["T-learner"] = predict_t_learner(t_models, valid)

valid_scores["R-learner style"] = r_model.predict(valid[feature_cols])

valid_scores["Placebo shuffled treatment"] = predict_t_learner(placebo_t_models, valid)

valid_eval = valid.join(valid_scores)

valid_eval.head()| account_id | churn_risk | product_health | discount_sensitivity | usage_depth | log_mrr | mrr_z | enterprise | onboarding_gap | support_load | ... | treatment | baseline | true_tau | outcome | ATE baseline | Risk-only score | S-learner | T-learner | R-learner style | Placebo shuffled treatment | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 3591 | 3592 | 0.284 | 0.797 | 0.133 | 1.174 | 4.073 | -0.530 | 0 | 0.183 | 0 | ... | 0 | 68.566 | 6.326 | 71.706 | 19.805 | -6.253 | 4.419 | 4.857 | 5.161 | 3.495 |

| 7686 | 7687 | 0.089 | 0.648 | 0.701 | -1.059 | 4.317 | -0.137 | 1 | 0.224 | 1 | ... | 0 | 66.772 | 5.779 | 57.065 | 19.805 | -13.097 | 3.226 | 6.323 | 9.117 | -3.517 |

| 8745 | 8746 | 0.730 | 0.537 | 0.079 | 0.243 | 3.088 | -2.115 | 0 | 0.490 | 3 | ... | 1 | 22.436 | 19.606 | 41.287 | 19.805 | 9.361 | 17.396 | 13.429 | 11.406 | -0.196 |

| 7984 | 7985 | 0.547 | 0.265 | 0.325 | -0.541 | 4.924 | 0.841 | 0 | 0.603 | 0 | ... | 1 | 53.500 | 26.164 | 90.063 | 19.805 | 2.954 | 19.980 | 26.434 | 31.962 | -0.632 |

| 9957 | 9958 | 0.308 | 0.825 | 0.584 | 0.289 | 4.695 | 0.471 | 1 | 0.311 | 0 | ... | 0 | 80.704 | 8.501 | 85.448 | 19.805 | -5.418 | 12.174 | 8.776 | 10.608 | 5.446 |

5 rows × 23 columns

6. Simulation-Only Metric: PEHE

The precision in estimating heterogeneous effects is:

\[ PEHE(\hat{\tau}) = \sqrt{\frac{1}{n}\sum_i(\hat{\tau}(X_i)-\tau(X_i))^2} \]

PEHE is excellent for simulation studies and benchmark datasets where potential outcomes are known by construction. It is not available in ordinary business data.

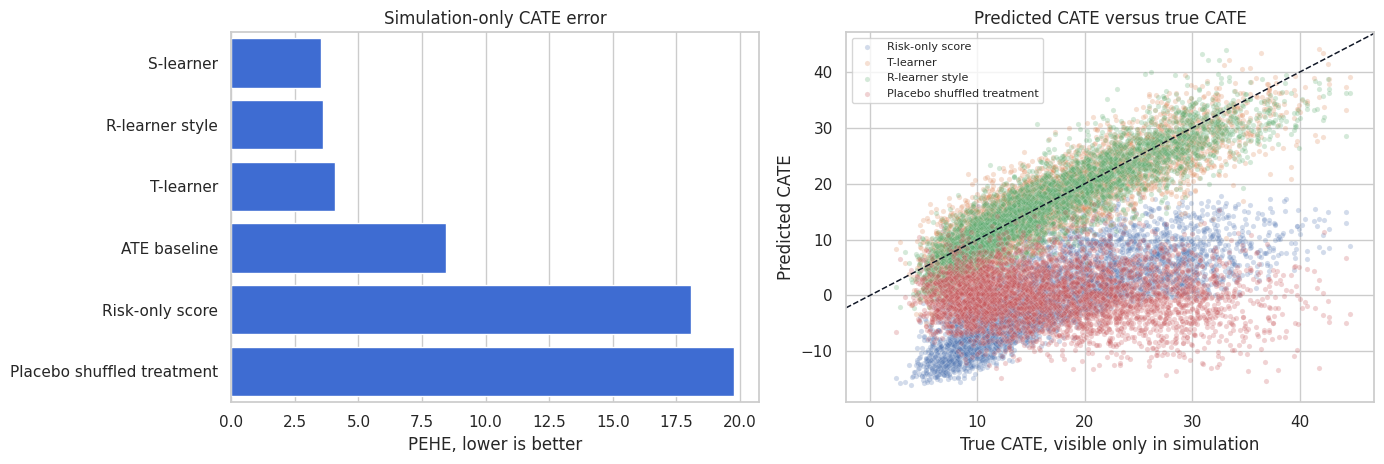

candidate_cols = list(valid_scores.columns)

pehe_rows = []

for col in candidate_cols:

error = valid_eval[col] - valid_eval["true_tau"]

pehe_rows.append(

{

"model": col,

"PEHE_simulation_only": np.sqrt(np.mean(error**2)),

"bias": np.mean(error),

"corr_with_true_tau": pd.Series(valid_eval[col]).corr(valid_eval["true_tau"], method="spearman"),

}

)

pehe_table = pd.DataFrame(pehe_rows).sort_values("PEHE_simulation_only")

display(pehe_table)| model | PEHE_simulation_only | bias | corr_with_true_tau | |

|---|---|---|---|---|

| 2 | S-learner | 3.524 | -0.644 | 0.913 |

| 4 | R-learner style | 3.586 | -0.488 | 0.912 |

| 3 | T-learner | 4.060 | -0.468 | 0.885 |

| 0 | ATE baseline | 8.438 | 2.593 | NaN |

| 1 | Risk-only score | 18.089 | -17.212 | 0.780 |

| 5 | Placebo shuffled treatment | 19.773 | -17.409 | -0.035 |

fig, axes = plt.subplots(1, 2, figsize=(14, 4.8))

sns.barplot(

data=pehe_table,

y="model",

x="PEHE_simulation_only",

color="#2563eb",

ax=axes[0],

)

axes[0].set_title("Simulation-only CATE error")

axes[0].set_xlabel("PEHE, lower is better")

axes[0].set_ylabel("")

for col in ["Risk-only score", "T-learner", "R-learner style", "Placebo shuffled treatment"]:

sns.scatterplot(

x=valid_eval["true_tau"],

y=valid_eval[col],

alpha=0.25,

s=14,

label=col,

ax=axes[1],

)

axes[1].axline((0, 0), slope=1, color="#111827", linestyle="--", linewidth=1.1)

axes[1].set_title("Predicted CATE versus true CATE")

axes[1].set_xlabel("True CATE, visible only in simulation")

axes[1].set_ylabel("Predicted CATE")

axes[1].legend(loc="best", fontsize=8)

plt.tight_layout()

plt.show()

PEHE teaches an important lesson: models that look plausible can still miss the treatment-effect function. The risk-only score may be useful for prioritizing churn prevention, but it is not necessarily a causal effect score. The placebo model should fail here; if it does not, the validation design is too weak.

7. Outcome Prediction Is Not Enough

Outcome prediction can be excellent even when CATE ranking is weak. A model can learn that high-value, healthy accounts have better outcomes while learning little about who is persuadable.

Here we compare:

- Outcome prediction quality.

- Treatment-effect ranking quality.

They are not the same metric.

observed_features_train = train[feature_cols + ["treatment"]].copy()

observed_features_valid = valid[feature_cols + ["treatment"]].copy()

outcome_predictor = HistGradientBoostingRegressor(

max_iter=180,

learning_rate=0.045,

min_samples_leaf=45,

l2_regularization=0.03,

random_state=5820,

)

outcome_predictor.fit(observed_features_train, train["outcome"])

outcome_pred = outcome_predictor.predict(observed_features_valid)

outcome_vs_causal = pd.DataFrame(

{

"metric": [

"Outcome RMSE",

"Outcome R2",

"Spearman correlation: outcome prediction vs true CATE",

"Spearman correlation: R-learner score vs true CATE",

],

"value": [

np.sqrt(mean_squared_error(valid["outcome"], outcome_pred)),

r2_score(valid["outcome"], outcome_pred),

pd.Series(outcome_pred).corr(valid["true_tau"], method="spearman"),

valid_eval["R-learner style"].corr(valid_eval["true_tau"], method="spearman"),

],

}

)

display(outcome_vs_causal)| metric | value | |

|---|---|---|

| 0 | Outcome RMSE | 8.361 |

| 1 | Outcome R2 | 0.834 |

| 2 | Spearman correlation: outcome prediction vs tr... | 0.027 |

| 3 | Spearman correlation: R-learner score vs true ... | 0.912 |

Good outcome prediction is useful for nuisance modeling, but it is not a sufficient validation of a treatment-effect model. A causal ML readout should not lead with ordinary RMSE or AUC unless the target is actually outcome prediction.

8. Held-Out R-Loss

The R-learner motivates a validation loss for treatment effects. Estimate nuisance functions:

\[ m(x) = E[Y\mid X=x] \]

\[ e(x) = P(W=1\mid X=x) \]

Then evaluate CATE scores with:

\[ L_R(\hat{\tau}) = \frac{1}{n}\sum_i \left[ \{Y_i-\hat{m}(X_i)\} - \hat{\tau}(X_i)\{W_i-\hat{e}(X_i)\} \right]^2 \]

Nie and Wager (2020) show how residualized losses can be used for heterogeneous treatment-effect estimation. In validation, R-loss is attractive because it is computable without knowing the true CATE.

valid_m_hat = nuisance_m.predict(valid[feature_cols])

valid_e_hat = np.clip(nuisance_e.predict_proba(valid[feature_cols])[:, 1], 0.04, 0.96)

valid_mu1_hat = nuisance_m1.predict(valid[feature_cols])

valid_mu0_hat = nuisance_m0.predict(valid[feature_cols])

valid_eval["m_hat"] = valid_m_hat

valid_eval["e_hat"] = valid_e_hat

valid_eval["mu1_hat"] = valid_mu1_hat

valid_eval["mu0_hat"] = valid_mu0_hat

def r_loss(frame, score_col):

y_res = frame["outcome"].to_numpy() - frame["m_hat"].to_numpy()

w_res = frame["treatment"].to_numpy() - frame["e_hat"].to_numpy()

tau_hat = frame[score_col].to_numpy()

return np.mean((y_res - tau_hat * w_res) ** 2)

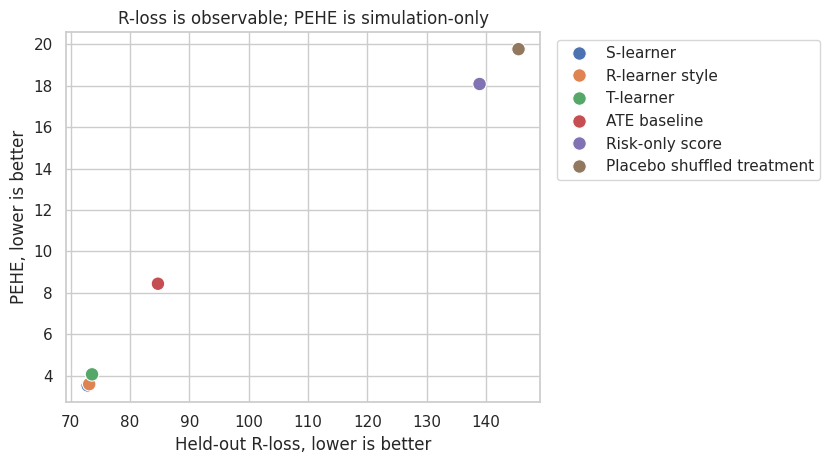

r_loss_table = pd.DataFrame(

[

{

"model": col,

"heldout_r_loss": r_loss(valid_eval, col),

"PEHE_simulation_only": np.sqrt(np.mean((valid_eval[col] - valid_eval["true_tau"]) ** 2)),

}

for col in candidate_cols

]

).sort_values("heldout_r_loss")

display(r_loss_table)| model | heldout_r_loss | PEHE_simulation_only | |

|---|---|---|---|

| 2 | S-learner | 72.845 | 3.524 |

| 4 | R-learner style | 73.101 | 3.586 |

| 3 | T-learner | 73.578 | 4.060 |

| 0 | ATE baseline | 84.690 | 8.438 |

| 1 | Risk-only score | 138.903 | 18.089 |

| 5 | Placebo shuffled treatment | 145.470 | 19.773 |

fig, ax = plt.subplots(figsize=(8.5, 4.8))

sns.scatterplot(

data=r_loss_table,

x="heldout_r_loss",

y="PEHE_simulation_only",

hue="model",

s=95,

ax=ax,

)

ax.set_title("R-loss is observable; PEHE is simulation-only")

ax.set_xlabel("Held-out R-loss, lower is better")

ax.set_ylabel("PEHE, lower is better")

ax.legend(bbox_to_anchor=(1.02, 1), loc="upper left")

plt.tight_layout()

plt.show()

R-loss is not perfect. It depends on nuisance quality, and it is not a business-value metric. But it is often a better model-selection signal than ordinary outcome prediction error because it directly evaluates the residualized treatment-effect moment.

9. Doubly Robust Pseudo-Outcomes for Calibration

A doubly robust pseudo-outcome for the CATE is:

\[ \Gamma_i = \hat{\mu}_1(X_i) + \frac{W_i}{\hat{e}(X_i)}\{Y_i-\hat{\mu}_1(X_i)\} - \hat{\mu}_0(X_i) - \frac{1-W_i}{1-\hat{e}(X_i)}\{Y_i-\hat{\mu}_0(X_i)\} \]

This pseudo-outcome is noisy at the individual level, but it is useful after grouping. If a model says a decile has average treatment effect 20, the doubly robust estimate for that decile should be near 20.

Xu and Yadlowsky (2022) study calibration error for heterogeneous treatment effects and connect treatment-effect validation to calibration ideas from predictive modeling.

def dr_cate_pseudo_outcome(frame):

w = frame["treatment"].to_numpy()

y = frame["outcome"].to_numpy()

e = frame["e_hat"].to_numpy()

mu1 = frame["mu1_hat"].to_numpy()

mu0 = frame["mu0_hat"].to_numpy()

gamma1 = mu1 + (w / e) * (y - mu1)

gamma0 = mu0 + ((1 - w) / (1 - e)) * (y - mu0)

return gamma1 - gamma0

valid_eval["dr_pseudo_tau"] = dr_cate_pseudo_outcome(valid_eval)

calibration_rows = []

for col in candidate_cols:

temp = valid_eval[[col, "dr_pseudo_tau", "true_tau"]].copy()

temp["score_bin"] = pd.qcut(temp[col].rank(method="first"), 10, labels=False)

grouped = (

temp.groupby("score_bin", as_index=False)

.agg(

avg_pred=(col, "mean"),

avg_dr=("dr_pseudo_tau", "mean"),

avg_true=("true_tau", "mean"),

n=(col, "size"),

)

)

grouped["model"] = col

calibration_rows.append(grouped)

calibration_df = pd.concat(calibration_rows, ignore_index=True)

calibration_summary = []

for col in candidate_cols:

g = calibration_df[calibration_df["model"] == col]

slope, intercept = np.polyfit(g["avg_pred"], g["avg_dr"], 1)

calibration_summary.append(

{

"model": col,

"dr_calibration_slope": slope,

"dr_calibration_intercept": intercept,

"decile_dr_true_corr": g["avg_dr"].corr(g["avg_true"]),

}

)

display(pd.DataFrame(calibration_summary).sort_values("decile_dr_true_corr", ascending=False))| model | dr_calibration_slope | dr_calibration_intercept | decile_dr_true_corr | |

|---|---|---|---|---|

| 4 | R-learner style | 0.858 | 2.614 | 0.993 |

| 2 | S-learner | 0.939 | 1.403 | 0.989 |

| 1 | Risk-only score | 0.803 | 16.968 | 0.980 |

| 3 | T-learner | 0.819 | 3.251 | 0.980 |

| 5 | Placebo shuffled treatment | -0.067 | 16.955 | 0.689 |

| 0 | ATE baseline | 0.428 | 8.484 | -0.268 |

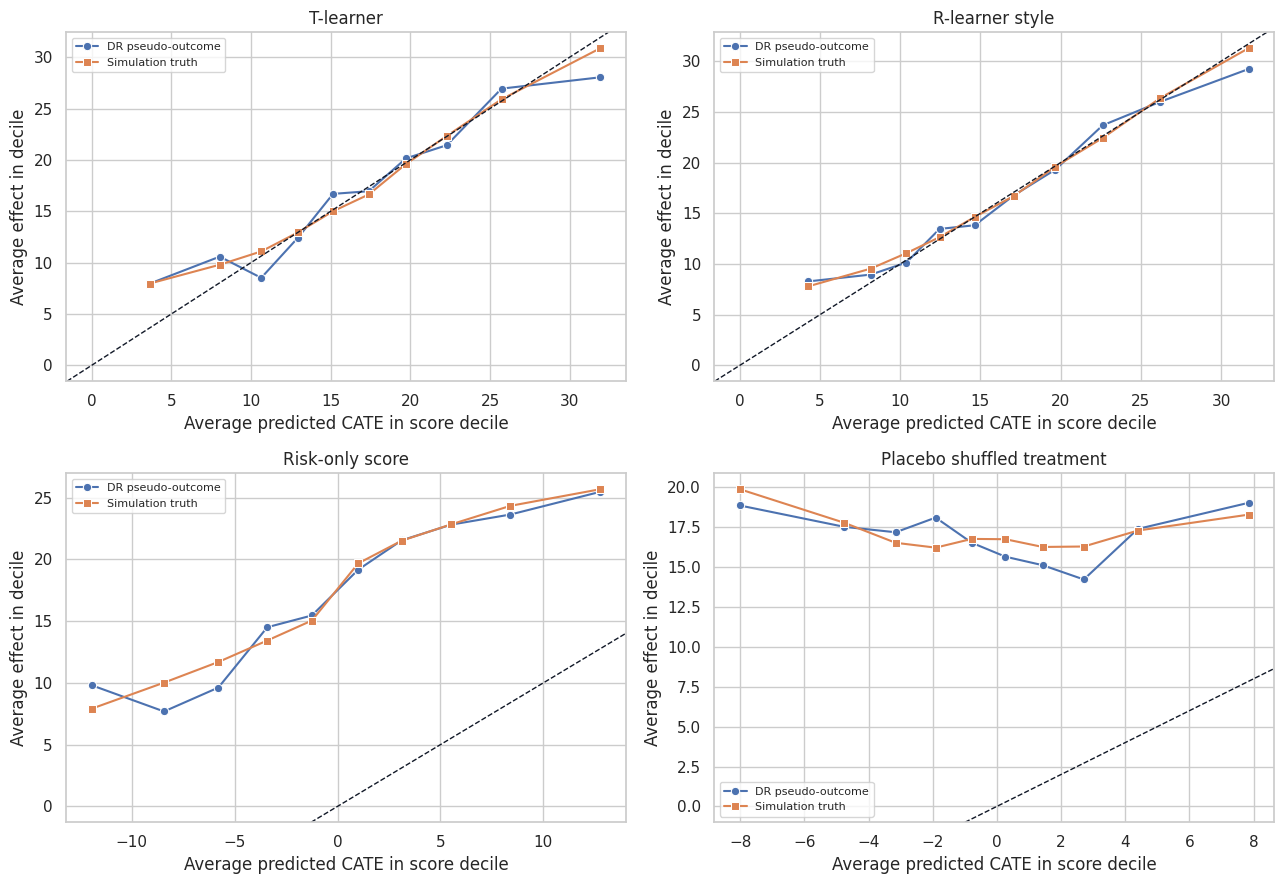

plot_models = ["T-learner", "R-learner style", "Risk-only score", "Placebo shuffled treatment"]

fig, axes = plt.subplots(2, 2, figsize=(13, 9), sharex=False, sharey=False)

for ax, model in zip(axes.ravel(), plot_models):

g = calibration_df[calibration_df["model"] == model]

sns.lineplot(data=g, x="avg_pred", y="avg_dr", marker="o", label="DR pseudo-outcome", ax=ax)

sns.lineplot(data=g, x="avg_pred", y="avg_true", marker="s", label="Simulation truth", ax=ax)

ax.axline((0, 0), slope=1, color="#111827", linestyle="--", linewidth=1.0)

ax.set_title(model)

ax.set_xlabel("Average predicted CATE in score decile")

ax.set_ylabel("Average effect in decile")

ax.legend(fontsize=8)

plt.tight_layout()

plt.show()

Calibration should be judged in groups, not one account at a time. Individual pseudo-outcomes are too noisy. Grouped calibration answers the more operational question: when the model says a segment is high effect, does that segment actually show high estimated lift?

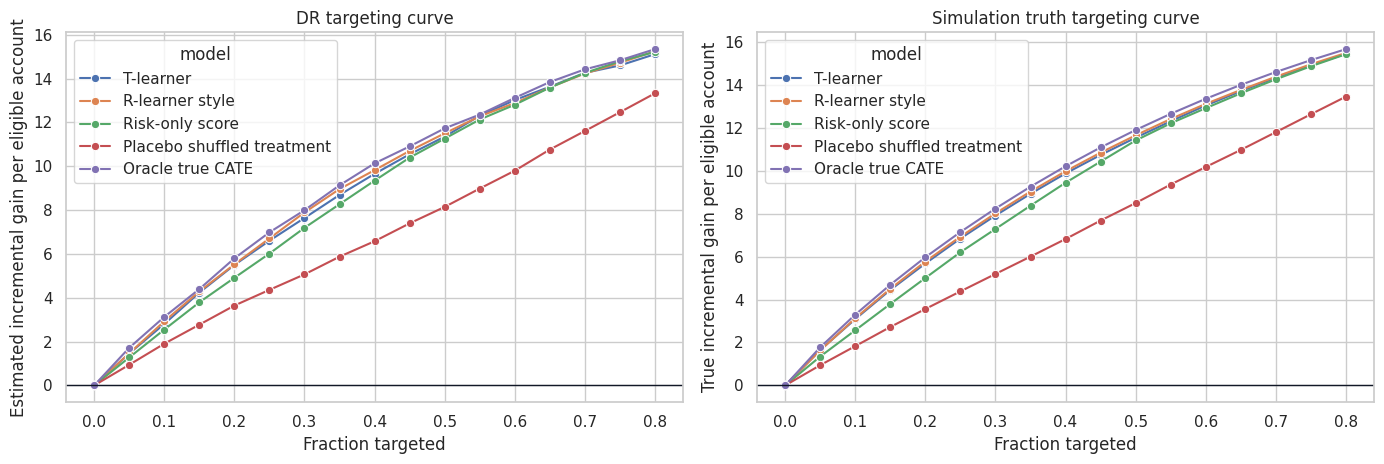

10. Uplift and Targeting Curves

Many causal ML applications are ranking problems. We may not need perfect CATE magnitudes if the business only has capacity to treat the top 20% or top 30%.

A targeting curve sorts units by score and estimates cumulative gain:

\[ G(q) = \frac{1}{n} \sum_i 1\{\hat{\tau}(X_i)\text{ is in top }q\}\tau(X_i) \]

In real data, replace \(\tau(X_i)\) with a doubly robust score. Devriendt et al. (2022) discuss uplift modeling as a ranking problem, and uplift/Qini/AUUC-style metrics are widely used for this kind of validation.

def targeting_curve(frame, score_col, fractions):

rows = []

score = frame[score_col].to_numpy()

for frac in fractions:

mask = top_fraction_mask(score, frac, require_positive=False)

rows.append(

{

"model": score_col,

"fraction": frac,

"treated_share": mask.mean(),

"dr_gain": np.mean(mask * frame["dr_pseudo_tau"].to_numpy()),

"true_gain": np.mean(mask * frame["true_tau"].to_numpy()),

}

)

return pd.DataFrame(rows)

fractions = np.linspace(0, 0.80, 17)

curve_models = ["T-learner", "R-learner style", "Risk-only score", "Placebo shuffled treatment"]

curve_df = pd.concat([targeting_curve(valid_eval, col, fractions) for col in curve_models], ignore_index=True)

valid_eval["oracle_score"] = valid_eval["true_tau"]

oracle_df = targeting_curve(valid_eval, "oracle_score", fractions)

oracle_df["model"] = "Oracle true CATE"

oracle_df["true_gain"] = [

np.mean(top_fraction_mask(valid_eval["true_tau"], frac) * valid_eval["true_tau"].to_numpy())

for frac in fractions

]

oracle_df["dr_gain"] = [

np.mean(top_fraction_mask(valid_eval["true_tau"], frac) * valid_eval["dr_pseudo_tau"].to_numpy())

for frac in fractions

]

curve_df = pd.concat([curve_df, oracle_df], ignore_index=True)

fig, axes = plt.subplots(1, 2, figsize=(14, 4.8))

sns.lineplot(data=curve_df, x="fraction", y="dr_gain", hue="model", marker="o", ax=axes[0])

axes[0].axhline(0, color="#111827", linewidth=1.0)

axes[0].set_title("DR targeting curve")

axes[0].set_xlabel("Fraction targeted")

axes[0].set_ylabel("Estimated incremental gain per eligible account")

sns.lineplot(data=curve_df, x="fraction", y="true_gain", hue="model", marker="o", ax=axes[1])

axes[1].axhline(0, color="#111827", linewidth=1.0)

axes[1].set_title("Simulation truth targeting curve")

axes[1].set_xlabel("Fraction targeted")

axes[1].set_ylabel("True incremental gain per eligible account")

plt.tight_layout()

plt.show()

def area_under_curve(curve, value_col):

ordered = curve.sort_values("fraction")

return np.trapezoid(ordered[value_col], ordered["fraction"])

auuc_rows = []

for model, group in curve_df.groupby("model"):

auuc_rows.append(

{

"model": model,

"DR_AUUC_like": area_under_curve(group, "dr_gain"),

"true_AUUC_like_simulation_only": area_under_curve(group, "true_gain"),

}

)

display(pd.DataFrame(auuc_rows).sort_values("DR_AUUC_like", ascending=False))| model | DR_AUUC_like | true_AUUC_like_simulation_only | |

|---|---|---|---|

| 0 | Oracle true CATE | 7.408 | 7.553 |

| 2 | R-learner style | 7.256 | 7.388 |

| 4 | T-learner | 7.193 | 7.331 |

| 3 | Risk-only score | 7.009 | 7.067 |

| 1 | Placebo shuffled treatment | 5.348 | 5.461 |

Targeting curves are often the most intuitive validation tool for stakeholders. They answer: if we treat the top \(q\) percent according to the model, how much incremental value should we expect?

For observational data, use doubly robust or policy-value estimates. For randomized experiments with equal treatment probability, simpler uplift curves are also common.

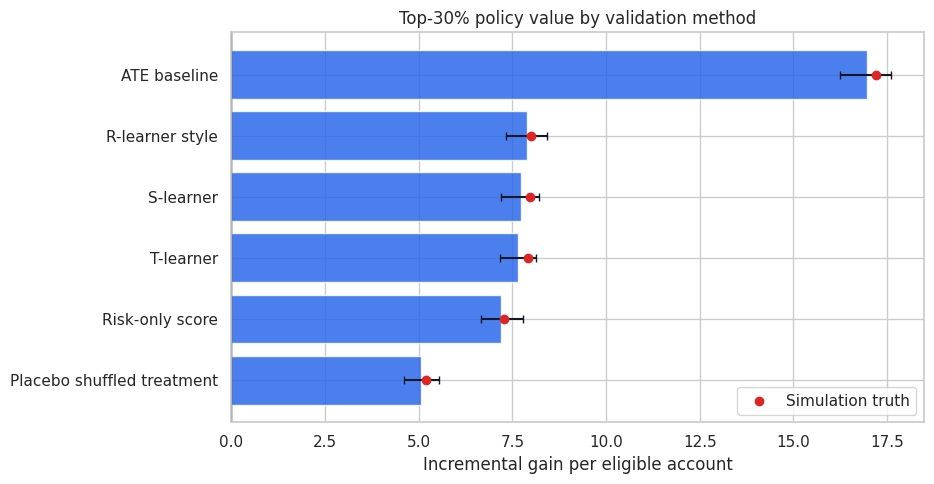

11. Top-k Policy Value

Now evaluate a concrete capacity rule: treat the top 30% of accounts according to each score.

This is closer to how a model will actually be used. A CATE model with moderate PEHE can still be valuable if it ranks the top of the queue well.

capacity = 0.30

policy_rows = []

for col in candidate_cols:

mask = top_fraction_mask(valid_eval[col], capacity, require_positive=False)

dr_contrib = mask * valid_eval["dr_pseudo_tau"].to_numpy()

true_contrib = mask * valid_eval["true_tau"].to_numpy()

ci_low, ci_high = bootstrap_ci(dr_contrib, seed=5821, n_boot=400)

policy_rows.append(

{

"model": col,

"target_rate": mask.mean(),

"DR_policy_gain": dr_contrib.mean(),

"DR_ci_low": ci_low,

"DR_ci_high": ci_high,

"true_policy_gain_simulation_only": true_contrib.mean(),

"avg_true_tau_selected": valid_eval.loc[mask == 1, "true_tau"].mean(),

}

)

policy_value_table = pd.DataFrame(policy_rows).sort_values("DR_policy_gain", ascending=False)

display(policy_value_table)| model | target_rate | DR_policy_gain | DR_ci_low | DR_ci_high | true_policy_gain_simulation_only | avg_true_tau_selected | |

|---|---|---|---|---|---|---|---|

| 0 | ATE baseline | 1.000 | 16.968 | 16.244 | 17.603 | 17.212 | 17.212 |

| 4 | R-learner style | 0.300 | 7.892 | 7.321 | 8.418 | 8.010 | 26.699 |

| 2 | S-learner | 0.300 | 7.719 | 7.202 | 8.217 | 7.965 | 26.549 |

| 3 | T-learner | 0.300 | 7.640 | 7.170 | 8.128 | 7.909 | 26.363 |

| 1 | Risk-only score | 0.300 | 7.191 | 6.665 | 7.771 | 7.284 | 24.281 |

| 5 | Placebo shuffled treatment | 0.300 | 5.067 | 4.607 | 5.537 | 5.189 | 17.297 |

fig, ax = plt.subplots(figsize=(9.5, 5.0))

plot_data = policy_value_table.sort_values("DR_policy_gain")

ax.barh(plot_data["model"], plot_data["DR_policy_gain"], color="#2563eb", alpha=0.82)

ax.errorbar(

x=plot_data["DR_policy_gain"],

y=np.arange(len(plot_data)),

xerr=[

plot_data["DR_policy_gain"] - plot_data["DR_ci_low"],

plot_data["DR_ci_high"] - plot_data["DR_policy_gain"],

],

fmt="none",

ecolor="#111827",

capsize=3,

)

ax.scatter(plot_data["true_policy_gain_simulation_only"], np.arange(len(plot_data)), color="#dc2626", zorder=5, label="Simulation truth")

ax.axvline(0, color="#111827", linewidth=1.0)

ax.set_title("Top-30% policy value by validation method")

ax.set_xlabel("Incremental gain per eligible account")

ax.legend()

plt.tight_layout()

plt.show()

This table turns validation into a decision: which score would we actually use under a 30% capacity constraint? It also shows uncertainty, which is crucial when two models are close.

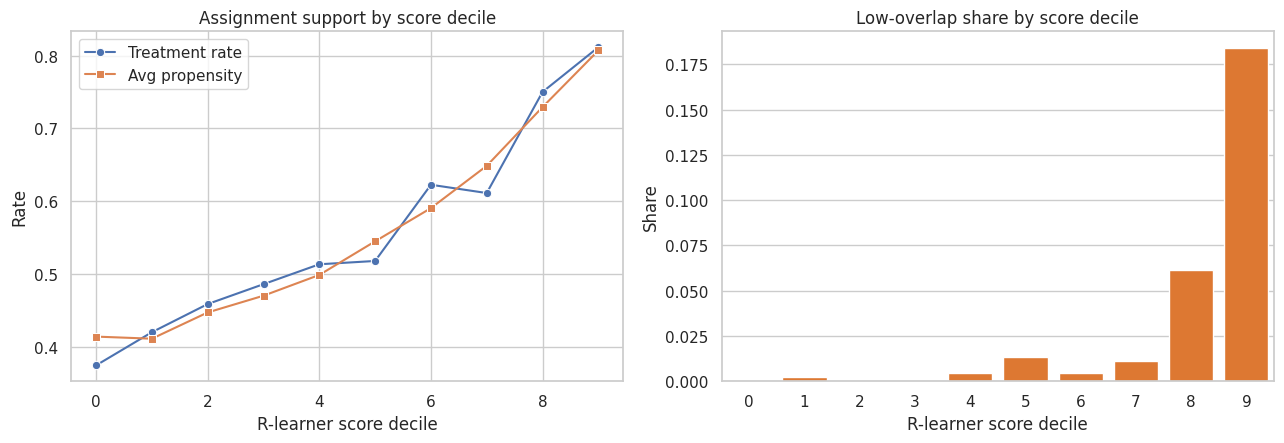

12. Overlap and Positivity by Score Band

Even a strong CATE score is risky if high-scored units live in regions with weak overlap. We need enough treated and untreated observations in the validation data to support the estimated contrast.

For each score decile, inspect:

- Average propensity.

- Treatment rate.

- Share with propensities near 0 or 1.

- Residual treatment variation.

score_for_overlap = "R-learner style"

overlap = valid_eval.copy()

overlap["score_decile"] = pd.qcut(overlap[score_for_overlap].rank(method="first"), 10, labels=False)

overlap_table = (

overlap.groupby("score_decile", as_index=False)

.agg(

n=("account_id", "size"),

avg_score=(score_for_overlap, "mean"),

avg_e_hat=("e_hat", "mean"),

treatment_rate=("treatment", "mean"),

low_overlap_share=("e_hat", lambda s: np.mean((s < 0.10) | (s > 0.90))),

residual_treatment_sd=("treatment", lambda s: np.std(s)),

avg_dr_pseudo=("dr_pseudo_tau", "mean"),

avg_true_tau=("true_tau", "mean"),

)

)

display(overlap_table)| score_decile | n | avg_score | avg_e_hat | treatment_rate | low_overlap_share | residual_treatment_sd | avg_dr_pseudo | avg_true_tau | |

|---|---|---|---|---|---|---|---|---|---|

| 0 | 0 | 440 | 4.261 | 0.414 | 0.375 | 0.000 | 0.484 | 8.283 | 7.792 |

| 1 | 1 | 440 | 8.170 | 0.412 | 0.420 | 0.002 | 0.494 | 8.956 | 9.548 |

| 2 | 2 | 440 | 10.386 | 0.448 | 0.459 | 0.000 | 0.498 | 10.145 | 11.068 |

| 3 | 3 | 440 | 12.453 | 0.471 | 0.486 | 0.000 | 0.500 | 13.461 | 12.647 |

| 4 | 4 | 440 | 14.644 | 0.499 | 0.514 | 0.005 | 0.500 | 13.822 | 14.638 |

| 5 | 5 | 440 | 17.095 | 0.545 | 0.518 | 0.014 | 0.500 | 16.782 | 16.720 |

| 6 | 6 | 440 | 19.673 | 0.591 | 0.623 | 0.005 | 0.485 | 19.311 | 19.610 |

| 7 | 7 | 440 | 22.621 | 0.649 | 0.611 | 0.011 | 0.487 | 23.678 | 22.431 |

| 8 | 8 | 440 | 26.223 | 0.729 | 0.750 | 0.061 | 0.433 | 26.011 | 26.379 |

| 9 | 9 | 440 | 31.715 | 0.807 | 0.811 | 0.184 | 0.391 | 29.232 | 31.287 |

fig, axes = plt.subplots(1, 2, figsize=(13, 4.6))

sns.lineplot(data=overlap_table, x="score_decile", y="treatment_rate", marker="o", label="Treatment rate", ax=axes[0])

sns.lineplot(data=overlap_table, x="score_decile", y="avg_e_hat", marker="s", label="Avg propensity", ax=axes[0])

axes[0].set_title("Assignment support by score decile")

axes[0].set_xlabel("R-learner score decile")

axes[0].set_ylabel("Rate")

axes[0].legend()

sns.barplot(data=overlap_table, x="score_decile", y="low_overlap_share", color="#f97316", ax=axes[1])

axes[1].set_title("Low-overlap share by score decile")

axes[1].set_xlabel("R-learner score decile")

axes[1].set_ylabel("Share")

plt.tight_layout()

plt.show()

If the best-looking score sends decisions into low-overlap regions, the next step should be exploration or a randomized pilot, not blind deployment.

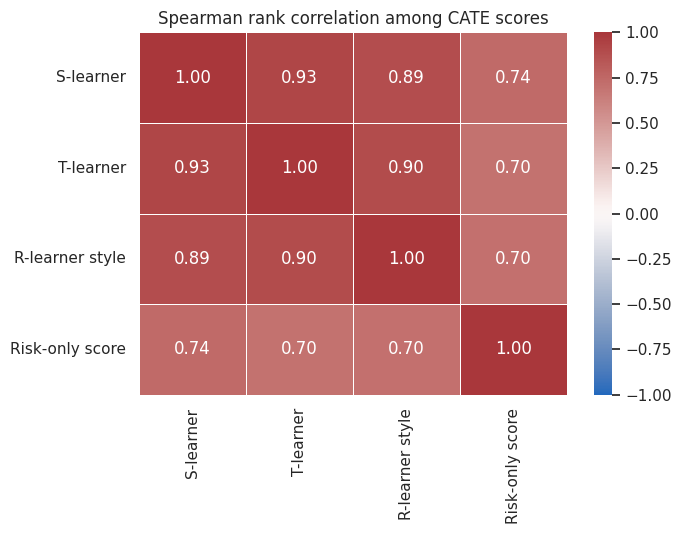

13. Stability Across Models

Good causal ML validation asks whether the recommendation depends on one fragile modeling choice.

We compare:

- Rank correlation across scores.

- Top-30% overlap across scores.

- Agreement between flexible and interpretable approaches.

Stability does not prove correctness, but instability is a risk signal.

stability_models = ["S-learner", "T-learner", "R-learner style", "Risk-only score"]

rank_corr = valid_eval[stability_models].corr(method="spearman")

display(rank_corr)

top_masks = {m: top_fraction_mask(valid_eval[m], 0.30) for m in stability_models}

overlap_rows = []

for i, m1 in enumerate(stability_models):

for m2 in stability_models[i + 1 :]:

a = top_masks[m1].astype(bool)

b = top_masks[m2].astype(bool)

overlap_rows.append(

{

"model_a": m1,

"model_b": m2,

"top_30_jaccard": np.sum(a & b) / np.sum(a | b),

"top_30_overlap_given_a": np.sum(a & b) / np.sum(a),

}

)

display(pd.DataFrame(overlap_rows).sort_values("top_30_jaccard", ascending=False))| S-learner | T-learner | R-learner style | Risk-only score | |

|---|---|---|---|---|

| S-learner | 1.000 | 0.926 | 0.886 | 0.742 |

| T-learner | 0.926 | 1.000 | 0.896 | 0.700 |

| R-learner style | 0.886 | 0.896 | 1.000 | 0.705 |

| Risk-only score | 0.742 | 0.700 | 0.705 | 1.000 |

| model_a | model_b | top_30_jaccard | top_30_overlap_given_a | |

|---|---|---|---|---|

| 0 | S-learner | T-learner | 0.731 | 0.845 |

| 3 | T-learner | R-learner style | 0.690 | 0.817 |

| 1 | S-learner | R-learner style | 0.676 | 0.807 |

| 5 | R-learner style | Risk-only score | 0.451 | 0.622 |

| 2 | S-learner | Risk-only score | 0.443 | 0.614 |

| 4 | T-learner | Risk-only score | 0.439 | 0.611 |

fig, ax = plt.subplots(figsize=(7, 5.5))

sns.heatmap(rank_corr, annot=True, fmt=".2f", cmap="vlag", vmin=-1, vmax=1, linewidths=0.5, ax=ax)

ax.set_title("Spearman rank correlation among CATE scores")

plt.tight_layout()

plt.show()

The goal is not to force all models to agree. Different learners can capture different signals. But if the selected policy changes completely when the modeling recipe changes, that should be visible in the readout.

14. Placebo and Negative-Control Checks

A placebo check asks whether the pipeline finds treatment effects when it should not.

Here the placebo model was trained after shuffling treatment labels. It should perform poorly on PEHE, R-loss, calibration, and policy value. In real projects, related checks include:

- Placebo outcomes that should not respond to treatment.

- Pre-treatment outcomes.

- Randomized treatment labels.

- Future outcomes outside the plausible effect window.

- Segments where domain experts expect no effect.

These checks do not prove validity, but they catch overly eager pipelines.

placebo_summary = pd.DataFrame(

{

"metric": [

"Placebo PEHE, simulation only",

"Placebo held-out R-loss",

"Placebo top-30 DR policy gain",

"Placebo top-30 true policy gain, simulation only",

"R-learner top-30 DR policy gain",

"R-learner top-30 true policy gain, simulation only",

],

"value": [

pehe_table.loc[pehe_table["model"] == "Placebo shuffled treatment", "PEHE_simulation_only"].iloc[0],

r_loss_table.loc[r_loss_table["model"] == "Placebo shuffled treatment", "heldout_r_loss"].iloc[0],

policy_value_table.loc[policy_value_table["model"] == "Placebo shuffled treatment", "DR_policy_gain"].iloc[0],

policy_value_table.loc[

policy_value_table["model"] == "Placebo shuffled treatment",

"true_policy_gain_simulation_only",

].iloc[0],

policy_value_table.loc[policy_value_table["model"] == "R-learner style", "DR_policy_gain"].iloc[0],

policy_value_table.loc[

policy_value_table["model"] == "R-learner style",

"true_policy_gain_simulation_only",

].iloc[0],

],

}

)

display(placebo_summary)| metric | value | |

|---|---|---|

| 0 | Placebo PEHE, simulation only | 19.773 |

| 1 | Placebo held-out R-loss | 145.470 |

| 2 | Placebo top-30 DR policy gain | 5.067 |

| 3 | Placebo top-30 true policy gain, simulation only | 5.189 |

| 4 | R-learner top-30 DR policy gain | 7.892 |

| 5 | R-learner top-30 true policy gain, simulation ... | 8.010 |

The placebo score should not pass. If it does, the validation metric may be rewarding baseline-risk sorting, leakage, or chance imbalances rather than causal lift.

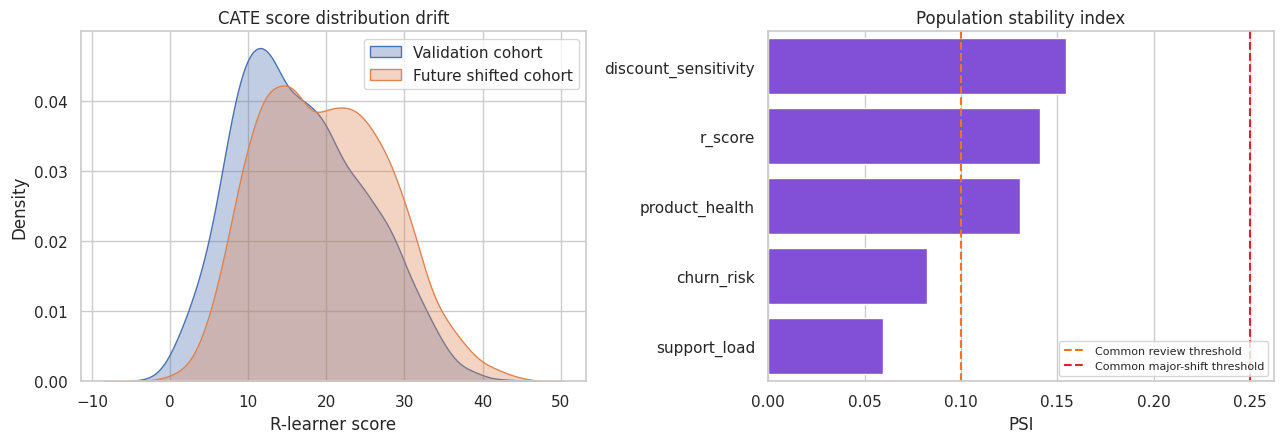

15. Deployment Drift

Validation is not over when the notebook passes. A deployed targeting model faces future cohorts that may differ from the validation cohort.

We simulate a shifted future cohort with higher churn risk, lower product health, and more discount sensitivity. Then we compare feature and score distributions.

future = simulate_campaign_data(n=5000, seed=5822, shifted=True)

future["r_score"] = r_model.predict(future[feature_cols])

valid_eval["r_score"] = valid_eval["R-learner style"]

def psi(expected, actual, bins=10):

quantiles = np.quantile(expected, np.linspace(0, 1, bins + 1))

quantiles = np.unique(quantiles)

expected_counts, _ = np.histogram(expected, bins=quantiles)

actual_counts, _ = np.histogram(actual, bins=quantiles)

expected_pct = np.clip(expected_counts / expected_counts.sum(), 1e-4, None)

actual_pct = np.clip(actual_counts / actual_counts.sum(), 1e-4, None)

return np.sum((actual_pct - expected_pct) * np.log(actual_pct / expected_pct))

drift_rows = []

for col in ["churn_risk", "product_health", "discount_sensitivity", "support_load", "r_score"]:

drift_rows.append(

{

"variable": col,

"validation_mean": valid_eval[col].mean() if col in valid_eval else valid_eval["r_score"].mean(),

"future_mean": future[col].mean(),

"mean_shift": future[col].mean() - (valid_eval[col].mean() if col in valid_eval else valid_eval["r_score"].mean()),

"PSI": psi(valid_eval[col].to_numpy() if col in valid_eval else valid_eval["r_score"].to_numpy(), future[col].to_numpy()),

}

)

drift_table = pd.DataFrame(drift_rows).sort_values("PSI", ascending=False)

display(drift_table)| variable | validation_mean | future_mean | mean_shift | PSI | |

|---|---|---|---|---|---|

| 2 | discount_sensitivity | 0.431 | 0.511 | 0.079 | 0.155 |

| 4 | r_score | 16.724 | 19.767 | 3.043 | 0.141 |

| 1 | product_health | 0.551 | 0.471 | -0.079 | 0.131 |

| 0 | churn_risk | 0.463 | 0.508 | 0.045 | 0.083 |

| 3 | support_load | 1.632 | 1.992 | 0.360 | 0.060 |

fig, axes = plt.subplots(1, 2, figsize=(13, 4.6))

sns.kdeplot(valid_eval["r_score"], label="Validation cohort", fill=True, alpha=0.35, ax=axes[0])

sns.kdeplot(future["r_score"], label="Future shifted cohort", fill=True, alpha=0.35, ax=axes[0])

axes[0].set_title("CATE score distribution drift")

axes[0].set_xlabel("R-learner score")

axes[0].legend()

sns.barplot(data=drift_table, y="variable", x="PSI", color="#7c3aed", ax=axes[1])

axes[1].axvline(0.10, color="#f97316", linestyle="--", label="Common review threshold")

axes[1].axvline(0.25, color="#dc2626", linestyle="--", label="Common major-shift threshold")

axes[1].set_title("Population stability index")

axes[1].set_xlabel("PSI")

axes[1].set_ylabel("")

axes[1].legend(fontsize=8)

plt.tight_layout()

plt.show()

Drift diagnostics do not estimate causal validity by themselves. They tell us whether the deployment population still looks like the population where the model was validated. Major drift should trigger recalibration, revalidation, or a new experiment.

16. A Practical Validation Checklist

For an industry causal ML system, validation should include:

- Identification review: treatment timing, confounders, leakage, positivity, and estimand.

- Data split discipline: train, validation, and final test or prospective pilot.

- Nuisance diagnostics: outcome model, propensity model, residual treatment variation.

- CATE diagnostics: R-loss, calibration, ranking curves, policy value.

- Robustness: alternative learners, hyperparameters, subgroup stability, and placebo checks.

- Decision diagnostics: top-k value, cost-adjusted value, capacity, fairness, and operational constraints.

- Monitoring: feature drift, score drift, action-rate drift, realized outcomes, and experimental holdouts.

- Human review: interpretability, domain plausibility, and escalation paths.

Causal ML validation is not one number. It is a chain of evidence.

best_model = policy_value_table.iloc[0]["model"]

best_policy = policy_value_table.iloc[0]

best_r_loss = r_loss_table.loc[r_loss_table["model"] == best_model, "heldout_r_loss"].iloc[0]

best_pehe = pehe_table.loc[pehe_table["model"] == best_model, "PEHE_simulation_only"].iloc[0]

readout = pd.DataFrame(

{

"item": [

"Recommended score by held-out top-30 DR value",

"Held-out R-loss",

"Top-30 DR policy gain",

"Approximate 95% CI for top-30 gain",

"Simulation-only PEHE",

"Simulation-only true top-30 gain",

"Main validation caveat",

"Recommended next step",

],

"value": [

best_model,

f"{best_r_loss:.2f}",

f"{best_policy['DR_policy_gain']:.2f}",

f"[{best_policy['DR_ci_low']:.2f}, {best_policy['DR_ci_high']:.2f}]",

f"{best_pehe:.2f}",

f"{best_policy['true_policy_gain_simulation_only']:.2f}",

"DR validation depends on nuisance quality and overlap.",

"Run a randomized pilot or maintain an exploration holdout before full automation.",

],

}

)

display(readout)| item | value | |

|---|---|---|

| 0 | Recommended score by held-out top-30 DR value | ATE baseline |

| 1 | Held-out R-loss | 84.69 |

| 2 | Top-30 DR policy gain | 16.97 |

| 3 | Approximate 95% CI for top-30 gain | [16.24, 17.60] |

| 4 | Simulation-only PEHE | 8.44 |

| 5 | Simulation-only true top-30 gain | 17.21 |

| 6 | Main validation caveat | DR validation depends on nuisance quality and ... |

| 7 | Recommended next step | Run a randomized pilot or maintain an explorat... |

Key Takeaways

- Causal ML validation is different because individual treatment effects are unobserved.

- Outcome-prediction metrics do not validate treatment-effect accuracy.

- PEHE is useful in simulation but unavailable in ordinary business data.

- Held-out R-loss is a practical model-selection criterion for CATE scores.

- Doubly robust pseudo-outcomes help evaluate grouped calibration and targeting value.

- Uplift and targeting curves are often the clearest way to communicate ranking performance.

- Top-k policy value links validation to operational capacity.

- Placebo checks catch pipelines that manufacture heterogeneity.

- Overlap and drift diagnostics are model-risk controls, not optional appendices.

- The strongest validation is still prospective: randomized pilots, exploration holdouts, or staged rollouts.

References

Devriendt, F., Van Belle, J., & Guns, T. (2022). Learning to rank for uplift modeling. IEEE Transactions on Knowledge and Data Engineering, 34(10), 4888-4904. https://doi.org/10.1109/tkde.2020.3048510

Gao, Z., Hastie, T., & Tibshirani, R. (2020). Assessment of heterogeneous treatment effect estimation accuracy via matching. arXiv. https://doi.org/10.48550/arxiv.2003.03881

Nie, X., & Wager, S. (2020). Quasi-oracle estimation of heterogeneous treatment effects. Biometrika, 108(2), 299-319. https://doi.org/10.1093/biomet/asaa076

Rothenhausler, D. (2020). Model selection for estimation of causal parameters. arXiv. https://doi.org/10.48550/arxiv.2008.12892

Xu, Y., & Yadlowsky, S. (2022). Calibration error for heterogeneous treatment effects. arXiv. https://doi.org/10.48550/arxiv.2203.13364