import warnings

import graphviz

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import seaborn as sns

import statsmodels.api as sm

from IPython.display import display

from sklearn.ensemble import RandomForestRegressor

from sklearn.metrics import mean_squared_error

from sklearn.model_selection import train_test_split

from sklearn.tree import DecisionTreeRegressor, export_text, plot_tree

warnings.filterwarnings("ignore")

sns.set_theme(style="whitegrid", context="notebook")

pd.set_option("display.float_format", "{:.3f}".format)01. Heterogeneous Treatment Effects

Average treatment effects answer an important first question: did the intervention work on average? Industry decisions usually require a second question: for whom did it work enough to justify action?

This lecture introduces heterogeneous treatment effects (HTE) and the conditional average treatment effect (CATE). We will use a randomized customer-retention experiment to show why treatment effect heterogeneity matters, how to estimate it with transparent subgroup methods and simple interaction models, and how to connect the estimates to a targeting decision.

Learning Goals

By the end of this notebook, you should be able to:

- Define the CATE, subgroup treatment effects, and the relationship between them and the ATE.

- Explain why a strong average effect can still hide unprofitable treatment decisions for some customers.

- Separate prognostic variables from effect modifiers.

- Estimate HTEs with subgroup comparisons, interaction models, and an honest sample-splitting workflow.

- Evaluate a treatment targeting rule using a holdout sample and a known simulation benchmark.

- Translate HTE results into an industry readout that is useful for product, marketing, and operations teams.

def sigmoid(x):

return 1 / (1 + np.exp(-x))

def make_dag(edges, title=None, node_colors=None, rankdir="LR"):

graph = graphviz.Digraph(format="svg")

graph.attr(rankdir=rankdir, bgcolor="white", pad="0.2")

graph.attr("node", shape="box", style="rounded,filled", color="#334155", fontname="Helvetica")

graph.attr("edge", color="#475569", arrowsize="0.8")

node_colors = node_colors or {}

nodes = sorted({node for edge in edges for node in edge[:2]})

for node in nodes:

graph.node(node, fillcolor=node_colors.get(node, "#eef2ff"))

for edge in edges:

if len(edge) == 2:

graph.edge(edge[0], edge[1])

else:

graph.edge(edge[0], edge[1], label=edge[2])

if title:

graph.attr(label=title, labelloc="t", fontsize="18", fontname="Helvetica-Bold")

return graph

def difference_in_means(frame, outcome="outcome", treatment="treatment"):

treated = frame.loc[frame[treatment] == 1, outcome]

control = frame.loc[frame[treatment] == 0, outcome]

estimate = treated.mean() - control.mean()

se = np.sqrt(treated.var(ddof=1) / treated.size + control.var(ddof=1) / control.size)

return {

"estimate": estimate,

"std_error": se,

"ci_low": estimate - 1.96 * se,

"ci_high": estimate + 1.96 * se,

"n_treated": treated.size,

"n_control": control.size,

}

def subgroup_effect_table(frame, group_col, outcome="outcome", treatment="treatment"):

rows = []

for group_name, group_frame in frame.groupby(group_col, observed=True):

stats = difference_in_means(group_frame, outcome=outcome, treatment=treatment)

rows.append(

{

"group": str(group_name),

"n": len(group_frame),

"n_treated": stats["n_treated"],

"n_control": stats["n_control"],

"estimated_effect": stats["estimate"],

"std_error": stats["std_error"],

"ci_low": stats["ci_low"],

"ci_high": stats["ci_high"],

"true_cate_mean": group_frame["true_cate"].mean(),

"mean_risk_score": group_frame["risk_score"].mean(),

}

)

return pd.DataFrame(rows)

def plot_effect_table(table, title, xlabel="Treatment effect", reference=None, figsize=(8, 4)):

plot_data = table.copy().reset_index(drop=True)

y = np.arange(len(plot_data))

xerr = np.vstack(

[

plot_data["estimated_effect"] - plot_data["ci_low"],

plot_data["ci_high"] - plot_data["estimated_effect"],

]

)

fig, ax = plt.subplots(figsize=figsize)

ax.errorbar(

plot_data["estimated_effect"],

y,

xerr=xerr,

fmt="o",

color="#1f77b4",

ecolor="#94a3b8",

capsize=4,

label="Estimated effect",

)

ax.scatter(plot_data["true_cate_mean"], y, marker="D", color="#dc2626", label="True mean CATE")

ax.axvline(0, color="#334155", linewidth=1, linestyle="--")

if reference is not None:

ax.axvline(reference, color="#16a34a", linewidth=1.5, linestyle=":", label="Overall true ATE")

ax.set_yticks(y)

ax.set_yticklabels(plot_data["group"])

ax.set_xlabel(xlabel)

ax.set_title(title)

ax.legend(loc="best")

plt.tight_layout()

return fig, ax

def standardize_features(train, test, feature_cols):

means = train[feature_cols].mean()

stds = train[feature_cols].std(ddof=0).replace(0, 1)

return (train[feature_cols] - means) / stds, (test[feature_cols] - means) / stds, means, stds

def interaction_design(frame, feature_cols, means, stds, treatment="treatment"):

x_std = (frame[feature_cols] - means) / stds

design = pd.DataFrame(index=frame.index)

design["const"] = 1.0

design[treatment] = frame[treatment].astype(float)

for col in feature_cols:

design[col] = x_std[col].astype(float)

design[f"{treatment}_x_{col}"] = frame[treatment].astype(float) * x_std[col].astype(float)

return design

def predict_cate_from_interaction(model, frame, feature_cols, means, stds, treatment="treatment"):

x_std = (frame[feature_cols] - means) / stds

cate_hat = pd.Series(model.params[treatment], index=frame.index, dtype=float)

for col in feature_cols:

cate_hat += model.params.get(f"{treatment}_x_{col}", 0.0) * x_std[col]

return cate_hat1. Where Heterogeneous Effects Fit

Many earlier notebooks focused on identifying an average causal effect. That is the right starting point when the business question is, “Did the intervention work?” HTE becomes necessary when the question becomes, “Who should receive the intervention next?”

Examples:

- Marketing: Which customers should receive a retention offer?

- Product: Which users benefit from onboarding assistance?

- Pricing: Which accounts are harmed by a discount because it trains them to wait for promotions?

- Operations: Which support tickets should be routed to a specialist queue?

- Healthcare: Which patients benefit from a treatment enough to justify side effects or cost?

The main idea is simple: two customers can have the same expected outcome under the current policy but very different expected gains from the new policy. Causal machine learning tries to learn that difference, not just the outcome level.

make_dag(

edges=[

("CustomerCovariates", "UntreatedOutcome"),

("CustomerCovariates", "TreatmentEffect"),

("RandomAssignment", "TreatmentReceived"),

("TreatmentReceived", "ObservedOutcome"),

("UntreatedOutcome", "ObservedOutcome"),

("TreatmentEffect", "ObservedOutcome"),

("EstimatedCATE", "TargetingPolicy"),

("CustomerCovariates", "EstimatedCATE"),

],

title="HTE asks whether covariates modify the causal effect, not only the outcome level",

node_colors={

"CustomerCovariates": "#dbeafe",

"RandomAssignment": "#dcfce7",

"TreatmentReceived": "#fee2e2",

"UntreatedOutcome": "#fef3c7",

"TreatmentEffect": "#e0e7ff",

"ObservedOutcome": "#f1f5f9",

"EstimatedCATE": "#cffafe",

"TargetingPolicy": "#ede9fe",

},

)

The modern HTE literature includes several related streams. Athey and Imbens (2016) developed recursive partitioning methods tailored to heterogeneous causal effects. Wager and Athey (2018) extended this idea to causal forests for nonparametric estimation and inference. Kunzel et al. (2019) organized several “metalearner” strategies that adapt ordinary supervised learning algorithms to estimate CATEs. Hahn et al. (2020) developed Bayesian causal forests for settings with confounding and heterogeneous effects. We will use only simple tools here, but the conceptual spine is the same.

2. Estimands: ATE, Subgroup Effects, and CATE

For a binary treatment \(W \in \{0, 1\}\), let \(Y(1)\) be the potential outcome under treatment and \(Y(0)\) be the potential outcome under control.

The individual causal effect is:

\[ Y_i(1) - Y_i(0) \]

The problem is that we never observe both potential outcomes for the same unit. So most causal estimands average this missing contrast over a population.

The average treatment effect is:

\[ ATE = E[Y(1) - Y(0)] \]

A subgroup treatment effect averages over a group \(G\):

\[ E[Y(1) - Y(0) \mid G] \]

The conditional average treatment effect conditions on features \(X=x\):

\[ \tau(x) = E[Y(1) - Y(0) \mid X=x] \]

The ATE is the population average of the CATE:

\[ ATE = E[\tau(X)] \]

This relationship matters in practice. If the CATE varies a lot, the ATE can be a poor guide for a constrained targeting decision.

3. Running Example: Retention Outreach

Imagine a SaaS company runs a randomized experiment. Half of eligible accounts receive a proactive retention offer; half do not. The outcome is next-quarter net revenue from the account. Higher is better.

The company has a budget constraint. It cannot contact every account every quarter. The decision is therefore not merely whether the offer works on average. The decision is which accounts should receive it.

We will simulate the experiment so that the ground truth is known. Real projects do not have access to the true CATE, but simulation lets us check whether our estimators are learning the right pattern.

def simulate_retention_experiment(n=12_000, seed=5101):

rng = np.random.default_rng(seed)

risk_score = rng.beta(2.2, 2.8, n)

usage_z = rng.normal(0, 1, n)

customer_value = rng.lognormal(mean=4.2, sigma=0.55, size=n)

tenure_months = rng.gamma(shape=2.2, scale=10, size=n)

enterprise_plan = rng.binomial(1, sigmoid(-0.4 + 0.55 * (np.log(customer_value) - 4.2)))

support_tickets = rng.poisson(np.clip(1.2 + 2.5 * risk_score - 0.3 * usage_z, 0.1, None))

treatment = rng.binomial(1, 0.5, n)

mu0 = (

65

+ 0.16 * customer_value

+ 6.0 * usage_z

- 10.0 * risk_score

+ 4.0 * enterprise_plan

+ 0.12 * tenure_months

- 1.5 * support_tickets

+ 3.0 * np.sin(usage_z)

)

true_cate = (

-4.0

+ 15.0 * risk_score

+ 2.5 * enterprise_plan

- 2.0 * (usage_z > 1.0).astype(float)

+ 1.5 * (support_tickets >= 4).astype(float)

)

true_y0 = mu0 + rng.normal(0, 6, n)

true_y1 = true_y0 + true_cate

outcome = np.where(treatment == 1, true_y1, true_y0)

return pd.DataFrame(

{

"account_id": np.arange(1, n + 1),

"risk_score": risk_score,

"usage_z": usage_z,

"customer_value": customer_value,

"tenure_months": tenure_months,

"enterprise_plan": enterprise_plan,

"support_tickets": support_tickets,

"treatment": treatment,

"true_y0": true_y0,

"true_y1": true_y1,

"outcome": outcome,

"true_cate": true_cate,

"mu0": mu0,

}

)

df = simulate_retention_experiment()

summary = pd.DataFrame(

{

"quantity": [

"Accounts",

"Treatment share",

"Average observed outcome",

"True average treatment effect",

"Share with positive true CATE",

],

"value": [

len(df),

df["treatment"].mean(),

df["outcome"].mean(),

df["true_cate"].mean(),

(df["true_cate"] > 0).mean(),

],

}

)

display(summary)

display(df.head())| quantity | value | |

|---|---|---|

| 0 | Accounts | 12000.000 |

| 1 | Treatment share | 0.503 |

| 2 | Average observed outcome | 75.456 |

| 3 | True average treatment effect | 3.545 |

| 4 | Share with positive true CATE | 0.826 |

| account_id | risk_score | usage_z | customer_value | tenure_months | enterprise_plan | support_tickets | treatment | true_y0 | true_y1 | outcome | true_cate | mu0 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1 | 0.366 | -0.093 | 40.829 | 7.098 | 0 | 0 | 1 | 62.106 | 63.603 | 63.603 | 1.497 | 67.886 |

| 1 | 2 | 0.510 | 1.814 | 89.383 | 13.337 | 1 | 6 | 0 | 93.132 | 98.776 | 93.132 | 5.644 | 84.601 |

| 2 | 3 | 0.598 | -0.205 | 75.784 | 35.492 | 1 | 2 | 1 | 78.781 | 86.250 | 86.250 | 7.469 | 74.568 |

| 3 | 4 | 0.284 | -0.270 | 362.404 | 10.335 | 1 | 1 | 1 | 116.755 | 119.509 | 119.509 | 2.754 | 121.466 |

| 4 | 5 | 0.540 | 1.222 | 42.532 | 28.366 | 0 | 3 | 1 | 68.803 | 70.901 | 70.901 | 2.098 | 75.461 |

The treatment is randomized, so treatment assignment is independent of the customer features. That makes the ATE easy to estimate. The hard part is that each account still contributes only one observed outcome.

In the simulated data we store both potential outcomes for teaching purposes. In a real experiment, the untreated potential outcome for treated accounts and the treated potential outcome for control accounts are counterfactual and therefore unobserved.

sample_units = df.sample(8, random_state=12).copy()

sample_units["observed_arm"] = np.where(sample_units["treatment"] == 1, "treated", "control")

sample_units["counterfactual_not_observed"] = np.where(

sample_units["treatment"] == 1,

"Y(0)",

"Y(1)",

)

display(

sample_units[

[

"account_id",

"observed_arm",

"risk_score",

"usage_z",

"support_tickets",

"outcome",

"true_y0",

"true_y1",

"true_cate",

"counterfactual_not_observed",

]

].round(3)

)| account_id | observed_arm | risk_score | usage_z | support_tickets | outcome | true_y0 | true_y1 | true_cate | counterfactual_not_observed | |

|---|---|---|---|---|---|---|---|---|---|---|

| 437 | 438 | control | 0.642 | -0.890 | 5 | 57.666 | 57.666 | 64.797 | 7.131 | Y(1) |

| 7619 | 7620 | treated | 0.958 | -1.784 | 2 | 54.391 | 44.024 | 54.391 | 10.366 | Y(0) |

| 4014 | 4015 | treated | 0.641 | 0.253 | 2 | 77.639 | 72.029 | 77.639 | 5.609 | Y(0) |

| 3862 | 3863 | treated | 0.109 | -0.165 | 1 | 74.136 | 76.506 | 74.136 | -2.370 | Y(0) |

| 4351 | 4352 | control | 0.322 | -1.482 | 1 | 65.522 | 65.522 | 66.354 | 0.832 | Y(1) |

| 1850 | 1851 | treated | 0.252 | -0.882 | 4 | 51.176 | 49.890 | 51.176 | 1.285 | Y(0) |

| 3202 | 3203 | treated | 0.711 | -0.157 | 3 | 75.472 | 66.301 | 75.472 | 9.172 | Y(0) |

| 1155 | 1156 | control | 0.414 | -1.213 | 2 | 63.590 | 63.590 | 65.797 | 2.207 | Y(1) |

The table is intentionally a little uncomfortable: it shows the hidden potential outcomes because we are in a simulation. In live experimentation, the true_y0, true_y1, and true_cate columns are exactly what we wish we had and do not observe.

4. Start With the Average Effect

Because the experiment is randomized, the difference in mean outcomes between treated and control accounts is an unbiased estimate of the ATE:

\[ E[Y \mid W=1] - E[Y \mid W=0] \]

This is still the first thing to report. HTE analysis should not replace the average effect; it should explain where the average effect comes from and whether the treatment should be targeted.

ate_stats = difference_in_means(df)

ate_table = pd.DataFrame(

{

"quantity": [

"Estimated ATE",

"Robust standard error",

"95% CI lower",

"95% CI upper",

"True ATE from simulation",

"Estimation error",

],

"value": [

ate_stats["estimate"],

ate_stats["std_error"],

ate_stats["ci_low"],

ate_stats["ci_high"],

df["true_cate"].mean(),

ate_stats["estimate"] - df["true_cate"].mean(),

],

}

)

display(ate_table.round(3))| quantity | value | |

|---|---|---|

| 0 | Estimated ATE | 3.634 |

| 1 | Robust standard error | 0.240 |

| 2 | 95% CI lower | 3.163 |

| 3 | 95% CI upper | 4.104 |

| 4 | True ATE from simulation | 3.545 |

| 5 | Estimation error | 0.089 |

The estimated ATE is close to the true simulated ATE. If the company only needed a yes-or-no answer about the offer, this would be a strong start.

But the positive average effect does not tell us whether every account should be contacted. The average can be positive even when some accounts have small, zero, or negative effects.

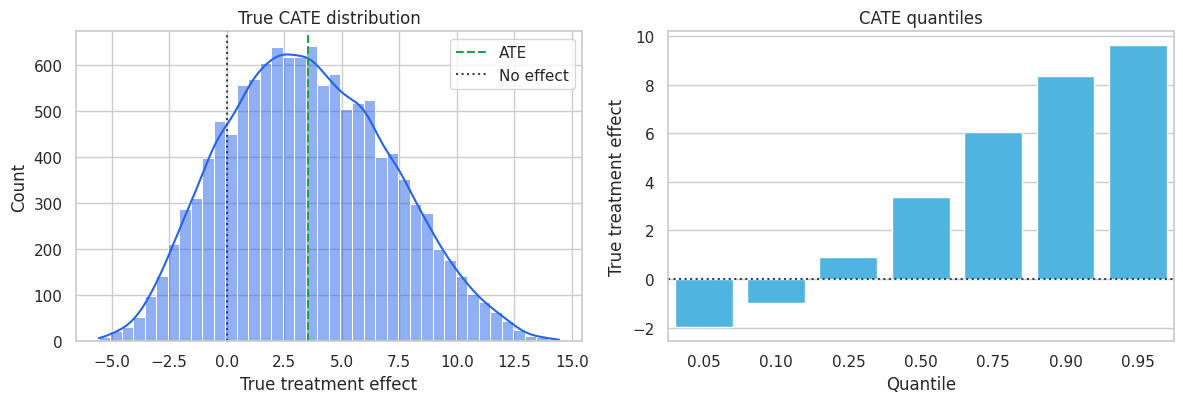

fig, axes = plt.subplots(1, 2, figsize=(12, 4.2))

sns.histplot(df["true_cate"], bins=40, kde=True, color="#2563eb", ax=axes[0])

axes[0].axvline(df["true_cate"].mean(), color="#16a34a", linestyle="--", label="ATE")

axes[0].axvline(0, color="#334155", linestyle=":", label="No effect")

axes[0].set_title("True CATE distribution")

axes[0].set_xlabel("True treatment effect")

axes[0].legend()

quantiles = df["true_cate"].quantile([0.05, 0.10, 0.25, 0.50, 0.75, 0.90, 0.95]).reset_index()

quantiles.columns = ["quantile", "true_cate"]

sns.barplot(data=quantiles, x="quantile", y="true_cate", color="#38bdf8", ax=axes[1])

axes[1].axhline(0, color="#334155", linestyle=":")

axes[1].set_title("CATE quantiles")

axes[1].set_xlabel("Quantile")

axes[1].set_ylabel("True treatment effect")

axes[1].set_xticklabels([f"{q:.2f}" for q in quantiles["quantile"]])

plt.tight_layout()

plt.show()

heterogeneity_summary = pd.DataFrame(

{

"quantity": [

"True ATE",

"True CATE standard deviation",

"Minimum true CATE",

"Median true CATE",

"Maximum true CATE",

"Share with negative true CATE",

],

"value": [

df["true_cate"].mean(),

df["true_cate"].std(),

df["true_cate"].min(),

df["true_cate"].median(),

df["true_cate"].max(),

(df["true_cate"] < 0).mean(),

],

}

)

display(heterogeneity_summary.round(3))

| quantity | value | |

|---|---|---|

| 0 | True ATE | 3.545 |

| 1 | True CATE standard deviation | 3.539 |

| 2 | Minimum true CATE | -5.554 |

| 3 | Median true CATE | 3.390 |

| 4 | Maximum true CATE | 14.450 |

| 5 | Share with negative true CATE | 0.174 |

The offer has a positive average effect, but not everyone benefits. This is the central reason HTE analysis matters. A policy that treats all eligible accounts may be acceptable when the intervention is cheap and harmless. A policy with cost, capacity limits, or customer-experience risk should use the heterogeneity.

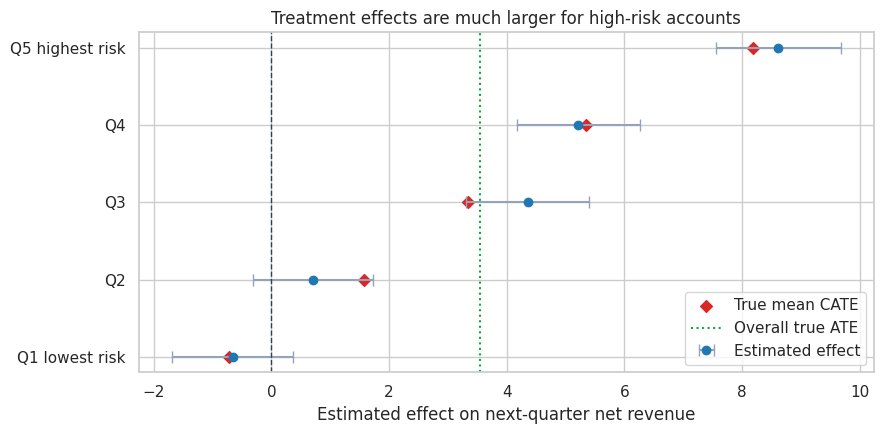

5. Transparent Subgroup Effects

Before using flexible machine learning, start with interpretable subgroup estimates. They are easy to explain, easy to audit, and often enough to identify the main pattern.

Here we split accounts into risk-score quintiles. Within each quintile, treatment was still randomized, so a difference in means estimates the subgroup treatment effect.

df["risk_quintile"] = pd.qcut(

df["risk_score"],

q=5,

labels=["Q1 lowest risk", "Q2", "Q3", "Q4", "Q5 highest risk"],

)

risk_table = subgroup_effect_table(df, "risk_quintile")

display(risk_table.round(3))

plot_effect_table(

risk_table,

title="Treatment effects are much larger for high-risk accounts",

xlabel="Estimated effect on next-quarter net revenue",

reference=df["true_cate"].mean(),

figsize=(9, 4.5),

)

plt.show()| group | n | n_treated | n_control | estimated_effect | std_error | ci_low | ci_high | true_cate_mean | mean_risk_score | |

|---|---|---|---|---|---|---|---|---|---|---|

| 0 | Q1 lowest risk | 2400 | 1194 | 1206 | -0.659 | 0.524 | -1.686 | 0.368 | -0.719 | 0.164 |

| 1 | Q2 | 2400 | 1203 | 1197 | 0.703 | 0.518 | -0.312 | 1.718 | 1.570 | 0.309 |

| 2 | Q3 | 2400 | 1206 | 1194 | 4.355 | 0.534 | 3.307 | 5.402 | 3.345 | 0.424 |

| 3 | Q4 | 2400 | 1232 | 1168 | 5.219 | 0.534 | 4.172 | 6.265 | 5.349 | 0.549 |

| 4 | Q5 highest risk | 2400 | 1203 | 1197 | 8.614 | 0.541 | 7.555 | 9.674 | 8.180 | 0.736 |

The subgroup pattern is clear: high-risk accounts benefit more from outreach. The low-risk group has little need for the intervention and can even have a negative effect in this simulation. That is plausible in many product settings: unnecessary interventions can annoy low-risk customers, discount customers who would have stayed anyway, or consume support capacity without much gain.

Subgroup analysis has two advantages:

- It is directly connected to a decision rule: treat higher-risk accounts first.

- It gives stakeholders a concrete mental model before more flexible models are introduced.

It also has limitations. Quintiles are arbitrary, and one feature at a time cannot represent interactions such as “high risk and enterprise plan” or “high risk but already very engaged.”

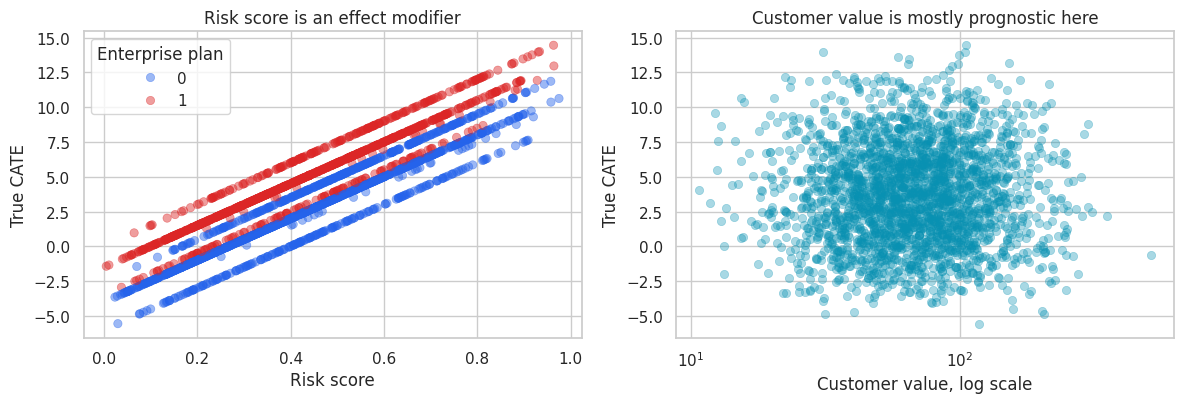

6. Prognostic Variables Are Not Automatically Effect Modifiers

A prognostic variable predicts the outcome level. An effect modifier predicts the treatment effect.

These are different roles:

\[ \mu_0(x) = E[Y(0) \mid X=x] \]

\[ \tau(x) = E[Y(1) - Y(0) \mid X=x] \]

A customer can have high expected revenue under control and still receive little incremental benefit from outreach. Another customer can have lower expected revenue under control but respond strongly to treatment.

This distinction is one of the most common places where predictive modeling and causal modeling diverge.

feature_cols_raw = [

"risk_score",

"usage_z",

"customer_value",

"tenure_months",

"enterprise_plan",

"support_tickets",

]

correlation_rows = []

for col in feature_cols_raw:

correlation_rows.append(

{

"feature": col,

"corr_with_untreated_outcome": df[col].corr(df["true_y0"]),

"corr_with_true_cate": df[col].corr(df["true_cate"]),

}

)

corr_table = pd.DataFrame(correlation_rows).sort_values("corr_with_true_cate", ascending=False)

display(corr_table.round(3))

sample_for_plot = df.sample(2500, random_state=44)

fig, axes = plt.subplots(1, 2, figsize=(12, 4.2))

sns.scatterplot(

data=sample_for_plot,

x="risk_score",

y="true_cate",

hue="enterprise_plan",

palette=["#2563eb", "#dc2626"],

alpha=0.45,

edgecolor=None,

ax=axes[0],

)

axes[0].set_title("Risk score is an effect modifier")

axes[0].set_xlabel("Risk score")

axes[0].set_ylabel("True CATE")

axes[0].legend(title="Enterprise plan")

sns.scatterplot(

data=sample_for_plot,

x="customer_value",

y="true_cate",

color="#0891b2",

alpha=0.35,

edgecolor=None,

ax=axes[1],

)

axes[1].set_xscale("log")

axes[1].set_title("Customer value is mostly prognostic here")

axes[1].set_xlabel("Customer value, log scale")

axes[1].set_ylabel("True CATE")

plt.tight_layout()

plt.show()| feature | corr_with_untreated_outcome | corr_with_true_cate | |

|---|---|---|---|

| 0 | risk_score | -0.212 | 0.895 |

| 5 | support_tickets | -0.330 | 0.418 |

| 4 | enterprise_plan | 0.212 | 0.339 |

| 2 | customer_value | 0.547 | 0.036 |

| 3 | tenure_months | 0.142 | -0.003 |

| 1 | usage_z | 0.602 | -0.158 |

The correlation table shows two different kinds of information. Customer value is strongly related to the untreated outcome because valuable accounts generate more revenue even without outreach. Risk score and support tickets are more informative about treatment responsiveness.

A purely predictive model that ranks customers by expected revenue may therefore target expensive accounts that would have stayed anyway. A CATE model tries to rank customers by incremental lift.

7. A Linear Interaction Model for CATE

A simple interaction model is often the best first CATE model. It keeps the link between coefficients and business interpretation visible.

The model is:

\[ Y_i = \alpha + \beta W_i + X_i'\gamma + W_i X_i'\delta + \epsilon_i \]

For a customer with features \(x\), the implied CATE is:

\[ \hat{\tau}(x) = \hat{\beta} + x'\hat{\delta} \]

The interaction coefficients \(\delta\) tell us how the treatment effect changes with the features. This model is not as flexible as a causal forest or metalearner, but it is a useful baseline and a strong communication tool.

df_model = df.copy()

df_model["log_customer_value"] = np.log(df_model["customer_value"])

feature_cols = [

"risk_score",

"usage_z",

"log_customer_value",

"tenure_months",

"enterprise_plan",

"support_tickets",

]

train_df, test_df = train_test_split(df_model, test_size=0.35, random_state=27, stratify=df_model["treatment"])

_, _, feature_means, feature_stds = standardize_features(train_df, test_df, feature_cols)

X_train = interaction_design(train_df, feature_cols, feature_means, feature_stds)

y_train = train_df["outcome"].astype(float)

interaction_model = sm.OLS(y_train, X_train).fit(cov_type="HC3")

coef_rows = []

for term in ["treatment"] + [f"treatment_x_{col}" for col in feature_cols]:

coef_rows.append(

{

"term": term,

"estimate": interaction_model.params[term],

"std_error": interaction_model.bse[term],

"ci_low": interaction_model.conf_int().loc[term, 0],

"ci_high": interaction_model.conf_int().loc[term, 1],

"p_value": interaction_model.pvalues[term],

}

)

interaction_table = pd.DataFrame(coef_rows)

display(interaction_table.round(3))| term | estimate | std_error | ci_low | ci_high | p_value | |

|---|---|---|---|---|---|---|

| 0 | treatment | 3.676 | 0.152 | 3.379 | 3.974 | 0.000 |

| 1 | treatment_x_risk_score | 3.342 | 0.161 | 3.027 | 3.657 | 0.000 |

| 2 | treatment_x_usage_z | -0.488 | 0.163 | -0.807 | -0.169 | 0.003 |

| 3 | treatment_x_log_customer_value | 0.196 | 0.222 | -0.238 | 0.631 | 0.376 |

| 4 | treatment_x_tenure_months | -0.214 | 0.155 | -0.517 | 0.089 | 0.166 |

| 5 | treatment_x_enterprise_plan | 1.363 | 0.150 | 1.069 | 1.656 | 0.000 |

| 6 | treatment_x_support_tickets | 0.610 | 0.166 | 0.285 | 0.935 | 0.000 |

The coefficient on treatment is the estimated treatment effect for an account with average standardized covariates. The interaction terms show how the effect changes as the features move away from their averages.

Because we standardized the continuous features, the interaction coefficients are easier to compare: a one-standard-deviation increase in risk score has a much larger positive effect than a one-standard-deviation change in most other features.

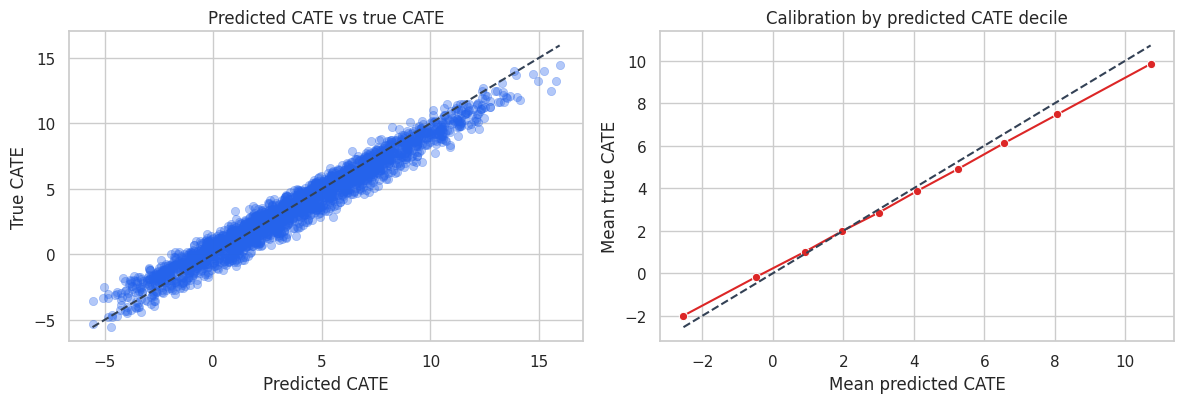

test_df = test_df.copy()

test_df["cate_hat_interaction"] = predict_cate_from_interaction(

interaction_model,

test_df,

feature_cols,

feature_means,

feature_stds,

)

cate_corr = np.corrcoef(test_df["cate_hat_interaction"], test_df["true_cate"])[0, 1]

cate_rmse = np.sqrt(mean_squared_error(test_df["true_cate"], test_df["cate_hat_interaction"]))

metrics = pd.DataFrame(

{

"metric": ["Correlation with true CATE", "CATE RMSE", "Mean predicted CATE", "Mean true CATE"],

"value": [

cate_corr,

cate_rmse,

test_df["cate_hat_interaction"].mean(),

test_df["true_cate"].mean(),

],

}

)

display(metrics.round(3))

calibration = test_df.copy()

calibration["predicted_cate_decile"] = pd.qcut(

calibration["cate_hat_interaction"],

10,

labels=[f"D{i}" for i in range(1, 11)],

)

calibration_table = (

calibration.groupby("predicted_cate_decile", observed=True)

.agg(

n=("account_id", "count"),

mean_predicted_cate=("cate_hat_interaction", "mean"),

mean_true_cate=("true_cate", "mean"),

)

.reset_index()

)

display(calibration_table.round(3))

fig, axes = plt.subplots(1, 2, figsize=(12, 4.2))

plot_sample = test_df.sample(2500, random_state=19)

sns.scatterplot(

data=plot_sample,

x="cate_hat_interaction",

y="true_cate",

alpha=0.35,

edgecolor=None,

color="#2563eb",

ax=axes[0],

)

line_min = min(plot_sample["cate_hat_interaction"].min(), plot_sample["true_cate"].min())

line_max = max(plot_sample["cate_hat_interaction"].max(), plot_sample["true_cate"].max())

axes[0].plot([line_min, line_max], [line_min, line_max], color="#334155", linestyle="--")

axes[0].set_title("Predicted CATE vs true CATE")

axes[0].set_xlabel("Predicted CATE")

axes[0].set_ylabel("True CATE")

sns.lineplot(

data=calibration_table,

x="mean_predicted_cate",

y="mean_true_cate",

marker="o",

color="#dc2626",

ax=axes[1],

)

cal_min = min(calibration_table["mean_predicted_cate"].min(), calibration_table["mean_true_cate"].min())

cal_max = max(calibration_table["mean_predicted_cate"].max(), calibration_table["mean_true_cate"].max())

axes[1].plot([cal_min, cal_max], [cal_min, cal_max], color="#334155", linestyle="--")

axes[1].set_title("Calibration by predicted CATE decile")

axes[1].set_xlabel("Mean predicted CATE")

axes[1].set_ylabel("Mean true CATE")

plt.tight_layout()

plt.show()| metric | value | |

|---|---|---|

| 0 | Correlation with true CATE | 0.979 |

| 1 | CATE RMSE | 0.841 |

| 2 | Mean predicted CATE | 3.754 |

| 3 | Mean true CATE | 3.587 |

| predicted_cate_decile | n | mean_predicted_cate | mean_true_cate | |

|---|---|---|---|---|

| 0 | D1 | 420 | -2.536 | -1.995 |

| 1 | D2 | 420 | -0.470 | -0.170 |

| 2 | D3 | 420 | 0.900 | 1.002 |

| 3 | D4 | 420 | 1.962 | 1.980 |

| 4 | D5 | 420 | 3.005 | 2.853 |

| 5 | D6 | 420 | 4.101 | 3.875 |

| 6 | D7 | 420 | 5.241 | 4.893 |

| 7 | D8 | 420 | 6.552 | 6.115 |

| 8 | D9 | 420 | 8.072 | 7.474 |

| 9 | D10 | 420 | 10.717 | 9.845 |

In this simulation, the interaction model recovers the broad CATE pattern well. That is not guaranteed in real data. It works here because the true effect is mostly a smooth function of a few measured covariates.

The calibration table is especially useful for industry work. We usually cannot verify individual treatment effects, but we can ask whether customers in higher predicted CATE buckets have higher experimental lift on average.

8. Honest Subgroup Discovery

A major risk in HTE analysis is searching for subgroups and estimating their effects on the same data. The more cuts we try, the more likely we are to find an impressive subgroup by chance.

Athey and Imbens (2016) emphasized honesty: use one part of the data to discover the partition, and another part to estimate effects within the discovered leaves. This is not the only way to do valid HTE inference, but it is an excellent workflow principle.

For a randomized experiment with treatment probability \(e=0.5\), one simple transformed outcome is:

\[ Y_i^* = Y_i \frac{W_i - e}{e(1-e)} \]

Under random assignment, the conditional expectation of this transformed outcome is the CATE:

\[ E[Y_i^* \mid X_i=x] = \tau(x) \]

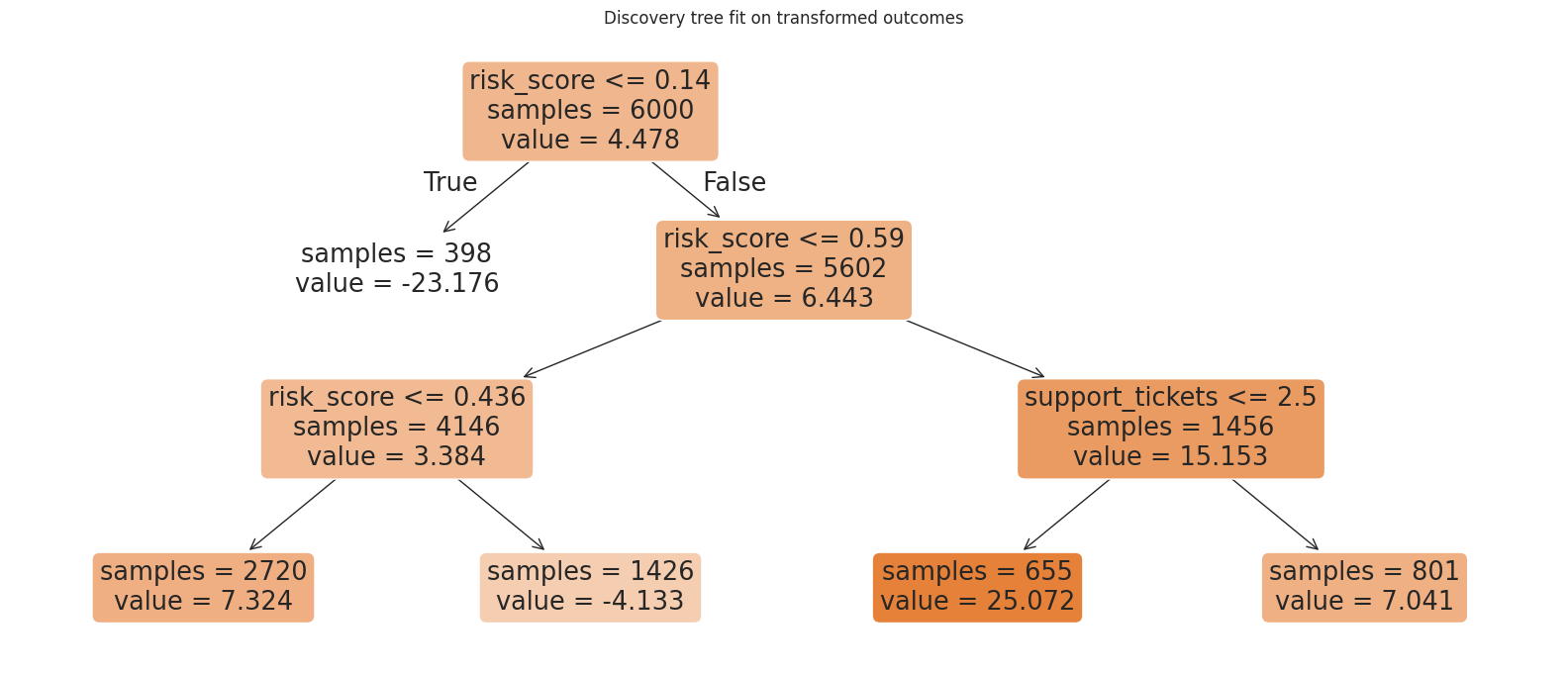

We will fit a shallow tree to this transformed outcome on a discovery sample, then estimate treatment effects in the resulting leaves on a holdout sample.

tree_features = [

"risk_score",

"usage_z",

"log_customer_value",

"tenure_months",

"enterprise_plan",

"support_tickets",

]

experiment_discovery, experiment_holdout = train_test_split(

df_model,

test_size=0.50,

random_state=99,

stratify=df_model["treatment"],

)

propensity = 0.5

pseudo_outcome = experiment_discovery["outcome"] * (

experiment_discovery["treatment"] - propensity

) / (propensity * (1 - propensity))

tree = DecisionTreeRegressor(max_depth=3, min_samples_leaf=350, random_state=11)

tree.fit(experiment_discovery[tree_features], pseudo_outcome)

print(export_text(tree, feature_names=tree_features, decimals=2))

fig, ax = plt.subplots(figsize=(16, 7))

plot_tree(

tree,

feature_names=tree_features,

filled=True,

rounded=True,

impurity=False,

ax=ax,

)

ax.set_title("Discovery tree fit on transformed outcomes")

plt.tight_layout()

plt.show()|--- risk_score <= 0.14

| |--- value: [-23.18]

|--- risk_score > 0.14

| |--- risk_score <= 0.59

| | |--- risk_score <= 0.44

| | | |--- value: [7.32]

| | |--- risk_score > 0.44

| | | |--- value: [-4.13]

| |--- risk_score > 0.59

| | |--- support_tickets <= 2.50

| | | |--- value: [25.07]

| | |--- support_tickets > 2.50

| | | |--- value: [7.04]

The tree is a discovery device. Its splits should be treated as hypotheses generated from data, not as final causal estimates. The next step estimates the treatment effect in each discovered leaf using data that the tree did not use for splitting.

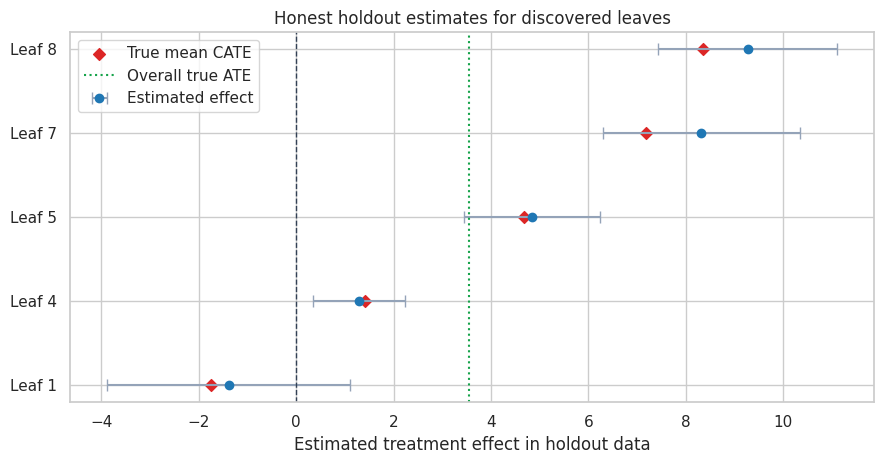

holdout = experiment_holdout.copy()

holdout["leaf_id"] = tree.apply(holdout[tree_features])

leaf_table = subgroup_effect_table(holdout, "leaf_id")

leaf_table = leaf_table.sort_values("estimated_effect").reset_index(drop=True)

leaf_table["group"] = [f"Leaf {leaf}" for leaf in leaf_table["group"]]

leaf_table["share_of_holdout"] = leaf_table["n"] / len(holdout)

display(

leaf_table[

[

"group",

"n",

"share_of_holdout",

"mean_risk_score",

"estimated_effect",

"std_error",

"ci_low",

"ci_high",

"true_cate_mean",

]

].round(3)

)

plot_effect_table(

leaf_table,

title="Honest holdout estimates for discovered leaves",

xlabel="Estimated treatment effect in holdout data",

reference=df["true_cate"].mean(),

figsize=(9, 4.8),

)

plt.show()| group | n | share_of_holdout | mean_risk_score | estimated_effect | std_error | ci_low | ci_high | true_cate_mean | |

|---|---|---|---|---|---|---|---|---|---|

| 0 | Leaf 1 | 381 | 0.064 | 0.094 | -1.388 | 1.275 | -3.887 | 1.112 | -1.757 |

| 1 | Leaf 4 | 2752 | 0.459 | 0.300 | 1.282 | 0.483 | 0.336 | 2.228 | 1.423 |

| 2 | Leaf 5 | 1440 | 0.240 | 0.510 | 4.845 | 0.709 | 3.455 | 6.235 | 4.686 |

| 3 | Leaf 7 | 643 | 0.107 | 0.703 | 8.314 | 1.030 | 6.294 | 10.333 | 7.188 |

| 4 | Leaf 8 | 784 | 0.131 | 0.723 | 9.266 | 0.942 | 7.420 | 11.111 | 8.360 |

The holdout estimates are noisier than the true leaf means, but they protect us from reporting purely in-sample discoveries as if they were confirmed effects. This matters in high-dimensional business datasets where hundreds of plausible segments can be searched.

A production-grade HTE workflow often repeats this logic with cross-fitting, causal forests, or doubly robust scores. Shin and Antonelli (2023) discuss doubly robust approaches for HTE inference, while Wager and Athey (2018) develop causal forests for nonparametric HTE estimation and inference.

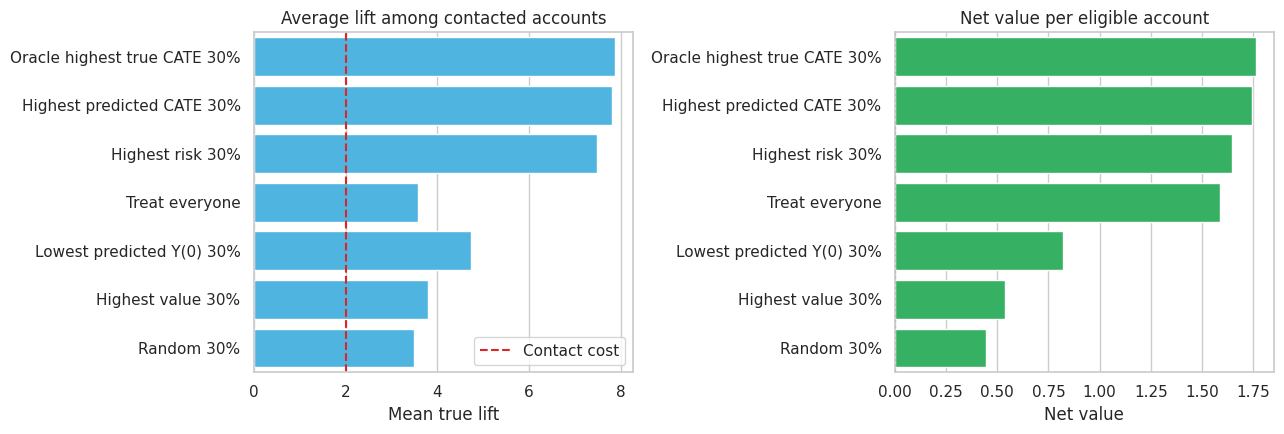

9. From CATE to Targeting

CATE estimates become operationally useful when we convert them into a policy. Suppose the company can contact only 30% of eligible accounts. Which accounts should receive the retention offer?

We will compare several rules on the test sample:

- Treat everyone.

- Randomly contact 30%.

- Contact the highest-risk 30%.

- Contact the highest-value 30%.

- Contact the lowest predicted untreated-outcome 30%.

- Contact the highest predicted-CATE 30% using the interaction model.

- Oracle rule: contact the highest true-CATE 30%. This is not available in real life, but it gives a benchmark.

To include a practical constraint, assume the contact costs 2 revenue units per contacted account. A policy’s net value per eligible account is:

\[ \text{Policy value} = P(\text{contact}) \times E[\tau(X) - c \mid \text{contact}] \]

where \(c\) is the contact cost.

control_train = train_df.loc[train_df["treatment"] == 0].copy()

rf_baseline = RandomForestRegressor(

n_estimators=300,

min_samples_leaf=25,

random_state=202,

n_jobs=-1,

)

rf_baseline.fit(control_train[tree_features], control_train["outcome"])

test_policy = test_df.copy()

test_policy["predicted_y0"] = rf_baseline.predict(test_policy[tree_features])

contact_share = 0.30

contact_cost = 2.0

n_contact = int(np.floor(contact_share * len(test_policy)))

rng = np.random.default_rng(2026)

random_contact = pd.Series(False, index=test_policy.index)

random_contact.loc[rng.choice(test_policy.index.to_numpy(), size=n_contact, replace=False)] = True

def top_fraction_mask(series, fraction=0.30, largest=True):

cutoff_n = int(np.floor(fraction * len(series)))

selected_index = series.sort_values(ascending=not largest).head(cutoff_n).index

mask = pd.Series(False, index=series.index)

mask.loc[selected_index] = True

return mask

policy_masks = {

"Treat everyone": pd.Series(True, index=test_policy.index),

"Random 30%": random_contact,

"Highest risk 30%": top_fraction_mask(test_policy["risk_score"], contact_share, largest=True),

"Highest value 30%": top_fraction_mask(test_policy["customer_value"], contact_share, largest=True),

"Lowest predicted Y(0) 30%": top_fraction_mask(test_policy["predicted_y0"], contact_share, largest=False),

"Highest predicted CATE 30%": top_fraction_mask(test_policy["cate_hat_interaction"], contact_share, largest=True),

"Oracle highest true CATE 30%": top_fraction_mask(test_policy["true_cate"], contact_share, largest=True),

}

policy_rows = []

for policy_name, mask in policy_masks.items():

targeted = test_policy.loc[mask]

policy_rows.append(

{

"policy": policy_name,

"target_share": mask.mean(),

"mean_true_lift_if_targeted": targeted["true_cate"].mean(),

"share_negative_lift_targeted": (targeted["true_cate"] < 0).mean(),

"net_value_per_eligible_account": mask.mean() * (targeted["true_cate"].mean() - contact_cost),

}

)

policy_table = pd.DataFrame(policy_rows).sort_values("net_value_per_eligible_account", ascending=False)

display(policy_table.round(3))| policy | target_share | mean_true_lift_if_targeted | share_negative_lift_targeted | net_value_per_eligible_account | |

|---|---|---|---|---|---|

| 6 | Oracle highest true CATE 30% | 0.300 | 7.878 | 0.000 | 1.763 |

| 5 | Highest predicted CATE 30% | 0.300 | 7.811 | 0.000 | 1.743 |

| 2 | Highest risk 30% | 0.300 | 7.487 | 0.000 | 1.646 |

| 0 | Treat everyone | 1.000 | 3.587 | 0.168 | 1.587 |

| 4 | Lowest predicted Y(0) 30% | 0.300 | 4.740 | 0.084 | 0.822 |

| 3 | Highest value 30% | 0.300 | 3.789 | 0.154 | 0.537 |

| 1 | Random 30% | 0.300 | 3.487 | 0.164 | 0.446 |

fig, axes = plt.subplots(1, 2, figsize=(13, 4.5))

sns.barplot(

data=policy_table,

y="policy",

x="mean_true_lift_if_targeted",

color="#38bdf8",

ax=axes[0],

)

axes[0].axvline(contact_cost, color="#dc2626", linestyle="--", label="Contact cost")

axes[0].set_title("Average lift among contacted accounts")

axes[0].set_xlabel("Mean true lift")

axes[0].set_ylabel("")

axes[0].legend(loc="lower right")

sns.barplot(

data=policy_table,

y="policy",

x="net_value_per_eligible_account",

color="#22c55e",

ax=axes[1],

)

axes[1].axvline(0, color="#334155", linestyle=":")

axes[1].set_title("Net value per eligible account")

axes[1].set_xlabel("Net value")

axes[1].set_ylabel("")

plt.tight_layout()

plt.show()

The CATE-based rule is close to the oracle benchmark and beats policies based only on high value or low predicted baseline outcome. This is the practical point of HTE modeling: ranking by expected outcome is not the same as ranking by expected incremental effect.

The treat-everyone policy can still have positive total value if the average effect is high enough. But when the budget is constrained or contact has customer-experience costs, the CATE-based rule can create more value per contacted account and avoid accounts with low or negative lift.

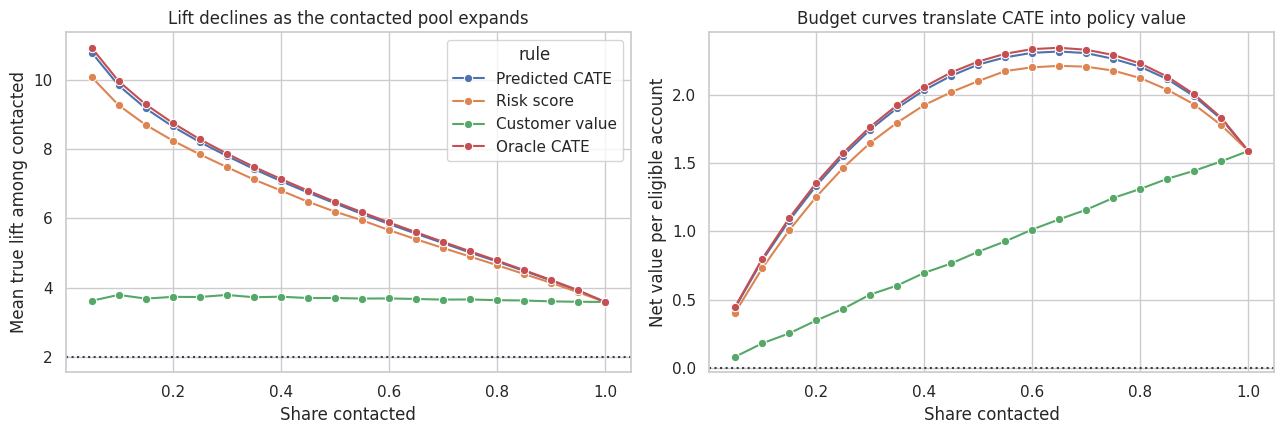

fractions = np.linspace(0.05, 1.00, 20)

curve_rows = []

for fraction in fractions:

for label, score, largest in [

("Predicted CATE", test_policy["cate_hat_interaction"], True),

("Risk score", test_policy["risk_score"], True),

("Customer value", test_policy["customer_value"], True),

("Oracle CATE", test_policy["true_cate"], True),

]:

mask = top_fraction_mask(score, fraction, largest=largest)

targeted = test_policy.loc[mask]

curve_rows.append(

{

"contact_share": fraction,

"rule": label,

"mean_true_lift_targeted": targeted["true_cate"].mean(),

"net_value_per_account": mask.mean() * (targeted["true_cate"].mean() - contact_cost),

}

)

curve_table = pd.DataFrame(curve_rows)

fig, axes = plt.subplots(1, 2, figsize=(13, 4.5))

sns.lineplot(

data=curve_table,

x="contact_share",

y="mean_true_lift_targeted",

hue="rule",

marker="o",

ax=axes[0],

)

axes[0].axhline(contact_cost, color="#334155", linestyle=":")

axes[0].set_title("Lift declines as the contacted pool expands")

axes[0].set_xlabel("Share contacted")

axes[0].set_ylabel("Mean true lift among contacted")

sns.lineplot(

data=curve_table,

x="contact_share",

y="net_value_per_account",

hue="rule",

marker="o",

ax=axes[1],

)

axes[1].axhline(0, color="#334155", linestyle=":")

axes[1].set_title("Budget curves translate CATE into policy value")

axes[1].set_xlabel("Share contacted")

axes[1].set_ylabel("Net value per eligible account")

axes[1].legend_.remove()

plt.tight_layout()

plt.show()

Budget curves are often more useful than a single top-30% policy. They show what happens as the available treatment capacity changes. A business team can use this view to choose a rollout threshold, estimate marginal returns, or negotiate campaign capacity.

10. How to Validate HTE Models in Practice

HTE validation is harder than outcome-prediction validation because individual treatment effects are unobserved. We cannot compute a row-level error metric like we can for prediction.

Useful validation strategies include:

- Holdout experimental lift by predicted-CATE bucket.

- Calibration curves comparing predicted CATE buckets with observed treatment-control differences.

- Policy value on a randomized holdout sample.

- Stability of discovered subgroups across time, geography, or cohorts.

- Sensitivity to feature sets, nuisance models, and targeting thresholds.

- Pre-registration of key subgroup hypotheses when the result will drive a major decision.

- Guardrails for harm, fairness, customer experience, and operational load.

Do not use post-treatment variables as effect modifiers. For example, if support tickets after outreach are included as features, the model may condition on a mediator or a downstream consequence of the treatment.

11. A Practical Readout Template

An HTE analysis should end with a decision-oriented summary, not only model diagnostics. A concise industry readout might look like this:

- Overall effect: the retention offer increases next-quarter net revenue by the estimated ATE.

- Main heterogeneity: effects rise sharply with pre-treatment risk score and are higher for enterprise accounts.

- Low-lift segment: low-risk, high-usage accounts have little incremental benefit and may be excluded from outreach.

- Proposed policy: contact the top 30% of accounts by predicted CATE.

- Expected value: compare net value per eligible account against random targeting and current targeting.

- Validation: monitor lift by predicted-CATE decile in the next randomized holdout.

- Guardrails: track opt-outs, complaints, support load, and fairness across protected or policy-relevant groups.

The best HTE project is not the one with the most complex model. It is the one where the causal estimand, validation plan, and policy decision fit together.

readout = pd.DataFrame(

{

"question": [

"Did the offer work on average?",

"Where is lift highest?",

"Which simple rule is a good baseline?",

"Which model-based rule performs best?",

"What should be validated next?",

],

"answer_from_this_simulation": [

f"Estimated ATE = {ate_stats['estimate']:.2f}; true ATE = {df['true_cate'].mean():.2f}.",

"High-risk accounts and enterprise accounts show larger treatment effects.",

"Highest-risk targeting is a strong transparent baseline.",

"Highest predicted-CATE targeting is closest to the oracle benchmark.",

"Run a holdout experiment and compare lift by predicted-CATE bucket.",

],

}

)

display(readout)| question | answer_from_this_simulation | |

|---|---|---|

| 0 | Did the offer work on average? | Estimated ATE = 3.63; true ATE = 3.55. |

| 1 | Where is lift highest? | High-risk accounts and enterprise accounts sho... |

| 2 | Which simple rule is a good baseline? | Highest-risk targeting is a strong transparent... |

| 3 | Which model-based rule performs best? | Highest predicted-CATE targeting is closest to... |

| 4 | What should be validated next? | Run a holdout experiment and compare lift by p... |

12. Common Failure Modes

HTE work can go wrong in predictable ways:

- Confusing high predicted outcome with high treatment responsiveness.

- Searching many subgroups and reporting only the most favorable one.

- Estimating subgroup effects on the same data used to discover the subgroup.

- Ignoring treatment cost, capacity, or customer-experience harm.

- Training on observational data without addressing confounding.

- Using features measured after treatment assignment.

- Reporting precise-looking individual effects when the reliable signal is only at the segment or bucket level.

- Deploying a targeting model without a randomized holdout to keep learning.

These failure modes explain why HTE is a causal workflow, not just a modeling task.

Key Takeaways

- The CATE, \(\tau(x)\), is the expected treatment effect for units with features \(X=x\).

- A positive ATE can hide customers with low or negative treatment effects.

- Prognostic variables predict outcome levels; effect modifiers predict treatment responsiveness.

- Start HTE analysis with transparent subgroup estimates before moving to flexible models.

- Interaction models are useful baselines because they are interpretable and easy to validate by bucket.

- Honest sample splitting helps prevent overclaiming data-discovered subgroups.

- CATE models become valuable when translated into targeting policies and validated with holdout experimental lift.

References

Athey, S., & Imbens, G. W. (2016). Recursive partitioning for heterogeneous causal effects. Proceedings of the National Academy of Sciences, 113(27), 7353-7360. https://doi.org/10.1073/pnas.1510489113

Hahn, P. R., Murray, J. S., & Carvalho, C. M. (2020). Bayesian regression tree models for causal inference: Regularization, confounding, and heterogeneous effects. Bayesian Analysis, 15(3), 965-1056. https://doi.org/10.1214/19-BA1195

Kunzel, S. R., Sekhon, J. S., Bickel, P. J., & Yu, B. (2019). Metalearners for estimating heterogeneous treatment effects using machine learning. Proceedings of the National Academy of Sciences, 116(10), 4156-4165. https://doi.org/10.1073/pnas.1804597116

Park, C., & Kang, H. (2023). A groupwise approach for inferring heterogeneous treatment effects in causal inference. Journal of the Royal Statistical Society Series A: Statistics in Society, 187(2), 374-392. https://doi.org/10.1093/jrsssa/qnad125

Shin, H., & Antonelli, J. (2023). Improved inference for doubly robust estimators of heterogeneous treatment effects. Biometrics, 79(4), 3140-3152. https://doi.org/10.1111/biom.13837

Wager, S., & Athey, S. (2018). Estimation and inference of heterogeneous treatment effects using random forests. Journal of the American Statistical Association, 113(523), 1228-1242. https://doi.org/10.1080/01621459.2017.1319839